Buy Now, Pay Later Is in Your Backyard — And Your Customers Are Using It

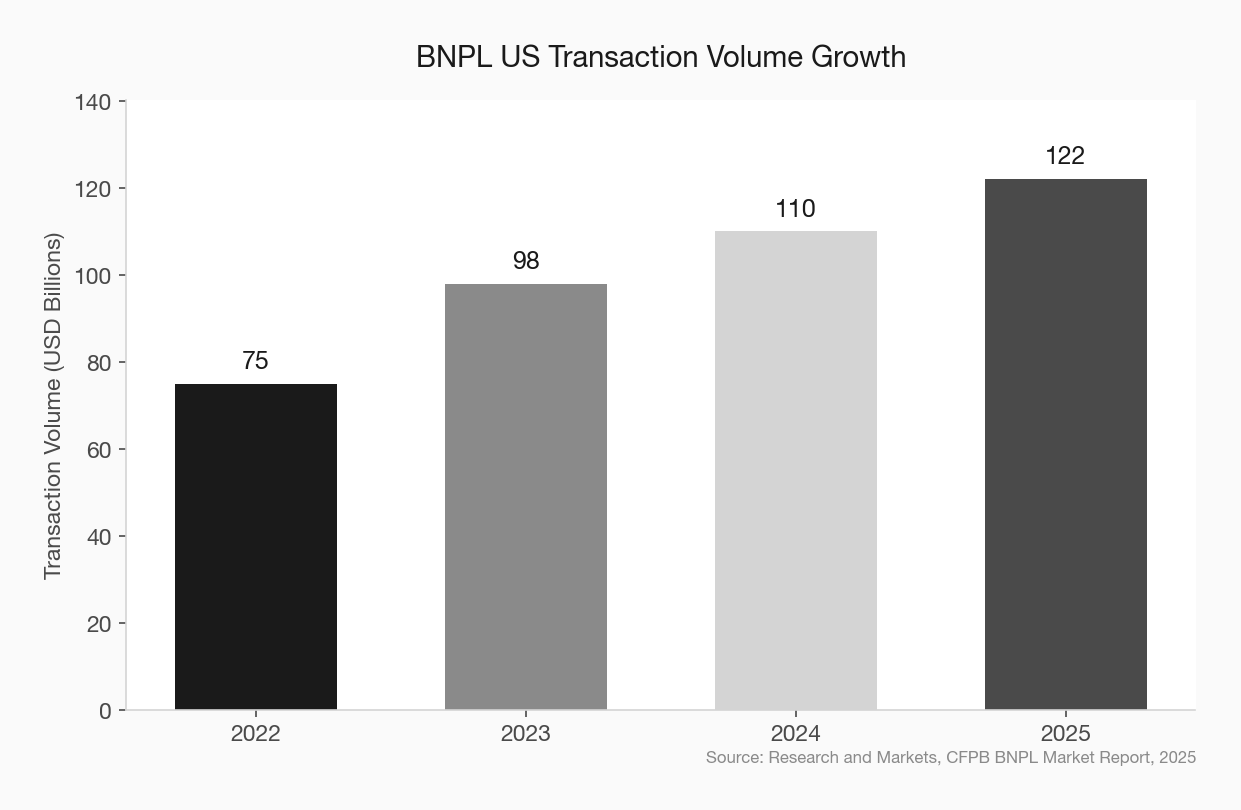

Affirm and Klarna processed over $122 billion in US BNPL transactions in 2025. Here's what community banks need to know — and do — right now.

Ninety-one million Americans used a buy now, pay later service in 2025. That’s not a rounding error — it’s more than a quarter of the US adult population financing purchases through Affirm, Klarna, Afterpay, or PayPal Credit instead of reaching for a personal loan or a credit card from their bank.

BNPL crossed $122 billion in US transaction volume in 2025, up nearly 11% year over year. Six major providers originated 335.8 million BNPL loans totaling $45.2 billion in 2023 alone. These aren’t payday borrowers or credit-invisible consumers. They’re your customers — using a product that should have been yours to offer.

Community banks have watched this category grow for five years. Most are still watching. That’s a strategic mistake they can still correct.

What BNPL Actually Is — And Why Banks Keep Misreading It

BNPL gets described as a payments product. It’s not. It’s a credit product dressed up as a payments product — which is precisely why it’s so dangerous to banks.

When a customer finances a $600 appliance through Affirm, they’re not using a payment method. They’re taking out an installment loan. The difference is that Affirm offered it at checkout in 15 seconds, required no separate application, and never asked them to call their bank.

That’s the threat in clear terms: BNPL providers are originating installment credit at the point of purchase, at a speed and convenience that community banks can’t match with legacy underwriting and loan origination workflows.

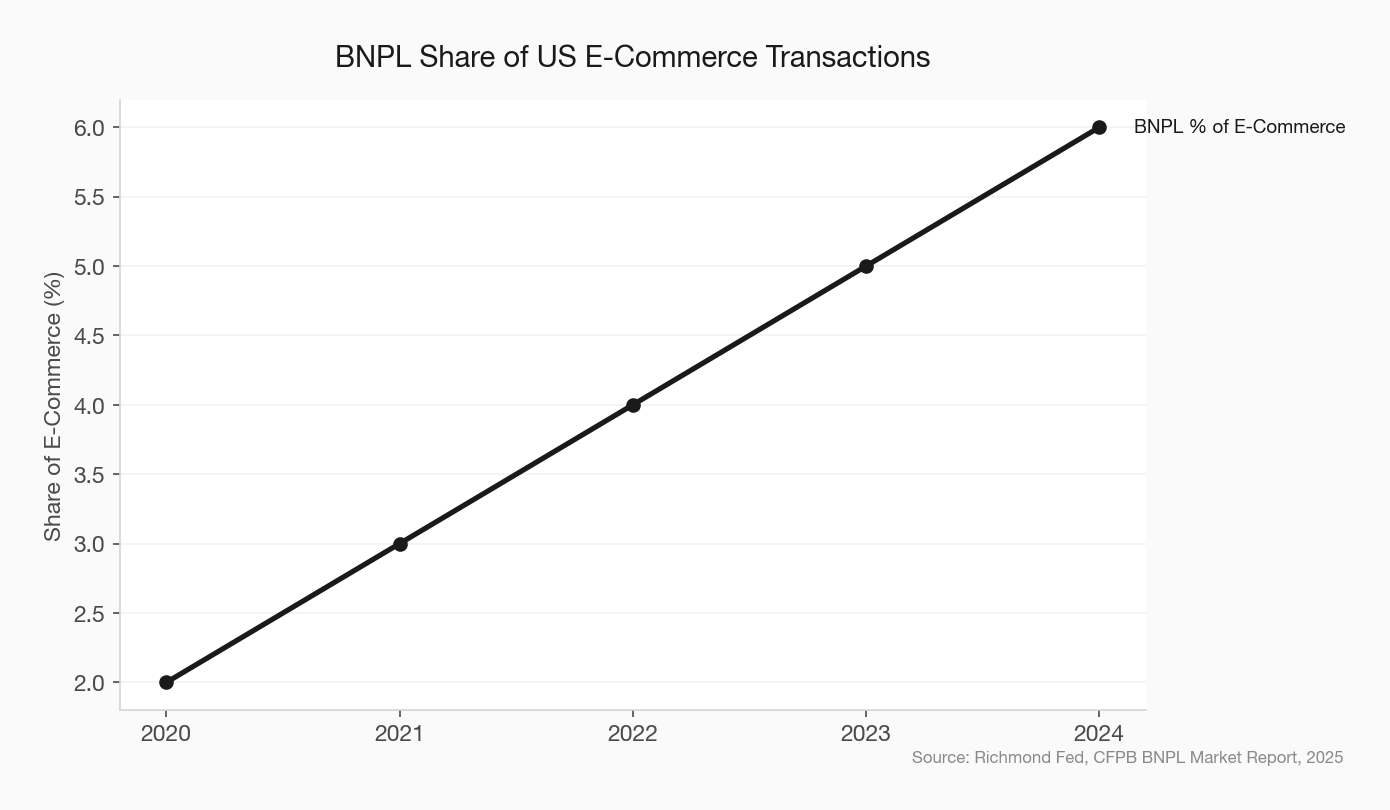

The category started with e-commerce. BNPL financed 6% of all US e-commerce transactions in 2024, up from just 2% in 2020. But it’s expanding rapidly into home improvement, healthcare, and even B2B purchasing. J.P. Morgan partnered with Klarna in 2025 to bring installment payments to its commercial clients. The category is moving upstream.

The Revenue That’s Already Gone

Before talking about what community banks should do, it’s worth being honest about what’s already been lost.

BNPL has directly cannibalized two product categories that traditionally lived at banks: personal loans and credit card revolving balances. Among younger consumers — the ones building financial relationships right now — BNPL is the preferred short-term financing tool. Credit card applications among Gen Z and younger Millennials have declined as BNPL adoption has risen.

Personal loan portfolios at community banks haven’t collapsed — yet. But the growth that should be coming isn’t materializing. New households that would have opened a personal line of credit five years ago are instead installing the Klarna app. The relationship formation that used to happen through lending is now happening through a fintech that will use it to cross-sell everything else.

This isn’t theoretical. The CFPB’s December 2025 BNPL market report documented that BNPL providers are actively expanding into deposit accounts, debit cards, and savings products — using BNPL as the customer acquisition vehicle. Affirm and Klarna are not just loan processors. They’re building primary financial relationships, using installment credit as the entry point.

how fintechs use credit as a customer acquisition tool

Where the Community Bank Advantage Sits

Here’s the part most community bankers miss: you are not losing to a better product. You are losing to a more convenient distribution of an inferior product.

BNPL loans typically carry higher effective costs than a personal loan from a community bank. The consumer doesn’t see it that way because the friction of a traditional loan application is invisible to them — but the convenience of a checkout integration is not.

That’s a solvable problem. Community banks have real structural advantages in this category:

Existing relationships. Your customers already trust you. A BNPL offer from their community bank — embedded in online banking or offered proactively by a banker — carries credibility that Klarna cannot manufacture.

Superior underwriting data. You have deposit history, transaction behavior, and relationship context that BNPL providers are guessing at. You can price better and extend credit more confidently.

Regulatory standing. BNPL providers operate under a patchwork of state oversight that’s tightening. The UK mandated creditworthiness assessments for BNPL in 2025. Australia followed. US regulation is moving in the same direction. Banks already operate under the framework that’s coming for fintechs — which means bank-issued BNPL is more defensible as scrutiny increases.

No-delinquency economics. Community bank underwriting on installment products has consistently outperformed fintech BNPL on credit quality. Approximately 34–41% of BNPL users miss at least one payment. Community banks don’t need to accept that default rate to be competitive — they just need to show up where the purchase happens.

community bank lending advantages over fintech competitors

The Response Playbook

There is no reason for a community bank to sit on the sideline of this category. Here’s what a practical response looks like.

Option 1: Activate through your core vendor

Jack Henry expanded its white-label BNPL capability to its SilverLake platform in 2025. That means hundreds of community banks can activate BNPL features inside their existing digital banking experience — no new vendor, no rebuild. Affirm also partnered with FIS to embed installment options into FIS client banks’ digital products.

If your core provider has a BNPL activation path, the first call you make this week should be to your relationship manager to understand the timeline and terms.

Option 2: Proactive installment offers at known purchase moments

BNPL wins at checkout because it intercepts customers before they think about their bank. Community banks can intercept earlier.

If a customer’s debit card shows a series of home improvement transactions, your mobile app can surface an installment loan offer before they reach the Home Depot self-checkout and tap Affirm. If a customer deposits a large check and then shows no activity, a banker’s outreach call about a flexible personal line makes sense.

This isn’t magic — it’s using transaction data you already have to make proactive offers at moments that matter.

Option 3: Target the merchants, not just the consumers

BNPL providers win by sitting at the point of sale. Community banks can do the same through local merchant relationships.

A community bank that approaches local retailers, contractors, and healthcare providers with a bank-sponsored installment financing program at checkout is competing directly with Affirm — with better rates, better underwriting, and a local relationship behind it. Several community banks have launched merchant-facing installment programs with notable success in home services and elective healthcare categories.

small business banking programs that compete with fintech

Option 4: Tell customers what BNPL actually costs

This one is underrated. Many consumers don’t understand the effective APR on a BNPL product compared to a personal loan from their bank — particularly late fee structures and deferred interest products. Community banks are positioned as trusted advisors, not just lenders.

Proactive financial education — through email, social, or banker conversations — that helps customers compare the true cost of BNPL against a bank personal loan builds trust and often brings the loan back to the bank. The ICBA has published guidance on exactly this approach.

community bank financial education as a brand strategy

The Window Is Closing

The institutions adopting in-house BNPL features tripled in 2025 compared to the prior year. That curve will keep moving. The community banks that build or activate an installment product now will have deposit data, merchant relationships, and consumer habits locked in before the category matures.

The ones that wait until BNPL is “a bigger deal” will be playing catch-up in a market where Affirm and Klarna have already established the consumer habit. Breaking an entrenched financial habit is harder and more expensive than forming one.

BNPL is not a niche product for Gen Z shoppers. It’s a $122 billion installment credit market that grew out of your loan portfolio. The category is your expertise, your customer, and your opportunity. Act like it.