How to Use Customer Reviews as a Community Bank Marketing Engine

Google reviews drive more new accounts than most paid campaigns. Here's how to build a review engine that actually works at a community bank.

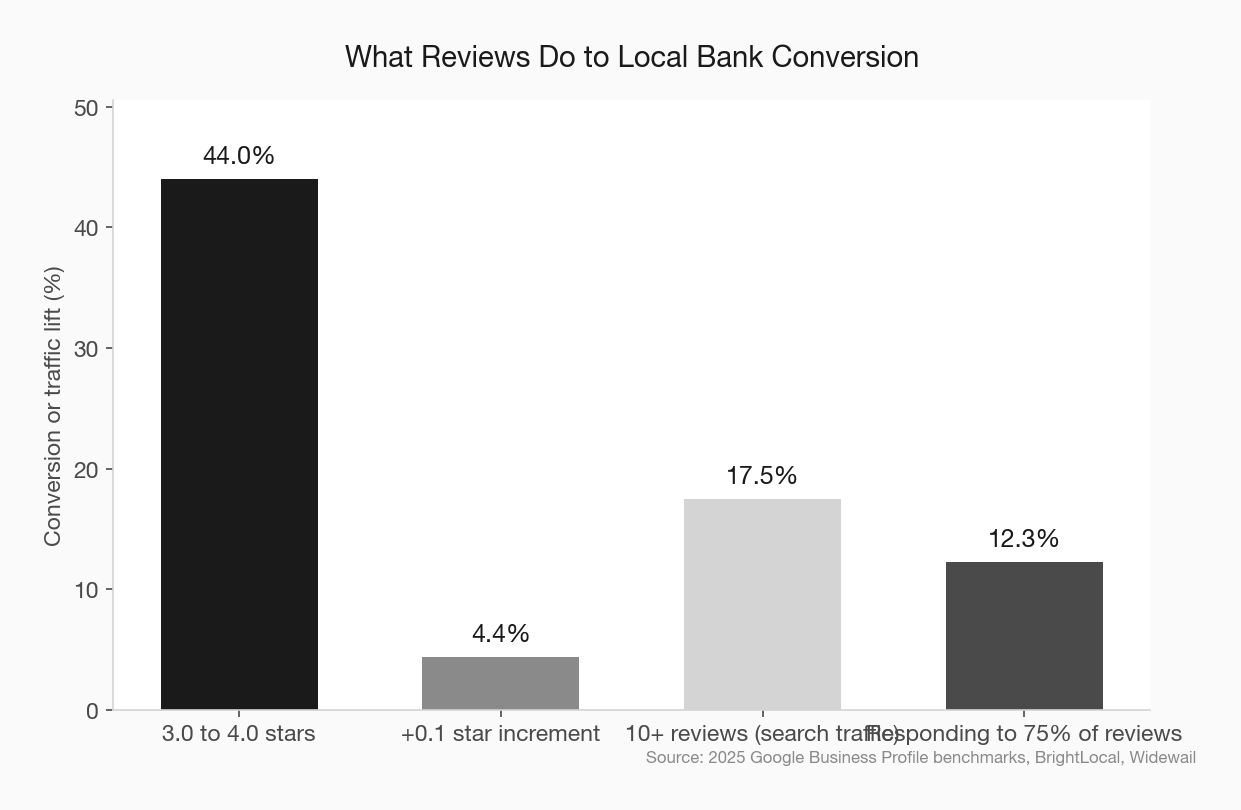

A single added star on a community bank’s Google rating is worth a 44% lift in local conversion. That is not a projection from a marketing deck. It is the number published in the 2025 Google Business Profile benchmarks for local businesses, and banking sits inside that range.

Community banks were raised on branch traffic, relationship managers, and quarterly board reviews. Reviews feel soft by comparison. They feel like something a marketing coordinator should handle on a Thursday afternoon.

That instinct is costing you deposits.

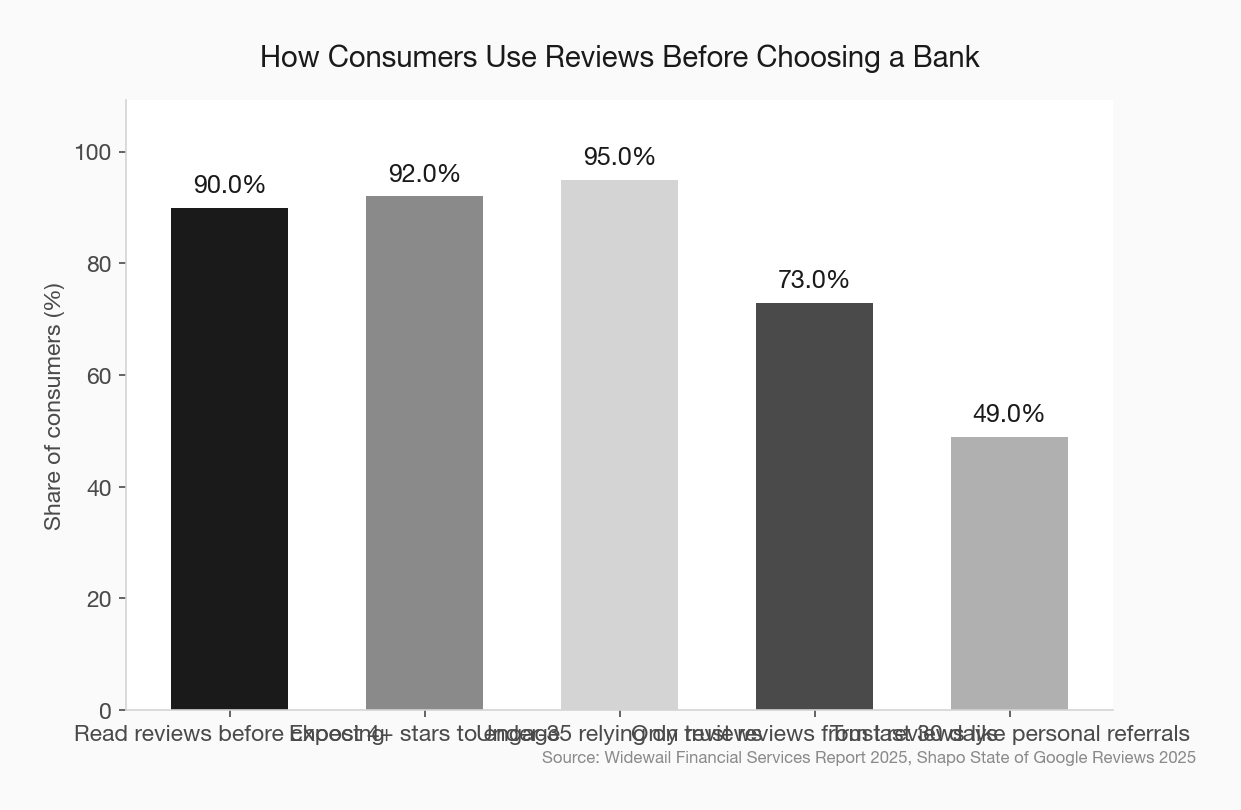

92% of consumers expect a 4+ star rating before they will engage with a business. 73% only trust reviews from the last 30 days. So your five-star review from 2023 is not doing the work you think it is. And the review your last small business loan customer did not leave is quietly closing doors on prospects you will never meet.

Reviews are the cheapest account acquisition channel most community banks can access. They are also the most ignored.

Why community banks have an unfair advantage here

Community banks have one thing megabanks and fintechs cannot reproduce. Real customers with real stories about people they know by name. The local builder. The ag family. The first-time homebuyer whose mortgage got across the line because someone in a branch picked up the phone.

That is the content Google ranks, and it is the content AI search engines pull into their summaries. A 28-year-old moving home after college is reading it the night before she picks where to deposit her first real paycheck.

Chime cannot manufacture that. JPMorgan cannot either. A branch manager who walked three families through 2008 loan modifications absolutely can.

But the story only exists as a marketing asset if it shows up on your Google Business Profile. A 4.8-star rating with 146 reviews is a different bank than a 3.9-star rating with 22 reviews, even if the institution, balance sheet, and staff are identical.

Widewail reports that 49% of consumers trust online reviews as much as personal recommendations. Among consumers under 35, 95% rely on reviews before engaging with a business. If you want a Gen Z deposit strategy, it starts here, not in your app redesign.

google business profile as a community bank marketing asset

What the numbers actually show

The math on reviews is not subtle:

- Moving from 3.0 to 4.0 stars lifts conversion by 44%

- Each additional tenth of a star adds 4.4% in conversion

- Businesses with 10 or more reviews see 15 to 20% more search traffic

- Responding to 75% of reviews improves conversion by 12.3%

A community bank averaging 3.8 stars across its branches is not losing a handful of customers. It is losing close to half the local-search foot traffic it would otherwise pull.

The sweet spot is narrower than most assume. 4.2 to 4.5 stars is where trust stabilizes. Above that, returns flatten. Below 4.2, the Financial Brand reports that AI-generated search responses begin pushing banks down in favor of better-rated competitors. That matters because 81% of consumers now use Google reviews when evaluating a local business.

You do not need to be perfect. You need to be above 4.2, and you need to be recent.

The moment matters more than the message

Most community banks that do ask for reviews ask in the wrong moment. The end of a teller transaction. A quarterly email blast. A pleading line in a statement insert.

Ask at the emotional peak of the relationship. Not at a routine touchpoint.

Northpointe Bank, a $3.9 billion community bank, asks at loan closings. That is the right instinct. Other moments worth building around:

- The day after a new account is funded

- The moment a mortgage pre-approval is issued

- The closing of a small business loan

- After a successful fraud resolution or account recovery

These are moments where the customer actually feels something. Gratitude. Relief. Pride. That is the window.

Widewail’s research shows 76% of customers who are directly asked to leave a review do it. The reason most community banks do not see that rate is not that their customers are unwilling. It is that the ask happens in the wrong context, from the wrong person, at the wrong time.

Train branch staff to ask at closings. Build an automated SMS or email follow-up for digital account opens. Give loan officers a short script and make asking part of the closing checklist.

What to ask and how to frame it

The weakest version of a review request is “Please leave us a review on Google.” It is generic. It invites nothing.

Stronger prompts:

- “Would you recommend us to a family member?”

- “Did we help you get to closing smoother than you expected?”

- “What did our team get right for you today?”

Frame the ask as a question the customer actually wants to answer. Most people already have a story rehearsed in their head about their experience. Your job is to give them a reason to type it out.

One warning. Do not offer incentives for reviews. It violates Google’s policies and puts your entire Business Profile at risk of suppression. Widewail and BrightLocal both flag this as the single most common banking mistake in review generation. The risk is not hypothetical. Profiles have been wiped.

Also, do not filter. Do not ask only the customers you know will leave five stars. Google detects unnaturally skewed review patterns. A branch with a 5.0 average and zero three-star reviews looks statistically wrong, and the algorithm treats it that way.

local seo for community banks

Responding is where most banks fall apart

You can do everything else well and still leave most of the value sitting there if you skip responses.

71% of customers are more likely to choose a business that responds to all of its reviews. Replying to all reviews by itself lifts conversion by 5.1%.

Community banks usually respond in one of three broken ways. They do not respond at all. They paste in a canned “thank you for your feedback” on every review. Or, worst, they write a defensive paragraph that leaves a worse impression than the original review.

A strong response looks like this:

- Thank the customer by name

- Reference something specific from their review

- Keep it to three sentences or fewer

- If it needs to continue, invite them offline

For negative reviews, the instinct is to explain yourself. Resist it. Take responsibility briefly, offer a direct contact, and move the conversation off the public page. A one-star review with a calm, specific response converts better than a one-star review with no reply at all. Public silence reads as indifference.

A 30-day review engine for community banks

Starting from nothing, here is the sequence.

Week 1: Audit. Pull the star rating and review count for every branch on Google Business Profile. Flag any branch under 4.2 stars. Identify reviews from the last 90 days that went unanswered.

Week 2: Instrument the ask. Choose three moments that map to emotional peaks. Loan close, new account funding, problem resolution. Build a short SMS and email template for each. Train branch staff on when and how to ask in person at those moments.

Week 3: Clear the backlog. Write a response to every review from the last 12 months, oldest first. Prioritize the negative ones. Short, specific, human.

Week 4: Close the loop. Assign one owner to monitor reviews daily. Marketing, CX, or a branch ops lead. Set a clear target of 10 new reviews per branch per month. Track average star rating, response rate, and percent of reviews responded to within 48 hours.

community bank marketing metrics that matter

This is a 30-day program with a multi-year payoff. And unlike most marketing spend, the assets you build here compound.

The compounding effect nobody talks about

Paid acquisition ends the day the spend stops. A Facebook campaign is gone in 48 hours. A rebrand costs six figures and ages poorly. A Google review stays on the Business Profile for as long as Google exists, which is likely longer than your core provider.

A bank that commits to 10 reviews per branch per month for two years builds a 240-review portfolio per location. That portfolio then shows up in every local search, in every AI-generated banking summary, and on every map pack impression for as long as the bank operates in that market.

The banks that start treating reviews as a first-class marketing channel in 2026 are the ones people will find in 2028. The ones that keep relying on a board-approved rebrand cycle will spend the next three years wondering why the mobile app refresh and the new logo did not move the conversion needle.

community bank website conversion

The final thought

Community banks love to complain about the marketing budget gap against fintechs. In one sense, they are right. A single Chime acquisition campaign dwarfs what a $600 million bank can spend in a year.

But Chime cannot manufacture a real customer at a real branch thanking a real loan officer by name. You can. Your customers are already doing it in conversation. The only question is whether the rest of your market ever hears it.

Ask. Respond. Measure. The playbook is boring, repeatable, and almost free. Which is exactly why most community banks will not bother, and why the ones that do will pull ahead in local search for the next decade.