How to Evaluate a Fintech Partnership Without Getting Burned

Community banks are signing fintech deals without adequate due diligence. After Synapse, Evolve, and Blue Ridge, here's the evaluation framework that matters.

The wreckage from bad fintech partnerships is no longer hypothetical. When Synapse Financial Technologies collapsed in April 2024, more than 100,000 people lost access to over $265 million in deposits spread across four partner banks. The bankruptcy trustee estimated a shortfall between $65 million and $95 million — money that was supposed to be in accounts at Evolve Bank & Trust, Lineage Bank, AMG National Trust, and American Bank. The CFPB eventually allocated $46.2 million from its Civil Penalty Fund to reimburse affected customers. By then, the reputational damage to every bank involved was already done.

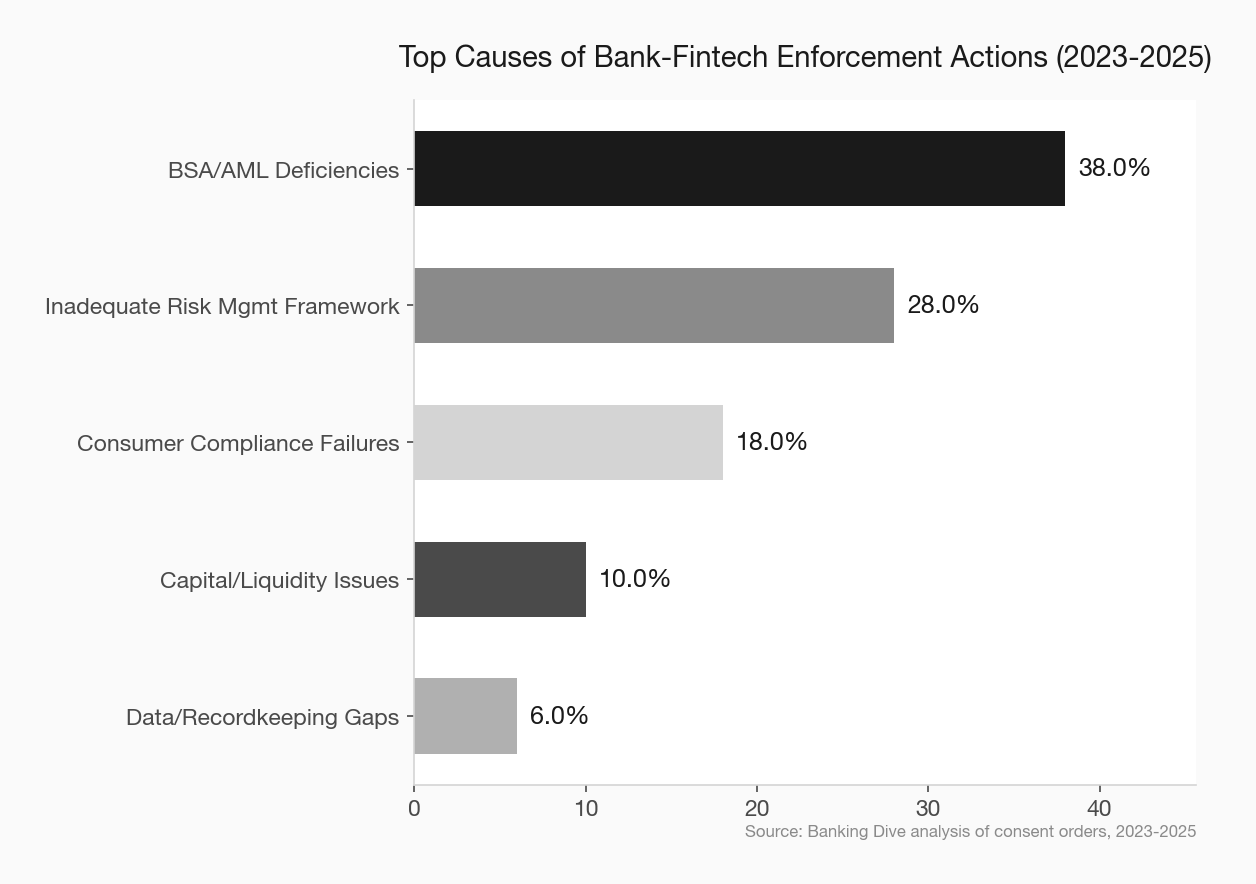

Synapse was the loudest explosion, but it wasn’t isolated. Blue Ridge Bank entered 2024 under a consent order after the OCC found it in “troubled condition” following its banking-as-a-service venture. Evolve Bank caught a cease-and-desist from the Federal Reserve for deficiencies in anti-money laundering, risk management, and consumer compliance — all tied to its fintech relationships. Lineage Bank, Piermont Bank, Sutton Bank, Cross River Bank, and First Fed Bank have all faced enforcement actions over the past two years.

The pattern is clear. Community banks that treated fintech partnerships as plug-and-play revenue found out the hard way that regulators hold the bank — not the fintech — accountable for everything.

The Partnership Landscape Right Now

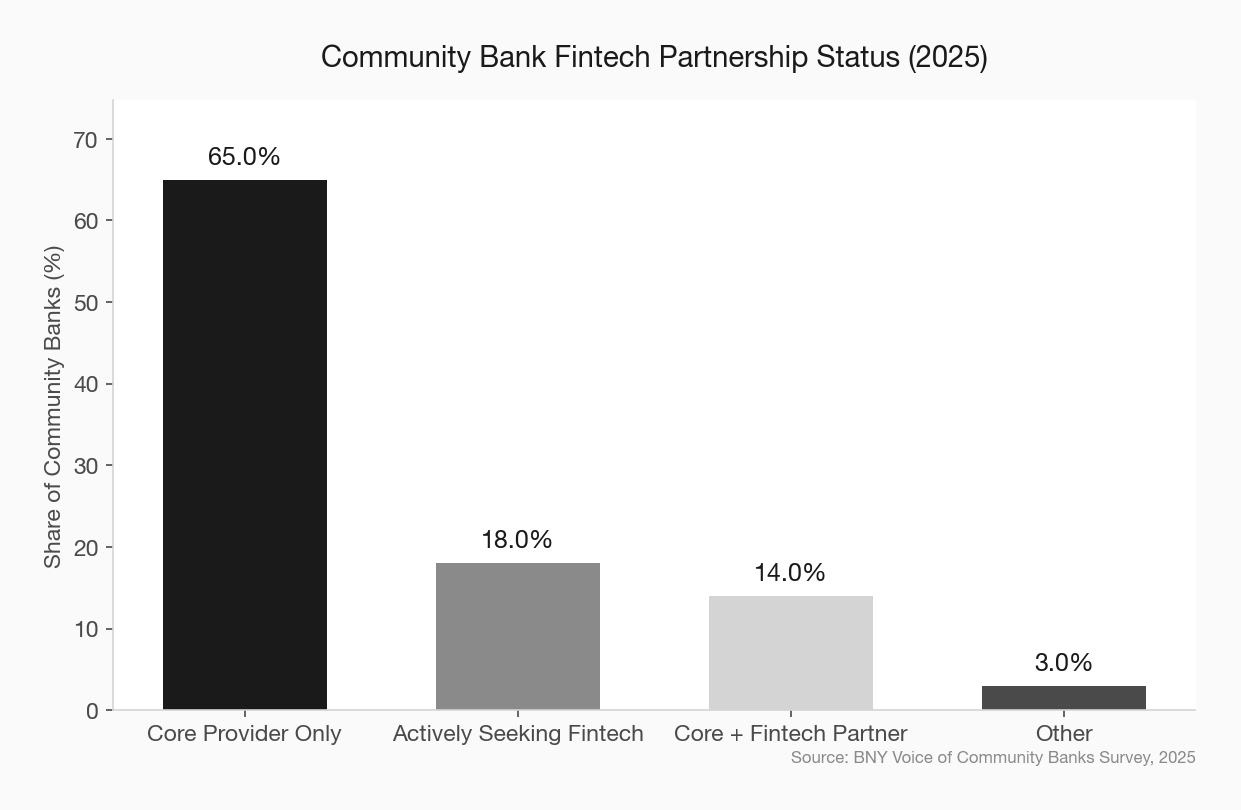

Nearly two-thirds of community banks have partnered with at least one fintech in the past four years, according to the 2025 BNY Voice of Community Banks Survey. Another 18% are actively seeking partnerships. The demand side isn’t slowing down — fintech firms have captured roughly 25% of market share in certain banking segments, and community banks know they need to keep pace.

But the regulatory environment has shifted beneath the opportunity. The interagency guidance on third-party risk management, finalized in June 2023 by the FDIC, OCC, and Federal Reserve, made one thing explicit: fintech partnerships where the fintech interacts directly with end customers are squarely “in scope” for full risk management requirements. That means the same due diligence you’d apply to a core processor now applies to a fintech partner offering deposit products through your charter.

And yet, a survey of compliance professionals found that 90% of sponsor banks still struggle with compliance in their fintech relationships. The gap between what regulators expect and what most community banks actually do is where consent orders live.

Where Banks Get Burned

The failures aren’t random. They cluster around a few predictable mistakes.

Treating the fintech like a vendor instead of an extension of your bank

When a fintech uses your charter to offer deposit accounts, loans, or payment services, regulators view those customers as your customers. The fintech’s compliance failures are your compliance failures. Blue Ridge Bank learned this when the OCC found deficiencies in its BSA/AML program that originated in its BaaS relationships.

Most community banks have vendor management programs built for their core processor and a handful of service providers. Those programs aren’t designed for the complexity of a fintech that’s originating accounts, handling KYC, and touching consumer funds in real time. You need a fundamentally different oversight model.

Inadequate contract terms

The contract is the only thing standing between your bank and the fintech’s bad behavior. Too many community banks sign agreements that lack clear data ownership provisions, audit rights, subcontractor visibility, and termination clauses that actually work.

In the Synapse case, partner banks couldn’t access Synapse’s ledger data after the bankruptcy filing. That’s a contract failure as much as a technology failure. If your agreement doesn’t give you independent access to reconciliation data at all times — not just during normal operations — you’re exposed.

No ongoing monitoring

Due diligence isn’t a one-time event at contract signing. It’s a continuous process. The banks that ended up under consent orders almost universally failed at ongoing monitoring — they didn’t catch deteriorating financial conditions, expanding risk profiles, or compliance drift until regulators flagged it.

The Evolve Bank enforcement action specifically cited the bank’s failure to “quickly identify and report risk exposures related to fintech partners, programs, or services.” The Fed required Evolve to submit an enhanced risk management framework with procedures for identifying risk on an ongoing basis — exactly the kind of program that should have been in place before the first fintech partnership was signed.

The Evaluation Framework That Actually Works

Here’s a practical framework for evaluating a fintech partnership. It’s built on the interagency guidance, the FDIC’s fintech due diligence guide, and the lessons from every consent order published in the past two years. FDIC guidance on fintech due diligence

1. Business Viability and Financial Condition

Before you evaluate the technology, evaluate the company. Most community banks skip this step or treat it as a formality.

What to assess:

- Funding runway and burn rate. If the fintech is venture-backed, how much capital do they have and how fast are they spending it? A fintech that runs out of money mid-contract creates the same operational risk as a technology failure. Ask for audited financials or, at minimum, reviewed statements.

- Revenue concentration. How dependent is the fintech on a single bank partner or a single revenue stream? If you’re their only or primary bank partner, their failure is your operational crisis.

- Management team stability. High C-suite turnover at a fintech is a leading indicator of strategic instability. Look at LinkedIn. Talk to references. Ask who left in the past 12 months and why.

- Client references from similar-sized banks. A fintech that works well with a $10 billion bank may not have the support model for a $500 million community bank. Talk to institutions your size.

2. Compliance Architecture

This is where most evaluations either go too shallow or get overwhelmed by checkbox exercises. Focus on structure, not just policy documents.

What to assess:

- Who owns compliance at the fintech? Is there a dedicated compliance officer, or is compliance a side responsibility of the general counsel? A fintech that doesn’t have a standalone compliance function is telling you where it ranks on their priority list.

- BSA/AML program design. How does the fintech handle KYC, transaction monitoring, and suspicious activity reporting? Does their program integrate with your bank’s BSA systems, or does it operate as a black box? After the Evolve enforcement action, regulators have zero patience for “the fintech handles it” as an answer.

- Consumer complaint handling. Where do consumer complaints go? How are they tracked? Who responds? Regulators look at complaint volumes and response quality as a proxy for consumer harm risk.

- Marketing and advertising review. Every piece of marketing the fintech puts out using your charter needs to comply with UDAP and fair lending requirements. Who reviews it? How fast? What’s the escalation path when something goes out that shouldn’t?

The STARC framework, introduced by the Coalition for Financial Ecosystem Standards in March 2025, provides a useful benchmark here. Think of it as the SOC 2 equivalent for fintech compliance. STARC includes 54 measurable standards across six core areas: BSA/AML, compliance management systems, third-party risk management, operational risk, complaint handling, and marketing compliance. If your fintech partner has STARC certification — or is willing to pursue it — that’s a meaningful signal. If they’ve never heard of it, that tells you something too. STARC framework for fintech partnerships

3. Technology and Operational Resilience

Technology due diligence for a fintech partnership goes beyond reviewing a SOC 2 report. You need to understand how the technology works in failure scenarios, not just in demos.

What to assess:

- Data reconciliation. How does the fintech reconcile customer funds with your bank’s ledger? How often? What happens when there’s a discrepancy? The Synapse collapse was fundamentally a reconciliation failure — the middleware’s internal ledger didn’t match what the banks held. Your reconciliation process needs to be independent of the fintech’s systems.

- Disaster recovery and business continuity. What’s the fintech’s recovery time objective? Have they tested it? Can you verify the test results? A fintech that can’t demonstrate a tested DR plan is a fintech you shouldn’t partner with.

- API architecture and data portability. If you need to terminate the relationship, can you extract your customer data cleanly? How long does that take? What format does it come in? The banks caught in the Synapse bankruptcy couldn’t access their own customer records for weeks.

- Subcontractor and fourth-party risk. Who does the fintech rely on? Cloud providers, identity verification vendors, payment processors — your risk surface includes their entire supply chain. Map it.

4. Contract Structure

The contract is your last line of defense. Treat it that way.

Non-negotiable terms:

- Independent audit rights with no advance notice requirement. You need the ability to audit the fintech’s operations, compliance, and financials at any time — not just during scheduled reviews.

- Direct data access. Your bank must have independent, real-time access to all customer data and reconciliation records. Not through the fintech’s portal. Through a separate, bank-controlled channel.

- Subcontractor approval. The fintech shouldn’t be able to change critical subcontractors without your written consent. Their supply chain is your risk.

- Termination without cause with a reasonable wind-down period. If the relationship isn’t working — or if your examiner raises concerns — you need an exit that doesn’t strand your customers.

- Indemnification that means something. The fintech should indemnify your bank for losses arising from their compliance failures, data breaches, or operational errors. But indemnification from a startup with 18 months of runway is a paper promise. Consider requiring escrow or insurance.

- Regulatory cooperation clause. The fintech must agree to cooperate with your regulators during examinations — including providing documents, access to personnel, and on-site inspection rights.

5. Ongoing Monitoring Program

The evaluation doesn’t end at contract signing. Build a monitoring program before you sign the deal.

What ongoing monitoring looks like:

- Quarterly financial reviews of the fintech’s condition. Set triggers for what constitutes a material change that requires board notification.

- Monthly compliance reporting that includes complaint volumes, SAR filing data, marketing review activity, and any regulatory inquiries the fintech has received.

- Annual on-site reviews of the fintech’s operations. This is non-negotiable for any fintech that touches customer deposits or loan origination.

- Real-time transaction monitoring integration. Your BSA team needs to see the same data the fintech sees — not a filtered summary three days later.

- Board reporting. Your board should receive a quarterly summary of every fintech partnership’s performance, risk metrics, and any issues identified. The Fed’s enforcement action against Evolve specifically required board-level written approval before onboarding new fintech partners. Treat that as the standard, not the exception.

interagency guidance on third-party risk management

The Red Flags That Should Kill a Deal

Not every fintech partnership is worth saving through negotiation. Here are the signals that should end your evaluation:

- The fintech resists audit rights or data access provisions. If they won’t let you look under the hood, there’s something under the hood.

- No audited or reviewed financial statements. A fintech asking for access to your charter while refusing to share financials is a non-starter.

- Compliance is “handled by outside counsel.” Compliance needs to be embedded in operations, not outsourced to a law firm that reviews things quarterly.

- They can’t explain their reconciliation process in plain language. If the fintech can’t clearly describe how customer funds move, how they’re tracked, and how discrepancies are resolved, walk away.

- High customer complaint volume with no remediation evidence. Check the CFPB complaint database. If the fintech’s partner products show elevated complaints, that’s your risk.

- They’re growing faster than their compliance infrastructure. Rapid customer acquisition with a two-person compliance team is a consent order waiting to happen.

how to assess fintech compliance readiness

What Smart Community Banks Are Doing Differently

The community banks getting fintech partnerships right share a few characteristics. They hire or designate a fintech relationship manager — someone whose job is partnership oversight, not just vendor management. They build the monitoring infrastructure before signing the deal, not after the first exam finding. They involve compliance and legal from the first conversation, not at contract review. And they treat the fintech partner’s customers as their own from day one.

The FDIC, OCC, and Fed have made their expectations clear. The interagency guidance, the enforcement actions, and the STARC framework all point in the same direction: the bank owns the risk. Full stop. A fintech partner can bring innovation, speed, and new customer segments — but only if your evaluation process is built to identify the ones that enhance your institution rather than endanger it. community bank fintech partnership case studies

The banks that got burned over the past two years didn’t fail because they partnered with fintechs. They failed because they partnered without asking hard questions, demanding real answers, and building oversight systems that matched the risk they were taking on. The opportunity is real. The due diligence has to be equally real.

building a fintech partnership oversight program