Online Account Opening: Why Most Community Banks Still Get It Wrong

Over half of community bank account opening applications are abandoned. Identity verification and funding are the culprits. Here's how to fix both.

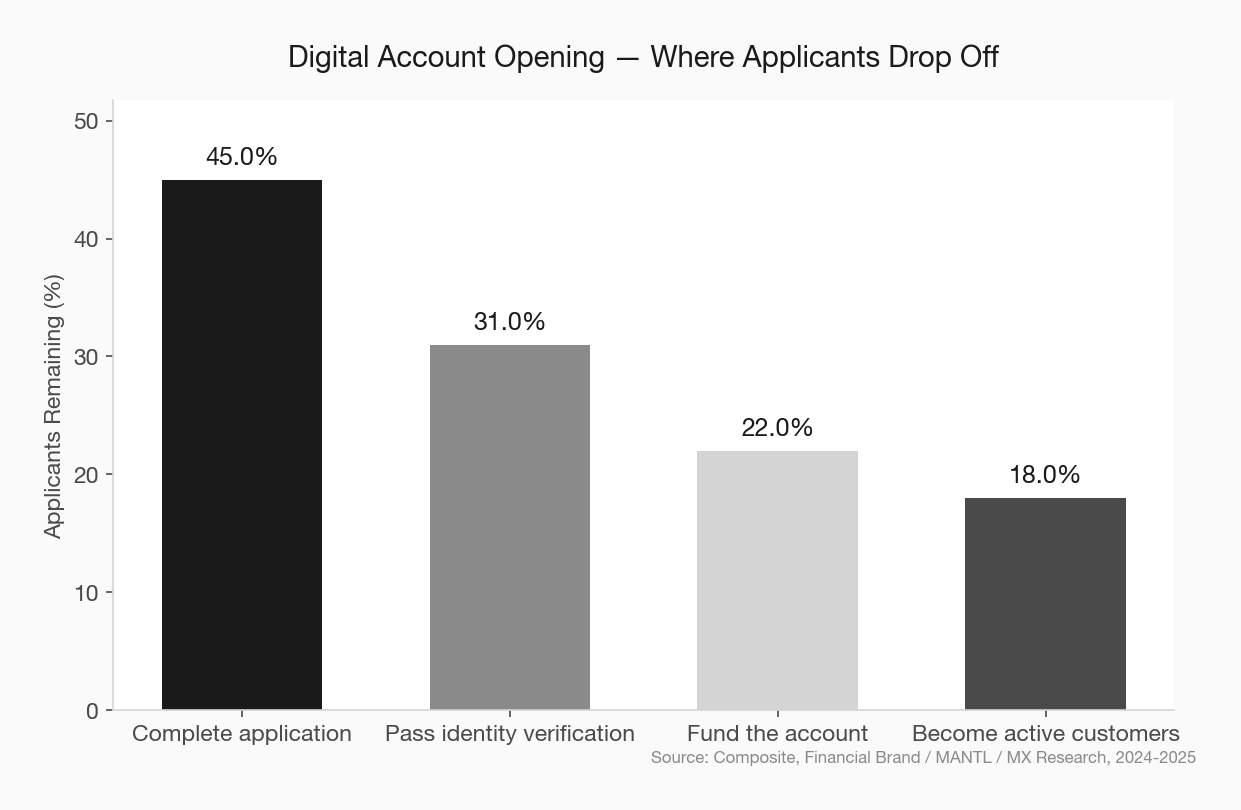

More than half of all digital account applications at traditional banks are abandoned before completion. That’s not a technology problem. That’s a design problem — and it’s costing community banks customers they’ve already earned.

Someone landing on your account opening page has already decided to give you a shot. They found you, they compared you to someone else, and they clicked “Open an Account.” The fact that more than half of them leave without finishing isn’t a sign that they changed their minds about you. It’s a sign that you made the process harder than they were willing to tolerate.

There are two places where community banks lose people at a disproportionate rate: identity verification and account funding. Fix those two steps and you can double your conversion rate without rebuilding your entire platform.

Why Abandonment Is Higher Than You Think

If your digital account opening takes longer than five minutes, you’re losing applicants. Not some of them — a lot of them. Research consistently shows abandonment exceeds 50% when a process crosses the five-minute mark, and for mobile users, the threshold drops to three minutes.

Here’s the uncomfortable part: 80% of banks say their own account opening process takes longer than five minutes. Nearly a third take longer than ten.

Most community banks measure this badly or not at all. They track how many people started an application and how many funded accounts they ended up with, but they don’t look at where in the process people dropped off. That missing middle is where the revenue is.

The Identity Verification Problem

Identity verification is the single biggest friction point in digital account opening, and most community banks are still doing it wrong.

KBA Is a Dead End

Knowledge-based authentication — those questions about your previous address, your first car, or which street you lived on in 2003 — was supposed to confirm identity. In practice, it mostly just stops legitimate applicants. According to Gartner research, KBA failures are disproportionately experienced by real customers who can’t remember answers to obscure questions, while fraudsters have become increasingly good at answering them using data harvested from breaches and social media.

The result is a verification method that’s simultaneously too strict for honest customers and too easy for bad actors. It’s a bad trade at both ends.

Documentary CIP Creates a 29% Drop in Conversion

Some community banks still require documentary Customer Identification Program (CIP) verification — collecting physical ID images, sometimes requiring a branch visit to finalize. Research from Cornerstone Advisors found that documentary CIP alone leads to a 29% reduction in conversion rates. For a modest reduction in fraud risk.

The math doesn’t support it. If you’re losing three in ten applicants to gain a marginal security benefit, you’re paying far too high a price — especially when modern biometric and database-backed identity solutions can provide equivalent or better fraud detection without the friction.

The 2025 Regulatory Update Worth Knowing

A rule finalized in June 2025 now allows certain financial institutions to collect a taxpayer identification number from a reliable third-party source rather than directly from the customer before account opening. That change matters because it removes one of the most common points of manual data entry in the application flow — and manual data entry is where many legitimate applicants give up or make errors that kick them to manual review.

regulatory changes community bank digital onboarding 2025

If your platform hasn’t been updated to reflect this, your vendor needs a call.

What Works Instead

Modern identity verification uses document capture (a photo of a government ID) combined with a selfie and a liveness check, cross-referenced against third-party databases. The process takes under 90 seconds and produces better fraud signals than KBA. Risk-scoring engines can then route low-risk applications directly to instant approval, flagging only genuinely suspicious applications for human review. The result is a system that’s faster for the applicant and more accurate for the bank.

The Funding Problem

Even if your identity verification is solid, you can still lose a significant percentage of applicants at the funding step — and most community banks are.

Micro-Deposits Are Killing Your Conversions

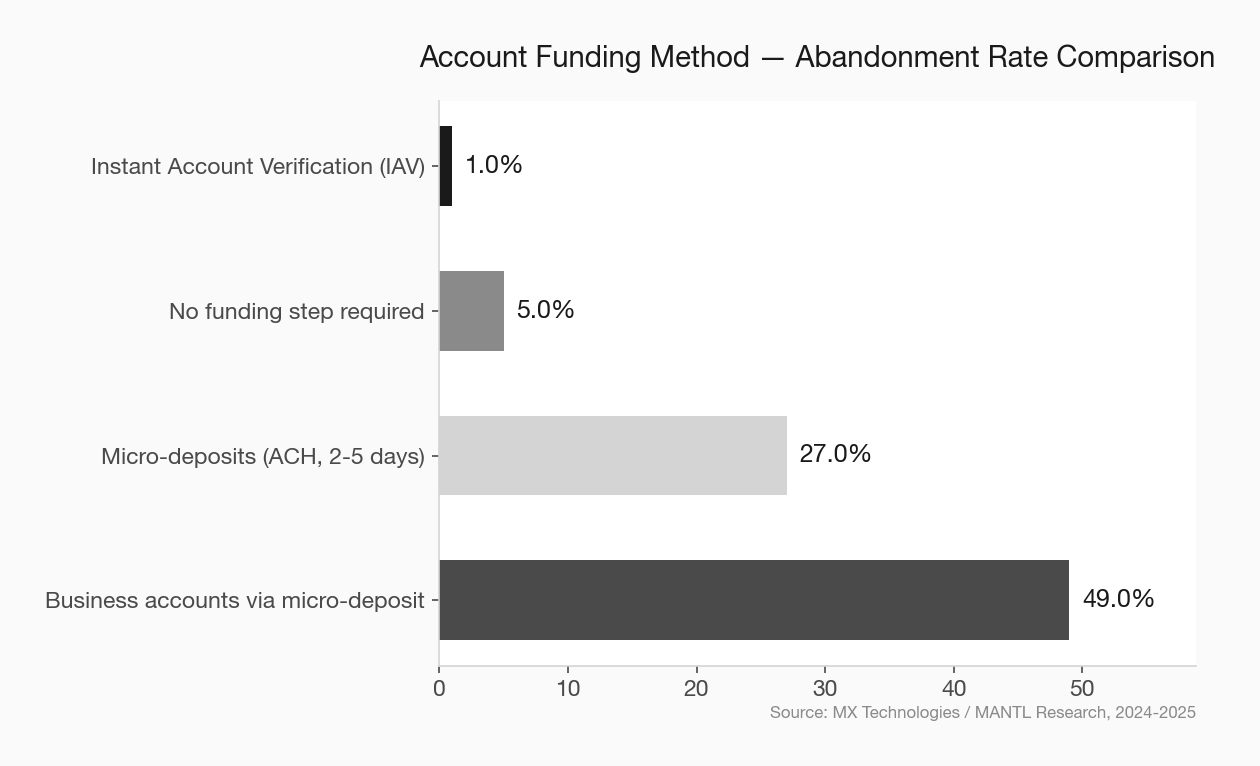

The traditional method for verifying an external funding account is micro-deposits: the bank sends two small transactions to the customer’s external account, the customer logs in to that account, finds the amounts, and enters them to confirm ownership. This process takes 2-5 business days.

The abandonment data is stark. Research from MX found that institutions requiring micro-deposits for ACH funding see a 27% abandonment rate at that step. Institutions that skip micro-deposits see 13%. For business accounts, the drop-off can reach 49%.

You’re asking someone who has already spent five minutes on your application to come back in three to five days to finish what they started. Most of them don’t.

Instant Account Verification Changes the Economics

Instant Account Verification (IAV) — where the applicant logs into their existing bank through a secure connection and grants temporary read access for verification — eliminates the waiting period. Verification happens in 10-30 seconds. MX data shows the onboarding drop-off rate for IAV is as low as 1%.

The per-transaction cost of IAV is roughly double that of micro-deposits. It doesn’t matter. If micro-deposits cost you 27% of your applicants, you’re paying far more in lost accounts than you’re saving on verification fees. instant account verification community bank funding options

FedNow and RTP rails have also made real-time micro-deposit confirmation possible — meaning even if you stay on the deposit-based path, you can now do it in seconds rather than days. If your core or platform doesn’t support this yet, it should be on your next vendor conversation list.

What “Fast Enough” Actually Looks Like

The industry benchmark for a well-designed digital account opening experience is under five minutes from start to funded. The best platforms — optimized for low friction — regularly achieve two to three minutes.

MANTL, a digital account opening platform used by community banks and credit unions, reports that the average application on their platform is completed in two minutes and 37 seconds. Their customers see a 3.8x improvement in conversion rates compared to their prior processes. That’s not a marginal improvement. That’s a different business.

digital account opening platforms community banks comparison

To be clear: this isn’t about which software you use. It’s about whether your current process is designed around the applicant’s experience or around your internal workflow. The two are not the same thing.

A Community Bank That Got It Right

Midwest BankCentre, a St. Louis-based community bank, launched a digital-only brand called Rising Bank specifically to compete for deposits beyond their geographic footprint. Their goal was $100 million in new deposits within twelve months.

They hit $75 million in ten weeks. They finished the year at $130 million.

Their account opening process was designed to take three minutes. Their application-to-funded conversion rate was 48% — roughly double the community bank average. The bank estimated that without Rising Bank, achieving the same deposit volume through branch expansion would have required building ten new locations.

That result isn’t just about technology. It’s about designing the process with conversion in mind from the first screen to the last.

community bank digital-only brand strategy deposit growth

What You Don’t Need

You don’t need a core conversion to fix this. You don’t need a full digital transformation initiative. You don’t need to rebuild your website or hire a UX team.

You need to:

- Audit your current drop-off rate at each step of your application flow

- Replace KBA with document-based biometric identity verification

- Switch from micro-deposits to instant account verification for external funding

- Set a five-minute completion target and measure against it monthly

Most community banks can make these changes through their existing digital account opening vendor or by switching to a platform that already has them built in. The lift is lower than most executives assume.

The 70% abandonment rate isn’t inevitable. It’s a design choice — just not one that was made intentionally.

digital account opening vendors community bank evaluation

The Closer

Every applicant you lose at identity verification or funding was a customer who wanted to bank with you. They raised their hand. The failure isn’t in your marketing or your rates or your location — it’s in the 47 seconds after they clicked “Apply” when you asked them to answer a question about a car they owned fifteen years ago.

That’s fixable. And it’s worth fixing before your next branching strategy discussion, your next technology roadmap, or your next board retreat. Because none of those moves will matter much if you can’t convert the people who are already trying to say yes.