Deposit Wars: How Community Banks Can Compete Without Destroying Margins

Rate-matching fintechs is a losing game. Community banks that win deposits in 2026 compete on trust, convenience, and full relationships — not basis points.

In February 2026, money market fund assets hit $8.2 trillion — a record. That’s $8.2 trillion sitting outside the banking system, much of it pulled from community bank accounts by customers chasing yield at SoFi, Ally, and a growing list of fintechs offering 3.3% to 4.0% APY with zero friction.

Meanwhile, 54% of community bank CEOs now say deposit growth is their biggest challenge, according to ICBA’s 2025 CEO Outlook. That’s a staggering reversal from 2022, when just 4% cited deposits as a concern. The deposit game has fundamentally changed, and community banks that respond by matching rates will bleed margin until there’s nothing left.

The banks that are winning deposits right now aren’t winning on rate. They’re winning on something fintechs structurally cannot offer: full-relationship banking built on trust, local knowledge, and a level of service that no chatbot can replicate.

The Rate-Matching Trap

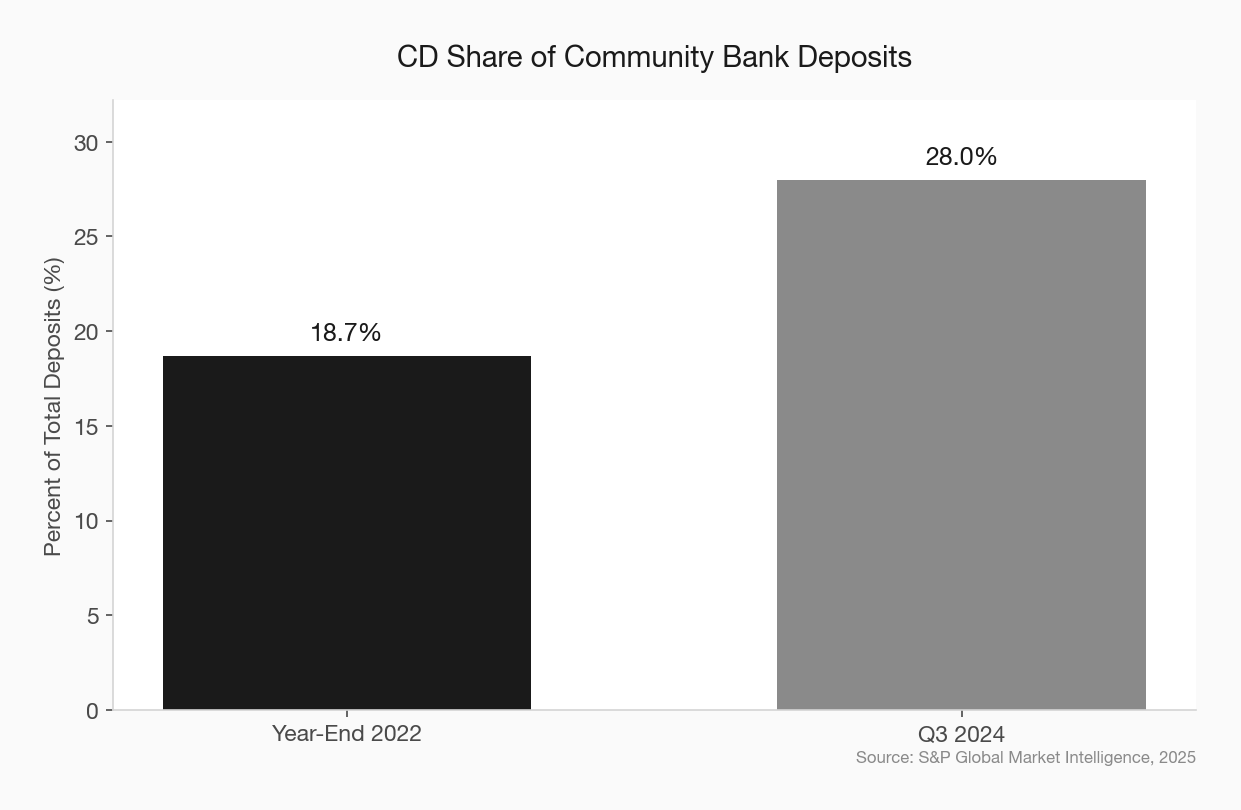

Here’s the math that should keep every community bank CFO up at night: CDs now represent nearly 28% of community bank deposits, up from 18.7% at the end of 2022. That shift — from cheap core deposits to expensive time deposits — is the real margin story, and it’s one community banks inflicted on themselves.

When a fintech offers 4% on savings with no minimums and a three-minute onboarding flow, the instinct is to respond with a rate special. But a community bank posting a 4.5% CD rate to compete with SoFi isn’t competing — it’s capitulating. You’re paying a premium for money that will leave the moment someone else offers 4.6%.

The FDIC’s Q4 2025 data offers a glimmer of hope: community bank NIM rose to 3.77%, the highest since 2018, driven by a 9 basis-point drop in the cost of funds. But that improvement came from the repricing cycle catching up, not from banks suddenly getting smarter about deposit strategy. The structural problem remains: too many community banks are funding growth with expensive, rate-sensitive money.

What Fintechs Actually Win On (It’s Not Just Rate)

Community bankers love to blame fintech deposit growth on rates alone. That’s comfortable, because rates are something you can point to. But it misses the bigger picture.

20% of Gen Z and 21% of Millennials told JD Power they would “definitely or probably” switch their primary bank in the next six months. They’re not leaving because Ally pays 30 more basis points. They’re leaving because opening an account at a fintech takes three minutes, transfers happen instantly, and the app doesn’t look like it was designed in 2009.

Chime grew from 7,000 users to 7 million in under a decade, processing $8 billion in monthly transactions. Revolut generated $2.2 billion in revenue in 2023. Jenius Bank hit $1 billion in deposits before its first anniversary. These companies didn’t win on rate — they won on experience, speed, and an absence of friction.

This is actually good news for community banks. Because while matching rates is expensive and unsustainable, fixing your digital experience and deepening relationships is something you can do profitably.

The Three Things That Actually Win Deposits

1. Full-Relationship Depth, Not Product Peddling

The banks topping S&P Global’s inaugural deposit rankings aren’t the ones with the highest rates. Western Bank in Artesia, New Mexico secured the second spot among small community banks with a noninterest-bearing deposit concentration of 59.17%. Titan Bank led the category with 46.79% noninterest-bearing deposits and consistent average deposit growth of 5.4% over eight quarters.

What do these banks have in common? They don’t compete on rate because their depositors aren’t there for rate. They’re there for the full relationship — lending, treasury management, advisory conversations, and the kind of local knowledge that no algorithm can replicate.

The community bank that knows a business owner’s cash flow cycle, understands their expansion plans, and has financed their last three equipment purchases holds deposits that are essentially immune to rate competition. That customer isn’t moving $500,000 to SoFi for an extra 50 basis points. The switching cost is too high because the relationship is too valuable.

This is the strategic insight most community banks miss: deposit retention is a downstream effect of relationship depth, not a pricing problem.

2. Eliminate the Friction That Drives Customers Away

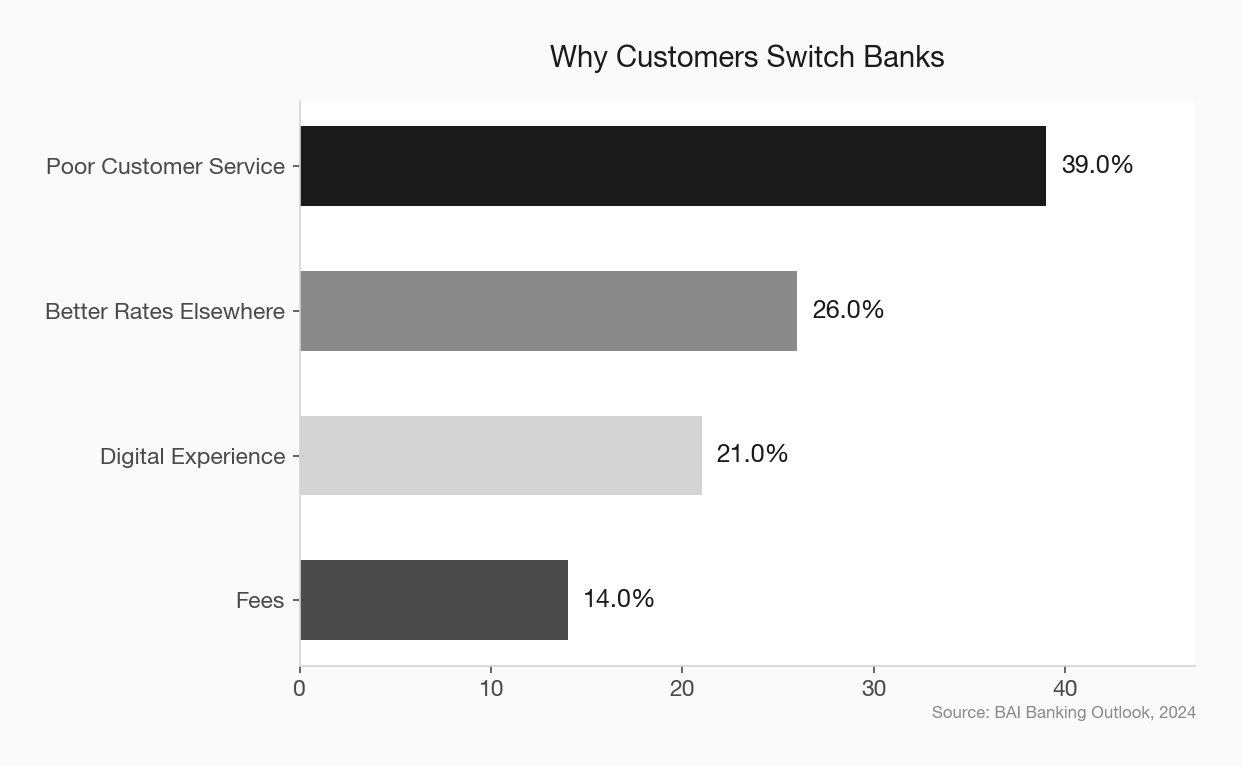

In 2023, 39% of banking customers who switched banks cited poor customer service as the reason. Not rates. Service.

And “service” in 2026 doesn’t just mean a friendly teller. It means digital account opening that doesn’t require a branch visit. It means a mobile app that actually works. It means instant fund availability, not three-day holds. It means responding to a secure message in hours, not days.

94% of financial institutions plan to embed fintech solutions into their digital banking experiences, according to Jack Henry’s 2025 Strategy Benchmark. The banks moving fastest are the ones that understand a simple truth: you don’t need to build like a fintech, but you do need to remove the friction that makes customers consider one.

Seattle Bank offers a useful model: they report a 70% retention rate on CD customers, converting many into full banking relationships. The tactic isn’t magic — it’s intentional follow-up, staff training on relationship conversations, and a process that treats every CD maturity as a retention opportunity rather than a transaction.

3. Tell People Where Their Money Goes

Here’s the most underused weapon in community banking: the local impact story.

Every dollar deposited at a community bank gets lent back into the local economy — small business loans, home mortgages, farm operating lines. A community bank can lend approximately $10 into its local economy for every dollar it earns in profit. A fintech deposit? That money disappears into a partner bank’s balance sheet somewhere, funding who-knows-what.

This is not a sentimental argument. It’s a value proposition. Businesses that bank locally are banking with an institution that has a direct financial stake in the same economy they operate in. That alignment matters — and community banks are terrible at articulating it.

Brattleboro Savings & Loan gets this right. Their marketing explicitly connects deposits to local homebuyers and small businesses. It’s specific. It’s tangible. And it gives depositors a reason to stay that has nothing to do with APY.

The Vertical Strategy: Go Niche, Go Deep

The Financial Brand recently highlighted a growing trend: community banks going vertical. Instead of trying to be everything to everyone — and competing on rate with institutions that have 100x the marketing budget — the smartest community banks are picking a lane and owning it.

That might be healthcare practices. Agricultural operations. Dental offices. Construction companies. The specifics matter less than the strategy: pick a niche where your lending expertise and local knowledge create a moat, then build deposit relationships around those verticals.

80% of banks and credit unions plan to expand SMB services in 2026, up from 65% in 2023. The banks that move first into underserved verticals won’t just win deposits — they’ll win the kind of sticky, full-relationship deposits that never leave for a basis point.

community bank brand story strategy community bank website conversion optimization embedded finance threat to community banks what Chime knows about branding community bank digital transformation strategy

The Stablecoin Wild Card

One more wrinkle community banks can’t afford to ignore: stablecoins. Deloitte’s 2026 banking outlook flags this as a potentially pivotal year for stablecoin adoption, and the implications for deposits are significant. If customers can park dollars in a tokenized, yield-bearing stablecoin outside the banking system entirely, the deposit competition picture gets even more complex.

Community banks don’t need a stablecoin strategy today. But they need to understand that the competition for deposits is expanding beyond other banks and fintechs — it’s moving toward entirely new rails. The banks with the deepest relationships and the strongest local value proposition will be the last ones standing when that wave arrives.

Stop Playing Their Game

The deposit wars are real. Core deposits grew 4% across U.S. commercial banks in 2025, but that growth was uneven — banks with between $10 billion and $100 billion in assets grew core deposits by more than 8%, largely driven by M&A. For the typical community bank, organic deposit growth remains a grind.

But the solution isn’t a rate war. It never has been.

The community banks winning deposits in 2026 are doing three things: deepening relationships so deposits stick, removing digital friction so customers don’t leave out of frustration, and telling a local impact story that gives people a reason to care where their money sits. None of that requires destroying your margin. All of it requires intentionality, investment in your people and your technology, and the discipline to stop chasing rate-sensitive money that was never going to stay.

Your deposit strategy is your growth strategy. Make sure it’s one you can actually sustain.