How One Community Bank Used AI to Cut Loan Processing Time by 40%

Hendricks County Bank halved underwriting time. Bankers Trust cut commercial loans from two weeks to five days. Here's how community banks are actually using AI in lending.

Hendricks County Bank and Trust, a community bank in Brownsburg, Indiana, had a problem every small lender knows well: underwriting a single small-business loan took five to six hours of manual work. Spreading financials, checking covenants, pulling documents, keying data — the same grind, loan after loan.

Then they deployed Abrigo’s Community Lending platform. Within a weekend of switching over, their underwriting time dropped by half. For some loans, it fell to a third of what it used to be. No new hires. No 18-month digital transformation initiative. One platform swap, one weekend, measurable results by Monday.

This is the AI story community banks need to hear — not the one about JPMorgan’s billion-dollar tech budget or Goldman’s proprietary machine learning models. The one about a bank in central Indiana that stopped doing things the slow way because a better tool finally existed at their price point.

The Lending Speed Gap Is Already a Competitive Problem

Community banks are getting slower at the exact moment borrowers expect faster. A 2025 Celent study commissioned by Zest AI found that 83% of lenders plan to increase their generative AI budgets in 2026, with 41% expecting increases above 5%. Two-thirds of lenders have already completed or will implement GenAI strategies by 2026.

Meanwhile, AI-native platforms like Casca are funding commercial loans up to 30 times faster than industry averages. Their document processing tools read 10,000 pages in five minutes — a task that would take a human analyst days.

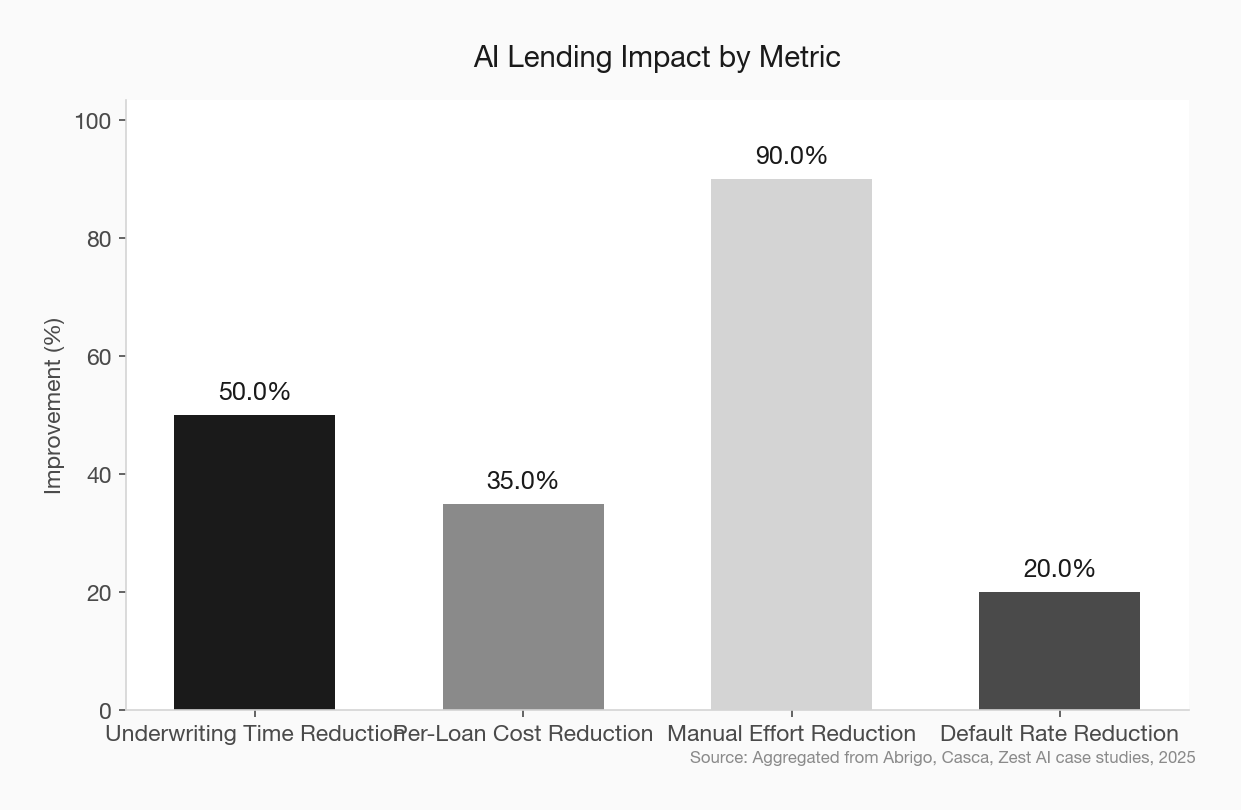

The institutions that reduced per-loan processing costs by 30-40% through AI automation now hold structural cost advantages that are difficult to reverse. Banks that haven’t deployed production-grade AI models by end of 2026 face a 15-20% cost disadvantage in consumer lending compared to AI-native competitors, according to industry analysis from Timvero.

That’s not a prediction. That’s a math problem.

What Hendricks County Bank Actually Did

Hendricks County Bank was one of the earliest adopters of Abrigo’s Community Lending platform, which launched in 2023. The implementation wasn’t a multi-year project with consultants and steering committees. They cut over in a single weekend.

The platform automates the most time-intensive parts of small-business underwriting: financial spreading, document collection, risk scoring, and decisioning for straightforward loans. Loan officers still make the final call on relationship-driven deals. But the hours of manual data entry and document shuffling that preceded every decision? Gone.

The results were immediate. Underwriting that took five to six hours per loan dropped to two to three hours, and in some cases even less. That’s not a marginal improvement — it’s the difference between a loan officer handling three applications per day versus five or six. community bank operational efficiency

Bankers Trust: From Two Weeks to Five Days

Hendricks County Bank isn’t the only community bank seeing these results. Bankers Trust, a $7 billion institution, used Abrigo’s loan origination system with AI-powered loan scoring to compress its commercial loan process for certain loans from two weeks to three to five days.

The key insight from both implementations: the AI isn’t replacing the relationship. It’s eliminating the paperwork that delays the relationship.

Community bankers spend decades building the judgment that makes their lending decisions better than an algorithm’s. The problem was never the decision — it was everything that had to happen before the decision could be made. Scanning documents, keying numbers into spreadsheets, waiting for departments to pass files back and forth. AI handles the friction. The banker handles the judgment.

The Three AI Applications That Actually Work for Community Banks

Not every AI tool is ready for a $500 million community bank. Some require data science teams. Others need clean data lakes that don’t exist in most core systems. But three applications are delivering measurable results right now, without requiring a technology overhaul.

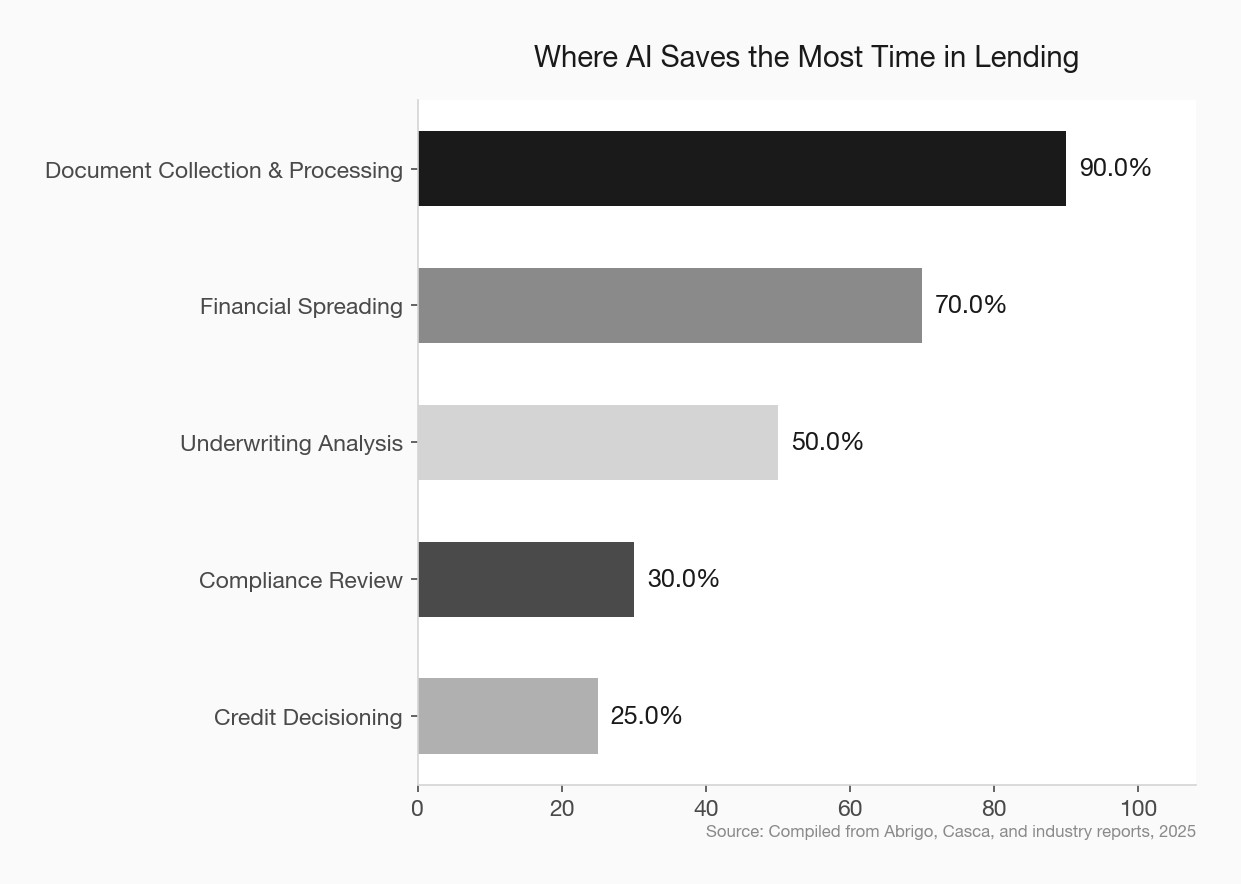

1. Automated Document Processing and Financial Spreading

This is the highest-ROI starting point. AI reads tax returns, bank statements, financial statements, and rent rolls — extracting data that loan officers currently key in by hand. Casca’s platform, used by banks including Live Oak and Huntington, claims to process up to 10,000 pages in five minutes and reduce manual back-office effort by 90%.

For a community bank processing 50 small-business loans per month, that’s hundreds of hours returned to loan officers for actual lending work. AI document processing for banks

2. AI-Powered Credit Scoring and Decisioning

Zest AI’s machine learning models deliver, on average, a 25% increase in approvals and a 20% reduction in defaults. That’s not a typo — more approvals and fewer losses simultaneously. The models achieve this by analyzing data patterns that traditional scorecards miss, particularly for thin-file borrowers who look risky on paper but aren’t.

Commonwealth Credit Union partnered with Zest AI and saw loan growth that outpaced industry norms, exceeding 14% in 2025. They’ve since launched the CU Lending Collective to help smaller institutions access the same technology. AI credit scoring community banking

3. Compliance and Review Automation

Abrigo’s Loan Review Assistant allows credit risk review staff to evaluate credit quality and document insights in minutes rather than days. Compliance teams using AI-assisted document analysis report spending 30% less time on manual reviews.

For community banks where compliance staff wear multiple hats, that time savings isn’t abstract — it’s the difference between staying current on reviews and falling behind.

The Vendor Problem Is Real — But It’s Changing

Here’s the honest part: community banks face a structural disadvantage in AI adoption. Three core service providers serve over 70% of depository institutions, and the ABA’s 2024 Core Platforms Survey reported overall satisfaction at just 3.19 out of 5, with innovation capabilities scoring even lower.

For most community banks, the AI tools available to them depend on what their core provider decides to build. And core providers have historically built for their largest clients first.

But the market is shifting. Abrigo, Casca, nCino, and Zest AI are all building specifically for community banks and credit unions. Casca raised $29 million in August 2025 specifically to scale its AI-native loan origination platform for smaller institutions. Their flagship customers — Live Oak Bank, Huntington National Bank, and Bankwell Bank — all invested in the round.

The tools exist. The question is whether your bank is evaluating them or waiting for your core provider to catch up. fintech vendor evaluation for community banks

What This Means for Your Bank

The 2025 BNY Voice of Community Banks Survey found that community banks growing their small business clientele were 49% more likely to invest in AI to improve operational efficiency. Growth-oriented banks aren’t waiting for perfect solutions. They’re deploying what works now and iterating.

Here’s what I’d tell any community bank CEO considering AI for lending:

Start with document processing. It’s the lowest-risk, highest-return application. Your loan officers are spending hours on data entry that a machine can do in minutes. Free them to do what they’re actually good at — building relationships and making judgment calls.

Don’t wait for your core provider. Evaluate standalone solutions from Abrigo, Casca, or nCino that can integrate with your existing systems. The banks seeing results aren’t waiting for permission from their core.

Set a measurable target. Hendricks County Bank measured hours per loan. Bankers Trust measured days to close. Pick your metric, benchmark it before you implement, and track it after. AI vendors will throw buzzwords at you. Demand numbers.

Accept that 80% automated is better than 0%. You’ll still need human judgment for complex deals. That’s fine. The goal isn’t full automation — it’s eliminating the manual work that makes your lending process slower and more expensive than it needs to be. community bank technology strategy

The Clock Is Running

The community banks that deployed AI in lending in 2024 and 2025 now hold cost advantages that will compound over time. Every month of faster loan processing means more loans closed, more borrowers served, and more revenue generated with the same staff.

The banks that wait until their core provider rolls out a feature in 2027 will be competing against institutions that have had two years of operational advantage. In small-business lending, where speed and relationships both matter, that gap is hard to close.

Hendricks County Bank didn’t need a data science team or a seven-figure technology budget. They needed a better tool and the willingness to adopt it over a weekend. The bar for entry is lower than most community bankers think. The cost of waiting is higher than most realize. AI adoption timeline for community banks