Embedded Finance Is Already in Your Market — Here's Where to Look

Shopify Capital, Toast, and ServiceTitan are lending to your business customers inside workflows you've never touched. Here's how to find them—and respond.

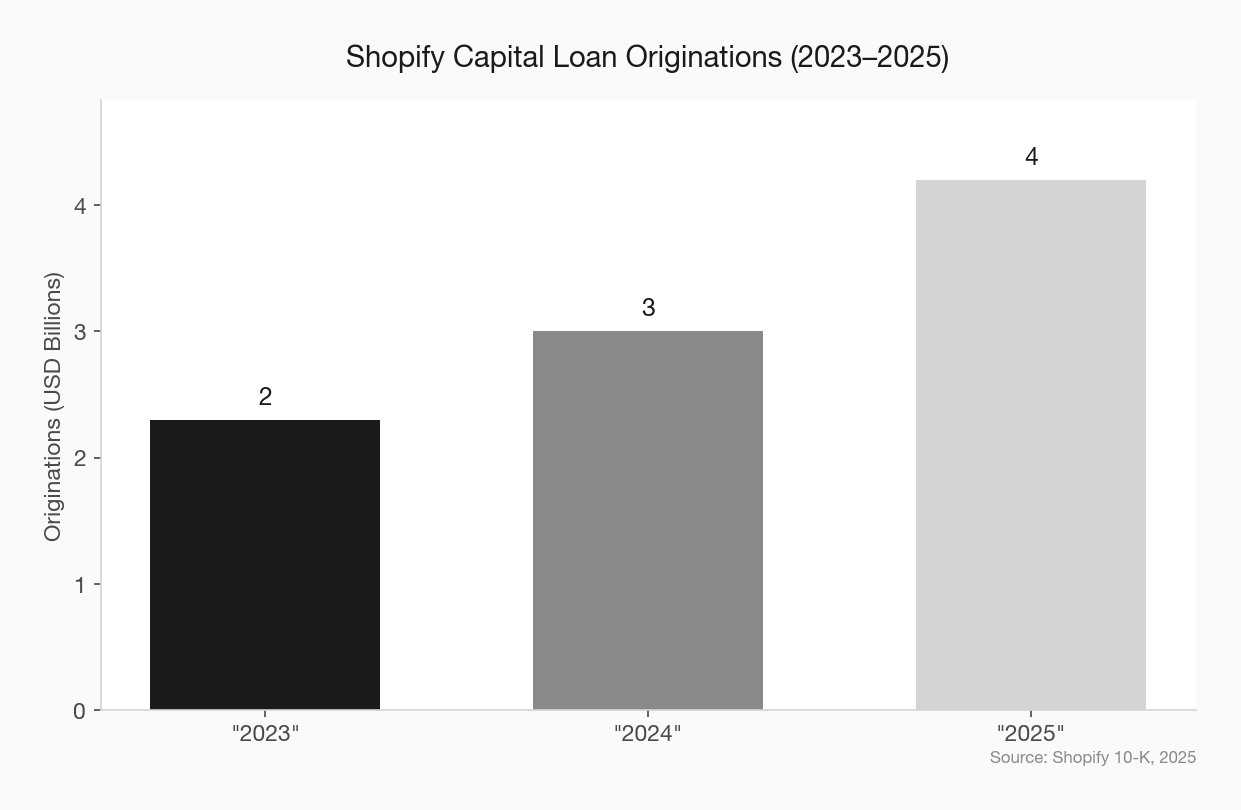

Shopify bought $4.2 billion in merchant loans and cash advances in 2025. That’s not a projection — it’s in their 10-K. It’s up 40% from the year before. And almost none of that money went through a bank.

That’s the embedded finance story in one number. Non-financial platforms are originating billions in credit by inserting a loan button into the software their customers already use every day. No branch. No loan officer. No rate sheet to compare. The customer never had to choose.

If you run a community bank and you haven’t mapped where embedded lending is active in your footprint, you are losing business you don’t know you’re losing.

What Embedded Finance Actually Means in Practice

Embedded finance isn’t a concept — it’s already operational in your market. Here’s what it looks like in the real world:

The restaurant owner on Toast. Toast Capital offers restaurants same-day working capital loans funded directly from daily sales. Toast underwrites based on POS transaction data — data your bank doesn’t have. The restaurant owner doesn’t fill out a loan application. They click “accept” on an offer Toast pre-generated from their own sales history.

The HVAC contractor on ServiceTitan. In January 2025, ServiceTitan — the field management software used by plumbers, electricians, HVAC contractors, and roofers — expanded its fintech suite to include integrated financing through Wisetack. The contractor’s customer needs a $7,000 furnace replacement. ServiceTitan offers financing on the spot, through the technician’s tablet, with an approval rate the company claims reaches 94%. The loan closes before the job is done. The community bank that had a relationship with that contractor’s customer never got a call.

The e-commerce seller on Shopify. Shopify Capital has now disbursed over $5.1 billion cumulatively to merchants. Repayment comes as a percentage of daily sales — automatic, invisible, and frictionless. The underwriting is machine learning against real transaction data. A merchant who applied for a $50,000 line of credit at your bank six months ago may have already funded their inventory expansion through Shopify Capital last week.

The gig worker with the fintech deposit account. Starion Bank — a community bank based in North Dakota — partnered with DoorDash to launch Crimson, a deposit account embedded directly in the Dasher app. In just over three months, that single partnership added 3 million accounts and earned Starion an American Banker 2025 Innovation of the Year award. Most community banks are still debating whether gig workers are a target segment worth pursuing.

These aren’t hypothetical future scenarios. They are active, right now, in your market.

The Underwriting Advantage You Can’t Replicate Without Changing Your Model

The reason embedded lenders win isn’t that they’re better bankers. It’s that they have data you don’t.

Shopify knows what a merchant sold yesterday, what their return rate is, and how their revenue has trended over the past 36 months — all in real time. Toast knows what a restaurant’s Tuesday lunch service looks like compared to last November. ServiceTitan knows when an HVAC company’s seasonal revenue peaks. They use that data to underwrite in seconds, with higher approval rates, and to design repayment structures that match the borrower’s actual cash flow.

Your bank’s loan application — even a streamlined digital one — requires the borrower to assemble documents that reconstruct a picture the platform already has. It takes days where the platform takes minutes.

This isn’t a speed problem you can solve with a better loan origination system. It’s an information asymmetry problem. The platforms have relationship data on your customers that you don’t have access to.

Why This Threat Is Different From Standard Fintech Competition

When SoFi or Chime competes for your customers, there’s a moment of choice. The customer sees an ad, compares rates, and decides. You can compete at that moment — with relationship, with service quality, with local knowledge.

Embedded finance eliminates the moment of choice.

The HVAC contractor’s customer doesn’t decide between your bank and Wisetack. They decide whether to fix their furnace. The financing option appears as part of that decision, not as a separate financial decision at all. By the time you could have a conversation with that customer about a personal loan, the credit is already funded.

This is the core threat: you don’t lose these deals. You’re simply not present for them.

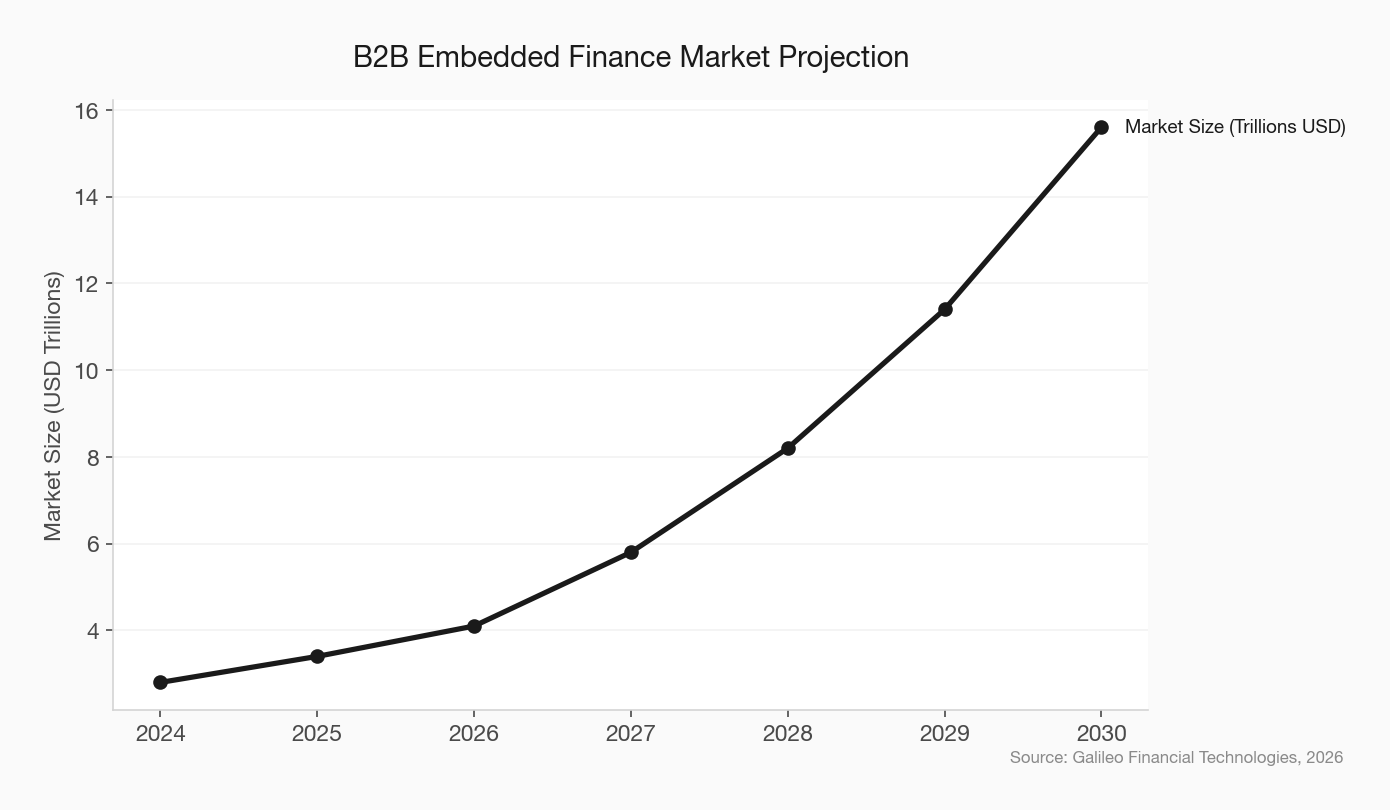

The B2B embedded finance market alone was estimated at $4.1 trillion in 2026 and is projected to reach $15.6 trillion by 2030. That’s not a share of the traditional lending market being contested — that’s a new market being built on top of existing business software, in workflows where banks have no natural presence.

How to Map Embedded Finance in Your Market

Before you can build a response, you need to know where the exposure is. This is a three-hour exercise, not a strategic initiative.

Start with your small business loan portfolio. Look at the industries with the highest concentration: restaurants, contractors, retail, healthcare, agriculture. For each industry, identify the dominant vertical software platforms. Restaurants on Toast or Aloha POS. Contractors on ServiceTitan, Jobber, or Housecall Pro. Retailers on Shopify or Square. These platforms all have or are building embedded finance products.

Ask your business customers which software they run their operations on. Most loan officers don’t know the answer. That’s the gap. The platforms your customers trust for their daily operations are the same ones positioning to displace you for their next working capital need.

Look for the platforms that already have banking relationships. Shopify Capital works through Celtic Bank. Toast Capital operates under a partnership structure. ServiceTitan integrates Wisetack, which is licensed as a lender. These are not fringe operations — they’re scaled fintech lenders with compliance infrastructure and institutional funding. understanding BaaS and bank partnership risk

Three Strategic Responses — in Order of Difficulty

1. Build awareness before you build a product.

The single most actionable thing a community bank can do right now is understand the platform landscape in its market. Which tools are your business customers using? Which of those tools have embedded lending? What terms are those lenders offering? A loan officer who knows that ServiceTitan merchants receive financing offers through Wisetack at rates between 8% and 30% APR is a loan officer who can have a different conversation.

This is a competitive intelligence task, not a technology initiative. community bank competitive intelligence fintech

2. Pursue platform partnerships — but vet them carefully.

Starion Bank didn’t build a gig economy product from scratch. They became the sponsor bank for an existing platform with a massive user base. That’s the embedded finance partnership model: the bank provides the charter, the deposit account infrastructure, and the regulatory compliance. The platform provides the distribution.

This model works. But it requires serious due diligence. After the Synapse collapse and the string of BaaS regulatory actions in 2024 and 2025, regulators are watching bank-fintech partnerships closely. BaaS risk community banks A partnership that generates deposit growth is not worth a consent order.

The banks building durable embedded finance partnerships are the ones that treat partner selection like a credit decision — with underwriting, ongoing monitoring, and defined exit conditions.

3. Defend the relationship layer by making it visible.

Where embedded lenders have a data advantage, community banks have a relationship advantage — but only if they use it.

The restaurant owner who took a Toast Capital advance at 28% APR would likely have preferred a $75,000 line of credit at your bank. The problem is that you didn’t offer it before they needed it. Proactive relationship management — knowing which of your business customers are growing, which have seasonal cash flow gaps, and which are the kinds of operators likely to use embedded lending as a shortcut — is the defense.

This is a retention strategy, not a technology strategy. It requires loan officers who know their customers’ businesses well enough to anticipate needs, not just respond to applications. community bank small business relationship banking

The Window Is Smaller Than You Think

A 2025 survey by Treasury Prime found that 100% of the 300 community bank decision-makers surveyed were exploring embedded finance as a strategic growth driver. The urgency is registering.

But registering isn’t acting. Roughly 27% of those institutions were still in “watch” mode — observing rather than engaging. That’s a reasonable posture for 2022. In 2026, with Shopify Capital growing 40% year-over-year and vertical SaaS platforms in every industry building or expanding embedded lending, watching is a strategy with a clear endpoint.

The community banks that will find success in this environment aren’t the ones who out-tech the platforms. They’re the ones who understand where the platforms operate in their markets, build the right partnerships, and deepen the relationship advantages that platforms structurally cannot replicate.

That starts with knowing what’s already in your market. Run the exercise. The answer might surprise you.

fintech partnership due diligence community bank community bank digital strategy small business