Earned Wage Access: When Your Customer's Employer Becomes Their Banker

EWA platforms like DailyPay are quietly shifting direct deposit relationships away from community banks. Here's the threat — and what to do about it.

Something is happening quietly in the payroll departments of hospitals, restaurants, and logistics companies in your market. Your customers’ employers are signing contracts with companies like DailyPay, Payactiv, and Tapcheck. And with each signature, the direct deposit relationship you thought you owned gets a little less certain.

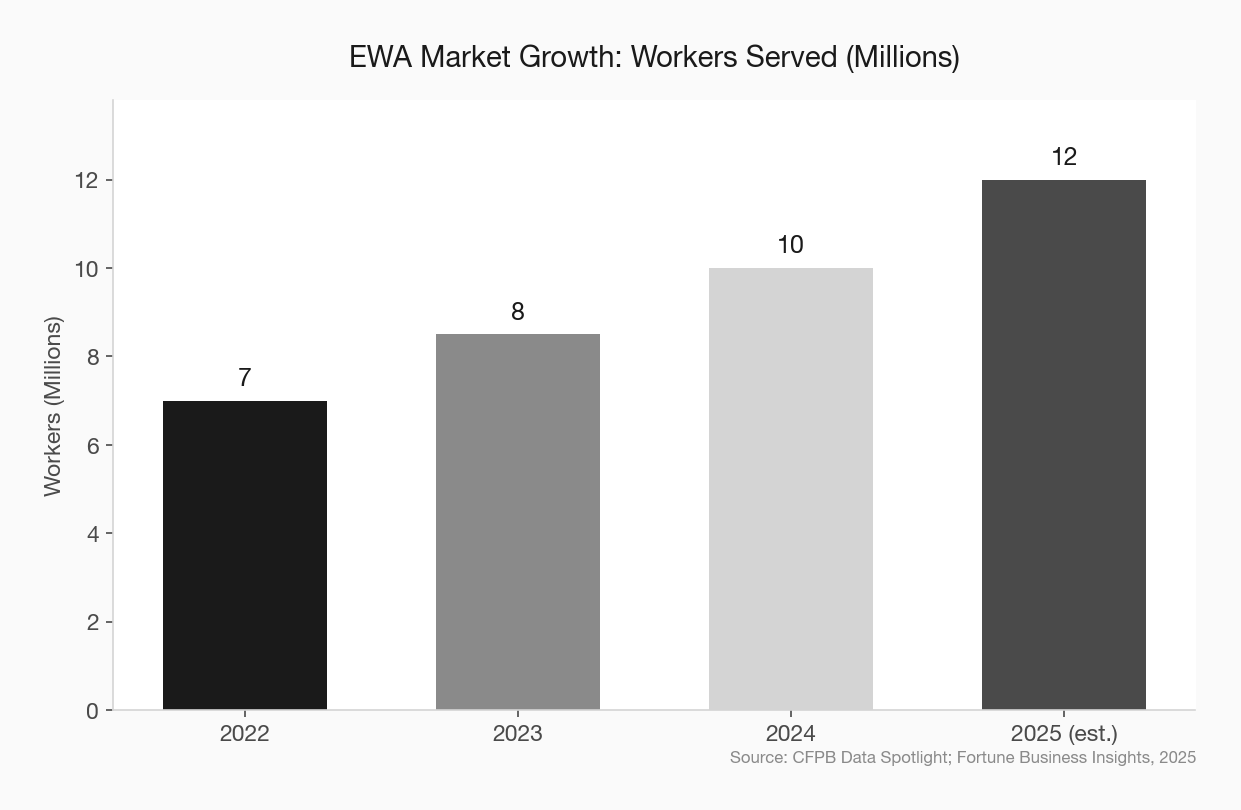

Earned wage access — the ability for workers to tap wages they’ve already earned before payday — is not a fringe benefit anymore. An estimated 10 million workers accessed roughly $32 billion through EWA platforms in 2024. DailyPay alone reported serving more than 6 million employees by the end of 2025. Two-thirds of employers who offer EWA say it makes the greatest day-to-day positive impact of any benefit they provide — outranking 401(k) plans, childcare benefits, and tuition reimbursement.

This is a product that has moved from novelty to infrastructure in about five years. And the deposit implications for community banks are real.

How EWA Actually Works — and Why It Threatens Your Deposit Base

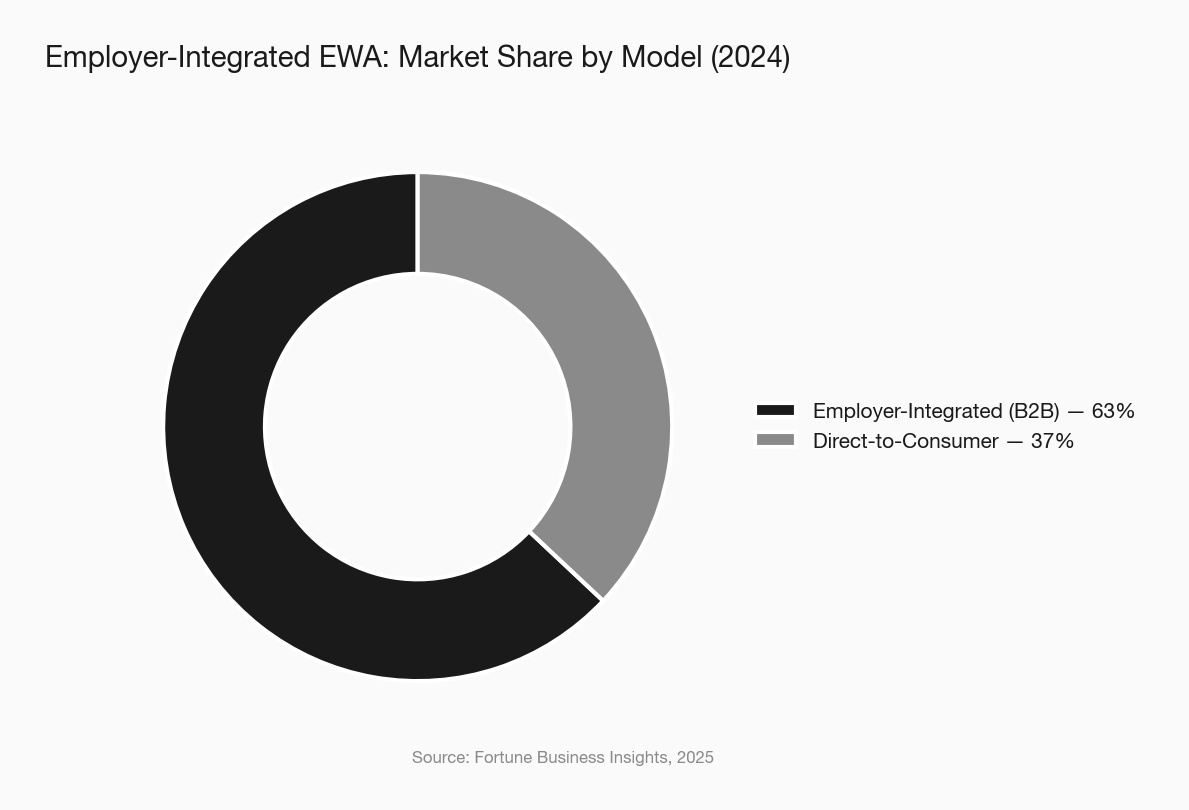

The employer-integrated EWA model — the dominant form, capturing 62.8% of the market in 2024 — works like this: a company like DailyPay integrates with your customer’s employer’s payroll and HR systems. When workers want access to wages they’ve already earned, they request a transfer through the DailyPay app. The money lands in a designated account, usually within minutes.

Here’s the catch: that designated account doesn’t have to be the worker’s community bank checking account. For the transfer to work instantly, many EWA platforms either maintain their own stored-value accounts or push workers toward fintech accounts — including Chime, which now offers its own EWA product to employers directly.

When a nurse at your local hospital starts pulling $200 advances through DailyPay three times a month, she’s training herself to think of DailyPay — not First National — as where her money lives in the short term. Over time, the direct deposit can follow. The average EWA user runs 27 transactions per year and accesses roughly $3,000 annually. That’s a lot of money moving through a pipe that bypasses your institution.

The December 2025 Regulatory Shift Changed Everything

For the last several years, EWA operated in a regulatory gray zone. The Biden-era CFPB proposed classifying EWA products as credit under the Truth in Lending Act — which would have imposed disclosure requirements, APR calculations, and compliance costs that might have slowed the industry’s growth.

In December 2025, the CFPB reversed that position. Its advisory opinion established that certain “covered” EWA products — those based on actual payroll data, using payroll deduction for repayment, with no credit risk assessment and no recourse against the worker if deductions fall short — are not credit under TILA and Regulation Z.

That ruling was a green light. EWA providers now have regulatory clarity they didn’t have before. Expect the market to accelerate. Six states passed new EWA regulations in 2025; more will follow in 2026 as the legal framework firms up state by state.

There’s a caveat: the New York Attorney General filed suit against DailyPay and MoneyLion in April 2025, alleging their products amounted to illegal payday loans under state law. That case isn’t resolved, and it signals that state-level enforcement remains unpredictable even as federal regulatory risk recedes. But for most community banks operating in markets outside New York, the takeaway is simple: EWA just got a clearer runway.

The Employer Relationship Is the Battleground

Community banks have always competed on relationships. But most of those relationships run customer-to-bank. The EWA threat operates on a different axis: employer-to-worker.

When DailyPay or Payactiv signs a contract with the hospital, the school district, or the regional food distributor in your market, they gain access to an entire workforce at once. They don’t have to convince each worker individually — the employer does it for them, often during onboarding.

community bank small business and employer banking strategy

This is important because community banks often have deep relationships with local employers. Many already hold the business accounts for the hospital, the food distributor, and the school district. But holding the business deposit relationship does not protect the personal deposit relationships of those businesses’ employees — which is exactly where EWA operates.

If you’re a community banker and you haven’t thought about which large employers in your market are currently offering or evaluating EWA programs, now is the time to find out.

What Community Banks Should Do Right Now

There are three moves worth considering, in order of urgency.

1. Audit your employer relationships.

Start with the businesses that bank with you. Do you know which of them are currently offering EWA? Have any signed with DailyPay or Payactiv in the last 12 months? A single conversation with your business relationship manager can surface this. If a major local employer is about to onboard 500 workers onto a DailyPay program, your retail team should know before that happens — not six months after.

2. Get ahead of the conversation with key employers.

If an employer in your market is evaluating EWA programs, you have a window. Introduce them to bank-native alternatives before a third party signs the deal. A company called Clockout — which won the ICBA ThinkTECH Accelerator All-Heart Award in August 2025 — is specifically building EWA infrastructure for community banks, with integrations through Q2 and Jack Henry that can go live in about 10 days.

fintech partnership due diligence community bank

The pitch to the employer is simple: you can offer your employees earned wage access through a product that keeps their banking relationship local. The community bank provides the service; the workers keep their primary account. No third-party app, no account migration risk.

3. Protect the direct deposit relationship.

If employees in your market are already using third-party EWA products, you’re fighting a retention battle, not a prevention battle — which is harder. The most effective tools here are the same ones that have always worked: direct deposit incentives, overdraft-alternative products that reduce the perceived need for EWA, and relationship-based outreach that makes switching feel costly.

community bank deposit strategy rate competition

The workers who use EWA most frequently — 27 transactions a year, average advance of $106 — are doing so because they’re cash-flow constrained between paydays. If your institution offers a small-dollar line of credit, a paycheck advance program, or a fee-free overdraft buffer, make sure those customers know about it. The EWA providers aren’t winning because they’re better banks. They’re winning because they showed up when traditional banking felt unavailable.

The Quiet Deposit Drain Is Already Underway

The reason EWA is a harder problem than most fintech threats is that it’s invisible at first. You don’t lose the account — you lose the primacy of the account. The worker keeps their checking account at your institution, but their direct deposit migrates to a DailyPay account or a Chime account because that’s where their daily financial activity now happens.

community bank marketing metrics deposit acquisition

You won’t see it in your core system as an account closure. You’ll see it as declining average daily balances, lower debit card transaction volume, and reduced overdraft fee income. By the time those trends are visible in your data, the behavioral shift has already happened.

The employers doing the most hiring in your market — hospitals, schools, distribution centers, retail chains — are exactly the employers most likely to be evaluating EWA programs right now. These aren’t abstract threats. They’re playing out in your backyard.

The community banks that will hold their deposit base through the EWA era are the ones that treat employer relationships as a retail banking strategy, not just a commercial banking one. The employer is the distribution channel. If someone else controls the channel, they’ll eventually control the customer.