Document AI Is the Fastest ROI in Community Banking Right Now

Loan documents, account paperwork, compliance filings — they're still mostly manual at community banks. Document AI changes that with minimal IT lift and payback in under a year.

More than 40% of bank employees spend nearly 10 hours a week on repetitive document tasks — data entry, file indexing, form extraction, and compliance prep. That’s a full quarter of the work week, every week, consumed by work that software can do better.

This is not a future problem to solve in the next digital transformation initiative. It is a present-day cost structure sitting on your income statement right now.

Document AI — specifically, Intelligent Document Processing (IDP) tools that combine optical character recognition with machine learning — is the highest-return technology investment available to community banks in 2026. The ROI math is clear, the implementation risk is low, and the payback window is typically six to twelve months. What’s missing is urgency.

The Document Problem Every Community Bank Has

Community banking runs on paper. Loan applications. Tax returns. Personal financial statements. W-2s. Business bank statements. BSA alerts. SAR narratives. Account opening forms. Each of these documents contains structured data that needs to be extracted, validated, and entered into a system — and in most community banks, a human does it manually.

The consequences are predictable: loan officers spend hours on document prep instead of client relationships. Compliance staff draft SAR narratives line by line. New account openings stall on identity verification. None of this is value-added work. It is process friction that costs money and slows the customer experience.

The average community bank processing 400 loans per year spends between 6 and 12 staff hours per loan on document-related tasks alone. At a fully loaded labor cost of $45 per hour, that’s $108,000 to $216,000 annually — just in manual document handling on the loan side. Add compliance and deposit operations and the number grows considerably.

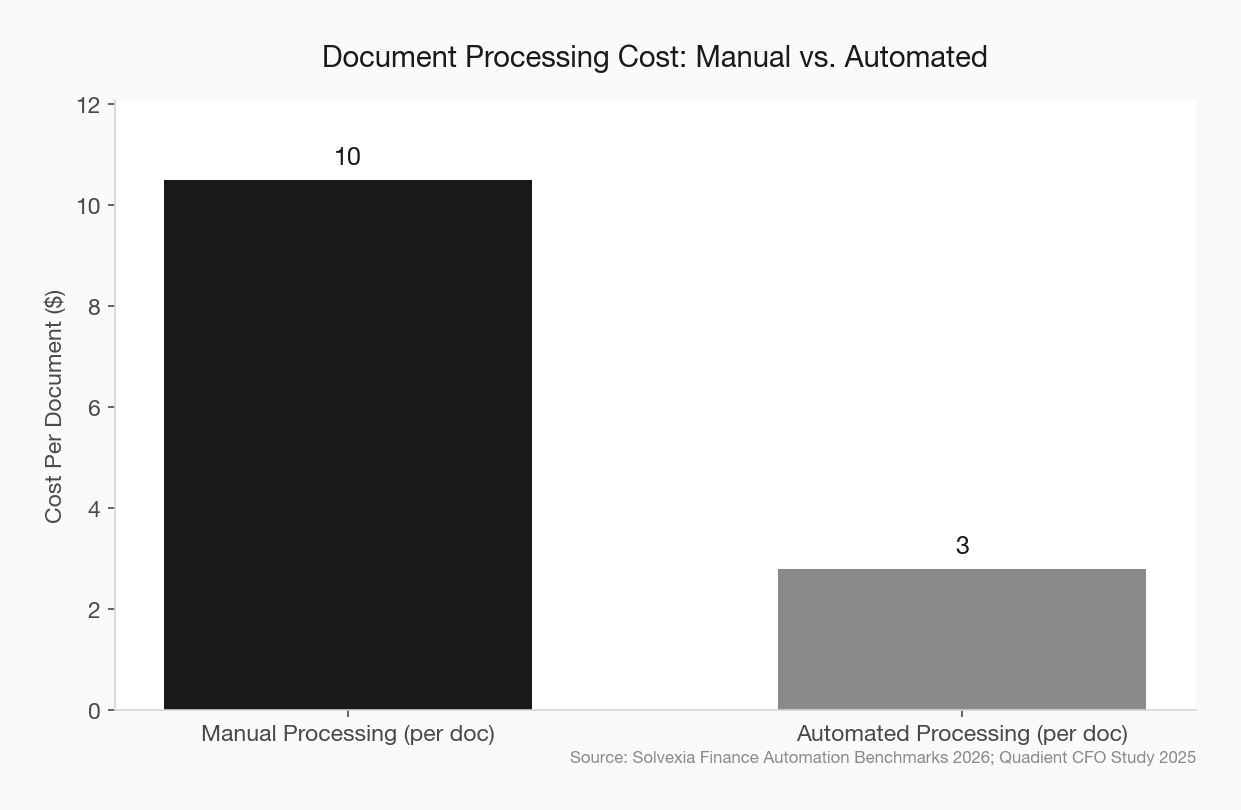

Organizations that implement document automation reduce document-related operating costs by 30% to 60%, according to Solvexia’s 2026 finance automation benchmarks. The savings per document processed average $8 to $12 compared to manual workflows.

What Document AI Actually Does (and Doesn’t Do)

Document AI is not magic and it is not a replacement for judgment. It is a classification and extraction engine.

You feed it a document — a tax return, a bank statement, an insurance certificate, a government ID. The system identifies what it is, extracts the relevant data fields, validates them against rules or databases, and populates the appropriate downstream system. What used to take a loan processor 25 minutes takes the software 90 seconds.

The human remains in the loop for exceptions, edge cases, and final decisions. Document AI handles the volume; people handle the judgment.

Modern IDP tools are trained on millions of financial documents and can classify over 1,600 document types out of the box. They handle messy inputs — handwritten notes, low-resolution scans, non-standard formats — with accuracy rates above 95% for most financial document categories.

What document AI does not do: it does not make credit decisions, it does not replace your underwriter, and it does not eliminate the need for a skilled loan officer. It removes the prep work so those people can focus on what they were hired to do.

Three Places to Start

Community banks should prioritize document AI based on three criteria: volume, repetitiveness, and downstream impact. By those measures, three use cases stand out.

Loan Origination and Financial Spreading

Tax returns, business financial statements, and personal financial statements are the most labor-intensive documents in the commercial lending workflow. A standard small business loan package might contain 50 to 100 pages of documents, each requiring manual review and data entry into a spreading tool.

Document AI extracts line items from tax returns (1040s, 1120s, Schedule Cs), populates spreading templates automatically, flags discrepancies between years, and pre-fills the data fields your underwriter needs to make a decision. The underwriter reviews, adjusts, and approves — but starts from a 90%-complete document instead of a blank screen.

Bankers Trust, a $7 billion Iowa-based community bank, reduced the processing time on certain commercial loans from two weeks to three to five days after implementing AI-assisted loan origination through Abrigo. That improvement came primarily from reducing document handling time, not from changing the credit decision process.

New Account Opening and KYC

Account opening abandonment is a significant conversion problem for community banks — and a meaningful chunk of that friction comes from identity document verification. Customers upload or photograph a driver’s license, a utility bill, a passport. A human manually reviews, enters the data, and checks it against identity databases.

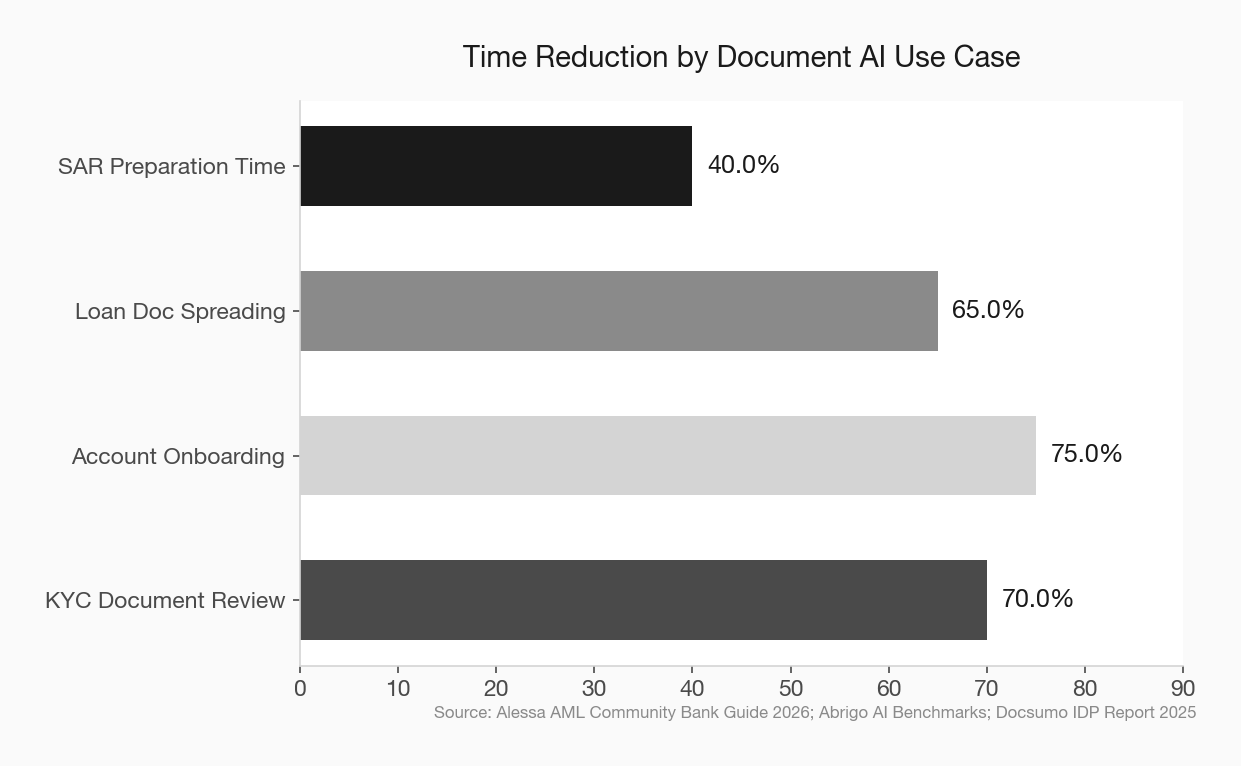

Document AI automates this entirely. It extracts data from government IDs, validates fields against authoritative databases, cross-references uploaded documents for consistency, and flags anomalies for human review. What takes 15 to 20 minutes of manual staff time takes under 2 minutes with AI.

The downstream effect is measurable. Shorter onboarding workflows directly reduce abandonment. One financial services firm cited in Docsumo’s 2025 IDP market report cut its onboarding time from 48 hours to under 4 hours after implementing document automation — resulting in a 34% increase in completed applications.

BSA/AML Compliance Filing

Suspicious Activity Reports are the highest-friction compliance document in community banking. BSA officers spend hours reviewing transaction data, organizing supporting documentation, and drafting narratives — work that must be done accurately but consumes capacity that could go toward actual risk detection.

Document AI applied to BSA workflows handles document organization, data extraction from transaction reports, and — increasingly — draft narrative generation. The BSA officer reviews, edits, and approves rather than building from scratch. Banks implementing AI-enhanced compliance tools report 30% to 50% reductions in SAR preparation time, along with 40% to 60% reductions in false positive alerts that trigger unnecessary manual review.

The Vendor Landscape Built for Your Scale

Enterprise document AI vendors — the ones selling to JPMorgan and Bank of America — exist, but they’re not your best option. Their implementations are complex, expensive, and designed for institutions with full IT departments.

The vendors worth evaluating for community banks under $2 billion in assets are:

Ocrolus focuses on financial document automation for lenders, with pre-built workflows for bank statements, pay stubs, tax returns, and income verification. It integrates with major loan origination systems and requires minimal custom configuration.

Abrigo is already embedded in hundreds of community bank workflows for credit analysis and BSA compliance. Their AI-enhanced modules layer document automation on top of systems many community banks already use, making adoption easier and implementation risk lower.

Encapture (now part of the nCino ecosystem) focuses on loan document capture and processing specifically for community and regional banks, with pre-built templates for common commercial loan document types.

ABBYY Vantage and Klearstack are flexible IDP platforms with financial services templates that work across loan operations, onboarding, and compliance — useful if you want one platform rather than point solutions.

The right choice depends on where your highest friction is today and what systems you already run. A bank already on nCino should evaluate Encapture first. A bank with significant commercial lending volume should look at Ocrolus or Abrigo. A bank whose primary pain point is BSA prep should start with Abrigo’s compliance modules.

community bank loan origination software comparison

What Implementation Actually Looks Like

The reason document AI has stayed theoretical at many community banks is the assumption that implementation is complicated. For enterprise ERP integrations, that assumption is correct. For document AI tools, it often isn’t.

Most modern IDP platforms are cloud-based, pre-trained on financial documents, and offer API connections to common banking systems. A typical implementation for a focused use case — say, tax return extraction for commercial lending — takes four to eight weeks, involves minimal IT resources, and can run in parallel with existing workflows while staff validate accuracy.

The critical success factors are not technical. They are operational. You need a process owner who can define what “good” extraction looks like, a pilot cohort of documents to test against, and a feedback loop for the first 60 days to train edge-case handling. These are project management challenges, not technology challenges.

Banks that fail at document AI implementations almost always fail for one of two reasons: they tried to automate too many document types simultaneously before validating accuracy, or they didn’t assign a business owner to the project and let IT drive it alone.

how to evaluate a fintech partnership without getting burned

The ROI Math Is Not Complicated

Here is a simple framework.

Take your current commercial loan volume. Multiply by the average staff hours per loan on document tasks. Multiply by your fully loaded labor cost per hour. That is your current annual document handling cost for lending alone.

Now apply a 60% efficiency improvement — the midpoint of industry benchmarks for document AI adoption. The result is your potential annual savings from one use case.

For a bank processing 300 commercial loans per year at 8 staff hours per loan at $45 per hour, that is $108,000 in annual labor costs on loan document prep. A 60% reduction saves $64,800 per year. A typical document AI implementation for this use case costs $25,000 to $60,000 in the first year, including setup and licensing.

That is a payback period of six months to one year — before accounting for faster loan processing, reduced error rates, and lower compliance risk.

The institutions processing 500 loans per month that have adopted document AI are reporting $500,000 to $700,000 in annual labor savings from automation alone, according to TIMVERO’s 2026 lending automation analysis.

AI tools your community bank should actually be using right now

Stop Waiting for the Right Moment

The most common reason community banks haven’t moved on document AI is not budget and it is not technology risk. It is the persistent belief that there will be a better time to start — after the core conversion, after the new hire, after the strategic plan.

There will not be a better time. The process friction is costing you money right now. Your competitors who started 18 months ago have already recaptured that labor cost and redeployed it into relationship banking.

Document AI is not a transformation initiative. It is a targeted fix for a specific, measurable problem. Pick one use case, pick a vendor that fits your existing stack, run a 90-day pilot, and measure the results. If it works — and at most institutions, it will — expand from there.

The community banks that will look back on 2026 as a turning point are the ones that stopped treating “we’re too busy to automate the work that makes us busy” as a strategy.

document AI case study AI loan processing community banks the real cost of your core banking system