PayPal and Venmo Are Already Your Competitors. Start Acting Like It.

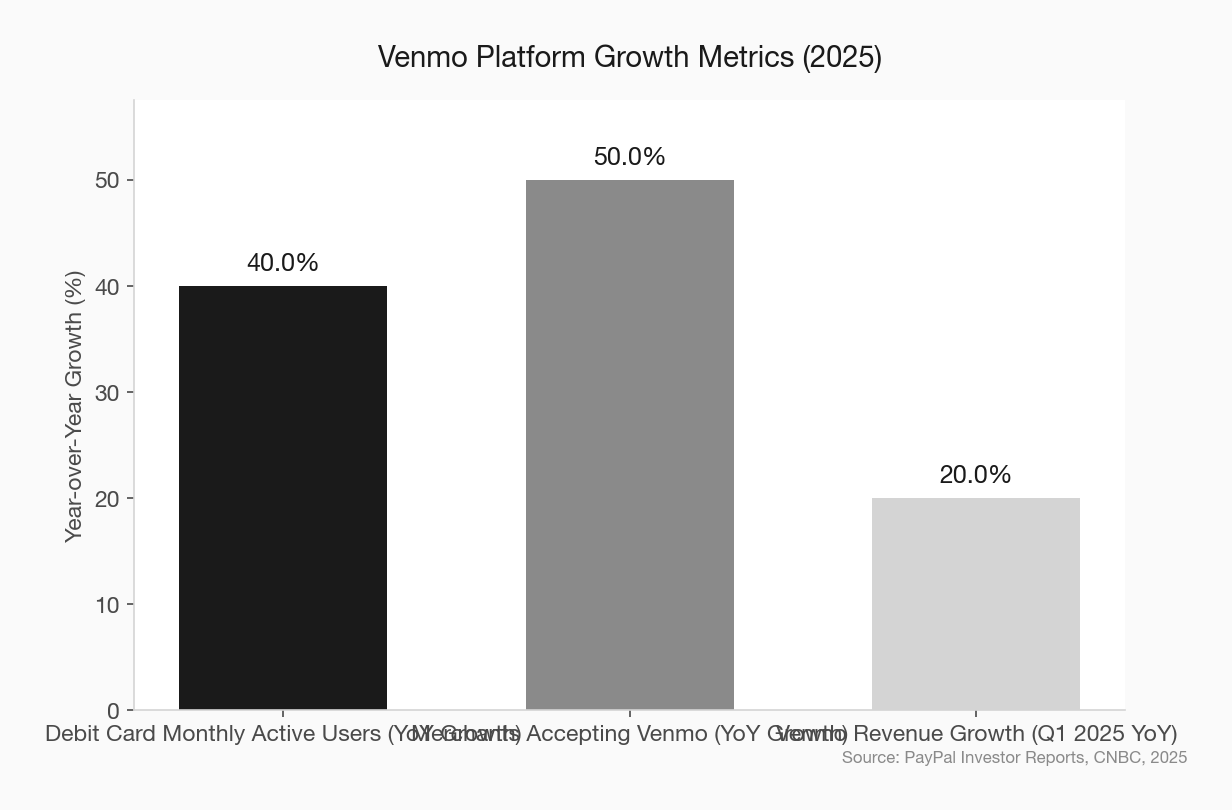

With 95 million active Venmo users and a debit card growing 40% annually, PayPal isn't just a payments app. It's actively building the primary banking relationship community banks assume they own.

Venmo processed payments for 95.4 million active U.S. accounts last year. Its debit card grew monthly active cardholders by 40% in a single quarter. Merchants accepting Venmo at checkout grew more than 50% year-over-year. You can now pay with Venmo at Uber, Instacart, TikTok Shop, and Domino’s — or anywhere that takes Mastercard, because the debit card works everywhere.

This is not a peer-to-peer payments app anymore. This is a financial platform with a stated goal of becoming the center of its customers’ financial lives. PayPal’s CEO has said that explicitly to investors.

Community banks that still think of Venmo as the thing college kids use to split pizza have fundamentally misread what’s happening.

Payments Are the Front Door to the Relationship

Here’s the core problem: the customer who pays with Venmo is not thinking about their community bank when they pay. They’re thinking about their Venmo balance, their Venmo rewards, and whether their Venmo debit card gets them cash back at that merchant.

That’s not a small thing. Payment frequency is the highest-touch interaction most customers have with any financial institution. The average consumer makes 40+ debit transactions per month. Every one of those transactions is a moment of financial identity — a moment where someone decides which institution they trust most with their money and their habits.

When PayPal captures that moment, consistently, month after month, the community bank quietly gets demoted. The mortgage stays. The savings account stays. But the daily financial relationship — the one that creates real stickiness, that generates cross-sell opportunities, that makes a customer hard to lose — migrates somewhere else.

Researchers call this “soft-switching.” The customer never closes their community bank account. They just stop using it as a primary transaction account. J.D. Power data confirms this pattern is accelerating.

community bank deposit retention strategies

What PayPal Has Actually Built

It’s worth being specific about the product set here, because vague awareness of “PayPal” doesn’t lead to action.

PayPal and Venmo together now offer:

- P2P transfers with 81% of all U.S. digital wallet P2P transaction volume running through Venmo alone

- A debit Mastercard with merchant-specific cash back rewards and spending accepted anywhere Mastercard is accepted

- FDIC pass-through insurance on stored balances (through program banks), which removes the main consumer safety objection

- Direct deposit capability, letting Venmo become the account where a paycheck lands

- High-yield savings through PayPal, designed explicitly to compete for primary account status

- Buy Now, Pay Later through PayPal Pay Later, embedded in the same ecosystem

- Commerce integrations with dozens of major consumer platforms

PayPal processed $1.79 trillion in total transaction volume in 2025. Venmo’s share of that is growing. The company has told investors it expects Venmo revenue to hit $2 billion by 2027, driven specifically by the debit card and merchant payment growth.

This is not fintech experimentation. This is a scaled, profitable, growing financial platform competing for your customers’ primary account relationship — without a banking license, without your regulatory burden, and with a user experience most community banks cannot match.

The Soft-Switch Is Already Happening in Your Market

The insidious thing about soft-switching is that it doesn’t show up in account closure data. Your customer retention numbers still look fine. Net promoter scores are solid. What’s invisible in your dashboard is that three years ago, your checking account customer used their debit card 37 times a month, and today they use it 14 times. The rest of those transactions went somewhere else — Venmo, Cash App, Apple Pay — and each one is a missed cross-sell, a missed moment of trust-building, a missed data point.

Community banks that track average transactions per active debit card will sometimes see this pattern. Most don’t track it.

The industry framing of this threat has been too abstract: “fintechs are disrupting banking.” That framing lets community bank executives keep it at arm’s length. The concrete reality is more uncomfortable: a specific person in your market, who you know by name, who has banked with you for 15 years, is using Venmo every day and their community bank once a month.

community bank customer engagement metrics

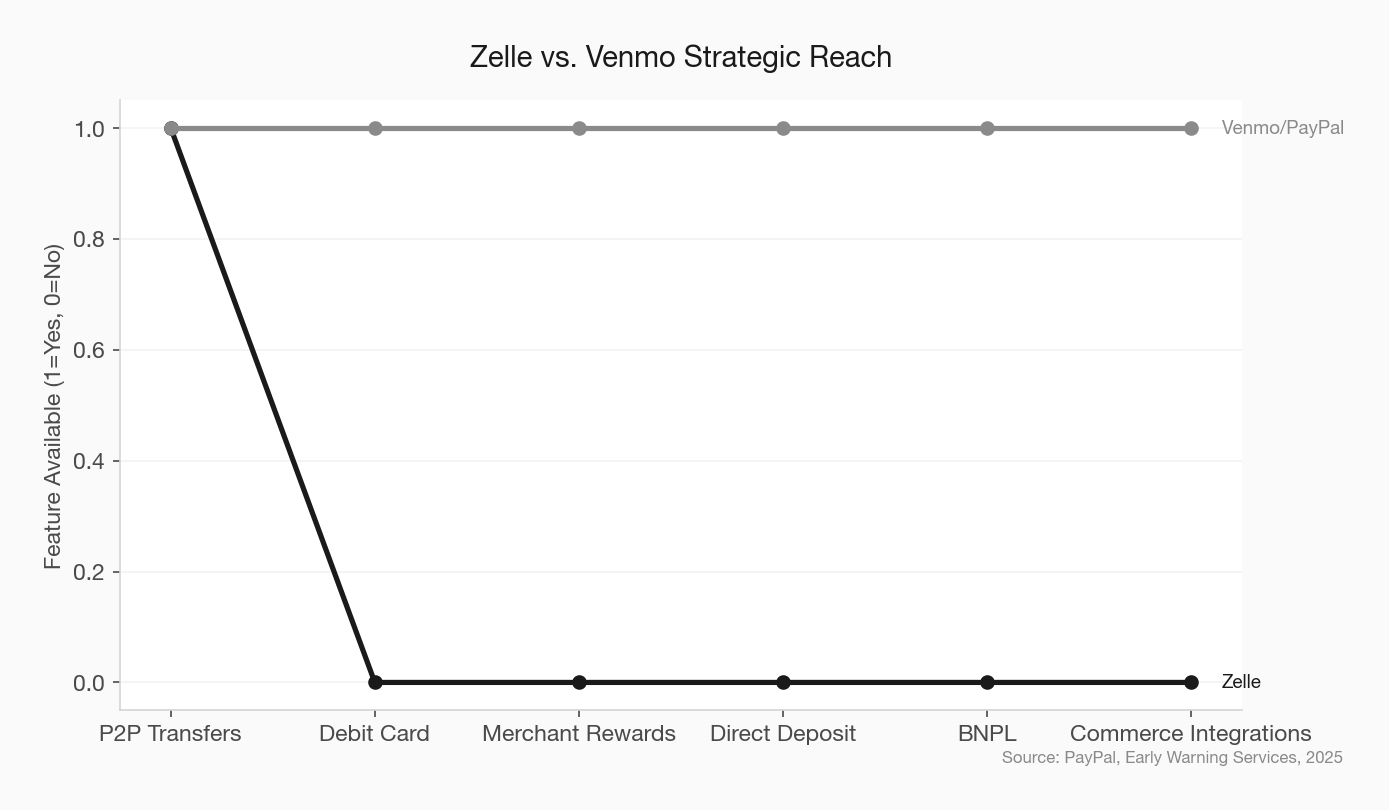

The Zelle Answer Is Necessary but Not Sufficient

The most common community bank response to payment app competition is Zelle. Fair enough — Zelle is the right move. In 2025, 337 banks and credit unions (97% with assets under $10 billion) went live or signed on with Zelle. American consumers and small businesses sent more than $1.2 trillion through Zelle last year. Offering Zelle keeps your customers from leaving for P2P alone.

But Zelle doesn’t solve the problem. It solves one symptom: P2P transfers. Venmo has expanded far beyond P2P. Venmo is now a debit card, a rewards program, a merchant payment method, a direct deposit destination, and a commerce platform. Zelle is a money-movement utility embedded inside your mobile banking app.

The community banks that stop at Zelle and call it a payments strategy are still losing ground on the relationship layer.

Zelle community bank adoption strategy

What Community Banks Should Actually Do

There are three moves worth making. None of them require a technology team.

First, audit the transaction frequency data on your checking accounts. Segment by age and look at debit transaction counts over the last 24 months. If you see a steady decline in transactions-per-account among under-40 customers, you are already in the soft-switch pattern. Knowing is the precondition for acting.

Second, build a debit rewards program that gives people a reason to use your card over Venmo’s. This doesn’t have to be expensive. It has to be visible, local, and personally relevant. The community bank that partners with 20 local businesses to offer 3% cash back at Main Street merchants has something Venmo can never match: local specificity. That’s differentiation that doesn’t require matching a tech company’s budget.

Third, reclaim the small business payments relationship before someone else does. Business owners are the most financially engaged customers a community bank has. PayPal and Venmo are already embedded in small business cash flow through point-of-sale, invoicing, and customer payments. A community bank that offers a business owner integrated payment acceptance, business debit with rewards, and same-day Zelle transfers — bundled, simple, and human — can compete on the relationship dimension that PayPal can’t touch.

community bank small business banking program

The Relationship Advantage Is Real But It’s Not Automatic

Community banks have one thing PayPal will never have: a person behind the relationship. When a small business owner calls Venmo because of a transaction dispute, they get a bot. When they call their community bank, they get someone who knows their name and their business.

That advantage is real. But it only matters if the community bank is actually present in the customer’s payment life. An advantage you’re not deploying is not an advantage — it’s a hypothetical.

PayPal’s strategy is explicit and documented in investor materials: become the primary financial platform for their users. They are executing that strategy, quarter by quarter, feature by feature, merchant by merchant.

The community bank that treats payments as a utility function — something you plug into through your core provider and don’t think about again — is conceding the front door to a competitor that has thought about nothing else for the last decade.

Payments are not a commodity. They are the daily touchpoint from which every other financial relationship grows. Community banks that understand this will still be competing in 2030. The ones that don’t will still have deposits — just fewer of them, and from customers who are aging out.

community bank marketing strategy 2026