Predictive Analytics for Loan Officers: Practical, Not Theoretical

Community bank loan officers sit on rich data they never use. Predictive analytics tools now flag churn, spot cross-sell, and prioritize outreach — no data science team needed.

The average community bank loan officer manages 150 to 300 relationships. They know who’s reliable, who’s a flight risk, and who might need a new line of credit — but they know it from gut feel, not data. That instinct is valuable. It’s also not scalable, not transferable when someone retires, and not reliable when markets shift faster than memory can track.

Here’s the reality: your loan officers are sitting on a goldmine of customer data — transaction histories, cash flow patterns, payment behaviors, account balances, product holdings — and almost none of it is being analyzed in any structured way. The tools that turn that data into actionable intelligence are no longer reserved for JPMorgan’s quant team. They’re accessible, affordable, and built for institutions your size.

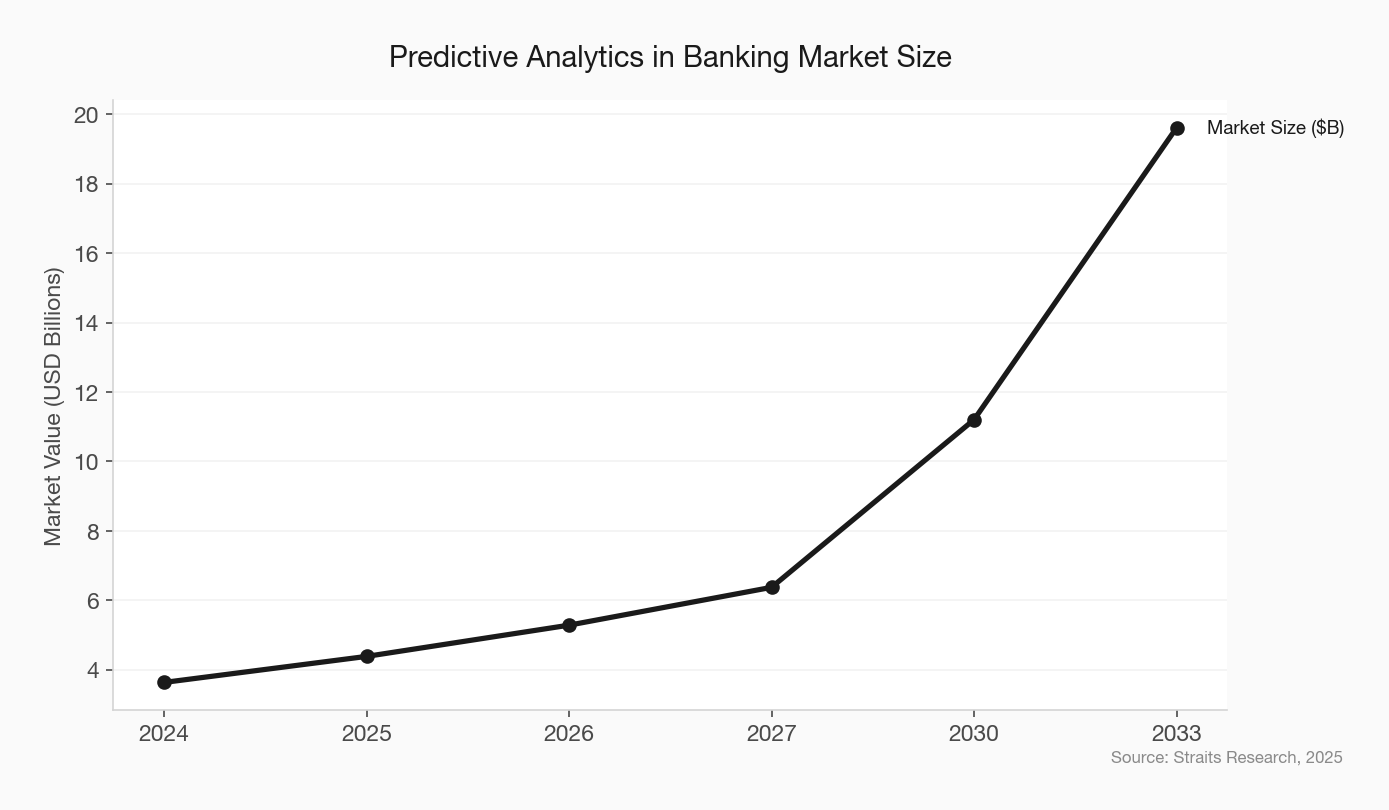

The predictive analytics market in banking hit $4.38 billion in 2025 and is projected to reach $19.61 billion by 2033. That growth isn’t being driven by megabanks alone. It’s being driven by community banks and credit unions that realized they don’t need a data science team — they need the right platform.

What Predictive Analytics Actually Means for a Loan Officer

Strip away the buzzwords and predictive analytics does three things for a community bank loan officer:

It tells you who’s about to leave. Churn prediction models analyze transaction patterns, balance trends, and engagement signals to flag customers at risk of moving their business. Banks and credit unions lose nearly 15% of customers annually. A 2025 BlastPoint study found that one financial institution reduced deposit attrition by 7% in a single quarter simply by targeting proactive retention campaigns to high-risk households. Your loan officer doesn’t need to build the model. They need the alert.

It tells you who’s ready to buy. Cross-sell models identify customers whose behavior patterns suggest they’re approaching a financial milestone — a recurring salary increase, a growing savings balance, increased credit utilization. These are signals that a customer may be ready for a mortgage, a business expansion loan, or a new deposit product. Traditionally, loan officers don’t have time to hunt for these signals. Predictive platforms serve them up automatically.

It tells you where to spend your time. Lead scoring and prioritization models rank your portfolio by likelihood of conversion, risk of default, or urgency of outreach. Instead of working through a call list alphabetically, your loan officer starts with the 15 relationships that matter most today.

None of this requires a PhD. It requires a platform that connects to your core and surfaces insights where your people already work.

The Tools That Actually Work for Community Banks

The vendor landscape has matured significantly. A few platforms stand out for community bank-sized institutions:

Alkami has built its predictive AI specifically for community banks and credit unions. Their platform analyzes spending and behavior patterns to anticipate account holder needs and surface next-best-action recommendations. For loan officers, this means seeing which customers demonstrate behaviors most likely to lead to loan adoption — and getting tailored messaging prompts to engage them. Alkami’s approach keeps human oversight central, which matters for relationship-driven institutions.

Abrigo offers a unified platform connecting lending, risk, and analytics workflows. Their configurable loan officer dashboards surface pipeline data, deal summaries, and risk signals in one view. For community banks already using Abrigo for lending or BSA/AML, the analytics layer plugs directly into existing workflows — no separate login, no parallel system.

Zest AI focuses specifically on credit decisioning. Their platform uses over 650 proprietary credit models to increase approval rates by 25% while reducing defaults by 20%. First Hawaiian Bank won Celent’s 2025 Model Bank Award for AI-Augmented Retail Lending after implementing Zest AI’s automated underwriting. SchoolsFirst Federal Credit Union more than doubled its instant approval rate using the same technology. These aren’t theoretical projections — they’re audited results.

Baker Hill provides loan origination software with built-in analytics for commercial and consumer lending. Their platform is designed for the community bank workflow: structured enough for compliance, flexible enough for relationship banking.

The common thread: none of these require your bank to hire a data scientist. They require a decision to connect your data and trust the output enough to act on it.

The Cross-Sell Opportunity Your Loan Officers Are Missing

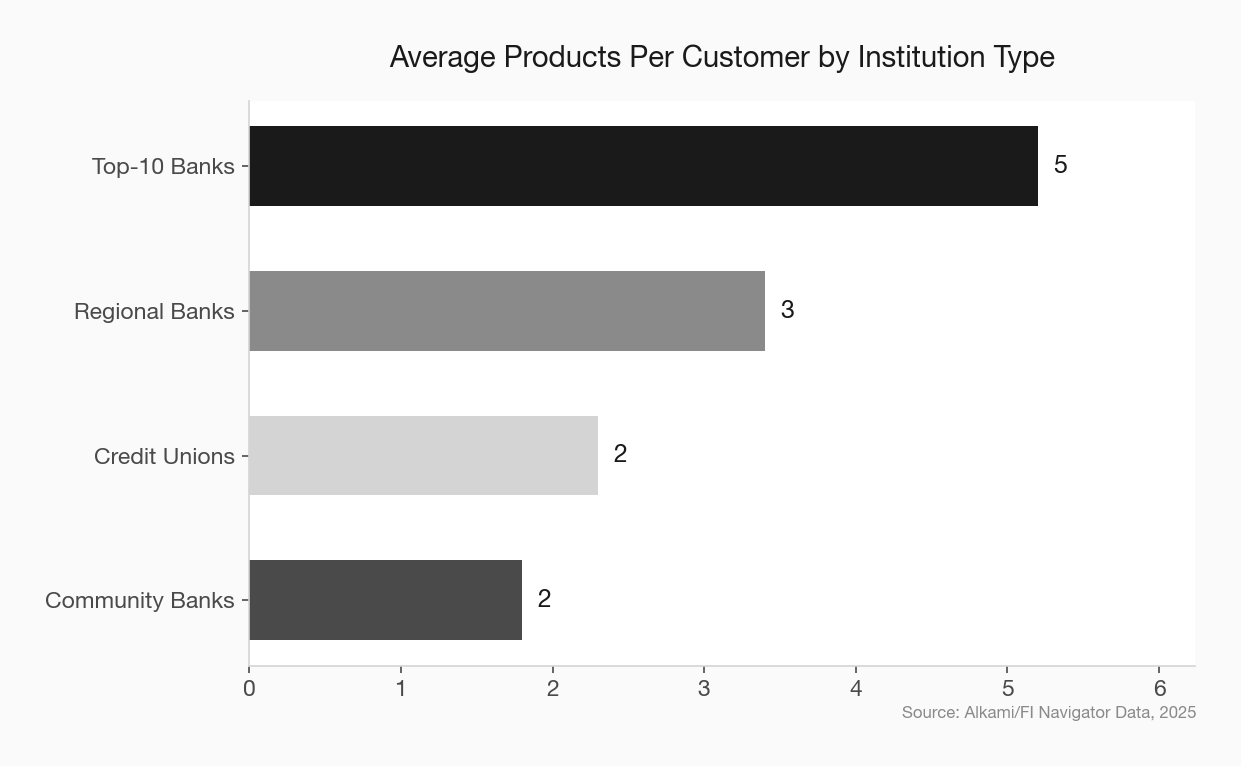

Here’s a number that should bother every community bank CEO: the average community bank customer holds 1.5 to 2 products. The average customer at a top-10 bank holds 4 to 6. That gap isn’t about product availability — community banks offer most of the same products. It’s about visibility and timing.

Your loan officer processes a commercial real estate loan. During underwriting, they see the borrower’s operating accounts, cash flow cycles, and payroll patterns. Embedded in that data are signals: this business could benefit from treasury management services. The owner’s personal accounts show a pattern consistent with someone about to need a home equity line. The business has seasonal cash flow gaps that a revolving credit facility would solve.

Traditionally, as one industry source put it, “your average loan officer is not going to go looking for that type of data. They don’t have time. We’re just serving it up to them.”

That’s the shift. Predictive cross-sell isn’t asking loan officers to become analysts. It’s giving them a prompt at the right moment: “This customer has a 72% likelihood of needing X in the next 90 days. Here’s the data supporting it.”

The revenue impact is direct. Moving from 1.8 to 2.5 products per customer doesn’t require new customers. It requires knowing which existing customers are ready and reaching them before a fintech does.

community bank deposit growth strategy

Churn Prediction: The Defensive Play That Pays for Itself

More than half of community bank executives — 54% — named deposit growth as their biggest challenge in 2025. And Deloitte found that 20-28% of Gen Z and millennial customers say they’re likely to switch their primary bank within two years due to poor personalization and lack of perceived value.

Churn prediction models flip the defensive game from reactive to proactive. Instead of discovering a customer left when you notice the zero balance, you get a signal weeks or months before the departure: declining transaction frequency, balance drawdowns, reduced direct deposit amounts, increased ACH transfers to competitors.

The Qualtrics Banking Report found that 56% of customers who left their bank said the bank could have changed their mind. That’s a staggering admission. More than half of your defections are preventable — if you see them coming.

Here’s what this looks like in practice: a predictive model flags 40 high-risk commercial relationships in your portfolio. Your loan officer or relationship manager gets a prioritized list with the underlying signals. They make 10 calls this week — not cold calls, but informed conversations. “I noticed your business has been growing. Are we keeping up with what you need?” That’s not AI replacing the relationship. That’s AI making the relationship work.

A $2.5 billion community bank that implemented predictive modeling for its commercial loan portfolio was able to identify a segment of borrowers whose true default risk was 35% higher than traditional credit scores suggested. The early warning enabled proactive loan restructuring and reduced loan loss provisions by approximately $1.2 million in year one.

community bank customer retention strategies

The Data You Already Have Is Enough

The most common objection I hear from community bankers: “We don’t have enough data.” Wrong. You have too much data. You’re just not using it.

The typical community bank core system contains years of transaction data, account history, payment behavior, and product usage for every customer. That’s the raw material. Modern predictive platforms don’t need exotic data sources — they need the transaction, balance, and behavioral data you’ve been collecting since you installed your core.

What they do need is clean connections. And this is where the real barrier lives. It’s not the analytics — it’s the core integration. Legacy core systems either don’t expose APIs or charge prohibitive fees for data access. If your core vendor treats your own data as a revenue center, that’s a strategic problem that goes beyond analytics.

For banks on modern or modernizing cores, the path is straightforward: connect the data feed, configure the models, and train your loan officers on the output. Most implementations take 60 to 90 days from contract to live dashboards.

For banks stuck on legacy cores, middleware solutions from vendors like Alkami and Baker Hill can bridge the gap — pulling data from the core via batch processes and normalizing it for the analytics layer. It’s not ideal. But it works, and it’s better than waiting for a core conversion that may be years away.

core banking system cost and API strategy

What 66% of Credit Unions Already Know

Here’s a data point that should motivate any competitive community banker: 66% of credit unions now plan to leverage AI for credit decisioning. Credit unions — institutions that community bankers sometimes dismiss as less sophisticated — are moving faster on predictive analytics adoption.

Why? Because credit unions figured out that predictive tools amplify the relationship advantage they already have. The same logic applies to community banks, arguably more so. Your loan officers know the market. Predictive analytics helps them know it faster and act on it sooner.

The institutions seeing the best results share three traits:

First, they started with one use case, not five. The banks that try to boil the ocean — churn prediction plus cross-sell plus credit scoring plus fraud detection — stall in implementation. The ones that pick a single pain point (usually churn or loan officer lead prioritization) and prove it out in 90 days build the internal credibility to expand.

Second, they made it a loan officer tool, not a management reporting tool. If the analytics output lives in a dashboard that only the CFO sees, nothing changes on the front line. The banks getting ROI put the insights directly in the loan officer’s workflow — in their CRM, in their daily task list, in their morning huddle.

Third, they didn’t ask for perfection. A model that’s right 70% of the time is infinitely more useful than a gut instinct that’s never measured. Loan officers who initially resist the technology come around fast when the model’s flagged customers actually do churn — or actually do convert on a cross-sell recommendation they would have missed.

AI tools community banks should use

The Implementation Playbook

For the community bank executive reading this and thinking “fine, what do I actually do,” here’s the sequence:

Month 1: Audit your data. What does your core expose? What’s the quality of your transaction data? Do you have a customer master that links accounts to households? If you can’t answer these questions, that’s your first task. Most cores have this data; most banks have never inventoried it.

Month 2: Pick one use case and one vendor. If deposit retention is your biggest pain, start with churn prediction. If loan growth is the priority, start with cross-sell scoring. Talk to Alkami, Abrigo, or a similar platform purpose-built for your tier. Get a demo with your own data — not a generic pitch deck.

Month 3: Pilot with five loan officers. Don’t roll it bank-wide. Pick your five most engaged (not necessarily most senior) loan officers. Give them the tool, give them a target (10 outreach actions per week based on model recommendations), and measure the results. Conversion rates, retained balances, new products opened.

Month 4-6: Measure, adjust, expand. If the pilot works — and the data consistently shows it does — expand to the full team. If it doesn’t, you’ve spent a quarter and a modest implementation fee to learn something valuable about your data infrastructure.

The cost for most community bank-tier predictive platforms runs between $3,000 and $15,000 per month depending on asset size and modules. Compare that to the cost of one lost commercial relationship or one loan officer spending 30% of their time on low-probability prospects.

The Real Barrier Isn’t Technology

Let’s be direct about what actually stops community banks from adopting predictive analytics: it’s not cost, it’s not data, and it’s not complexity. It’s culture.

Loan officers who’ve built careers on personal relationships can perceive data-driven recommendations as a threat to their autonomy. Management teams that have always relied on quarterly reviews and intuition can see real-time analytics as an uncomfortable accountability mechanism.

The banks that overcome this don’t frame predictive analytics as a replacement for judgment. They frame it as ammunition for the people who already know the market. Your best loan officer’s instinct, backed by data, is an unstoppable combination. Your newest loan officer’s learning curve, shortened by data, is a hiring advantage.

Community banks spend enormous energy worrying about fintechs. Here’s what fintechs have that you don’t: algorithms that know which customer to talk to and when. Here’s what you have that fintechs don’t: a human being who can walk into a business, sit across the desk, and make a judgment call.

Combine those two things. That’s the play.

hiring for digital skills at community banks