SoFi vs. Your Community Bank: An Honest Feature Comparison

SoFi wins on rates and digital polish. Community banks win on lending, trust, and local know-how. Here's the honest breakdown — and the talking points community bankers need.

SoFi just crossed 13.7 million members, was named Best Online Bank of 2026 by NerdWallet, and has posted eight consecutive quarters of GAAP profitability. It is no longer a scrappy challenger — it is a fully chartered bank with a national footprint, a compelling product suite, and a brand that resonates with the under-40 crowd.

Community bankers need to stop dismissing SoFi and start understanding it. Not to copy it. To compete with it.

This is a real, honest, feature-by-feature comparison. Where SoFi wins, where community banks win, and where the gap is a lot smaller than fintech boosters want you to think.

Where SoFi Has the Advantage

Let’s be direct. There are areas where SoFi genuinely outperforms the average community bank, and pretending otherwise serves no one.

High-Yield Savings Rates

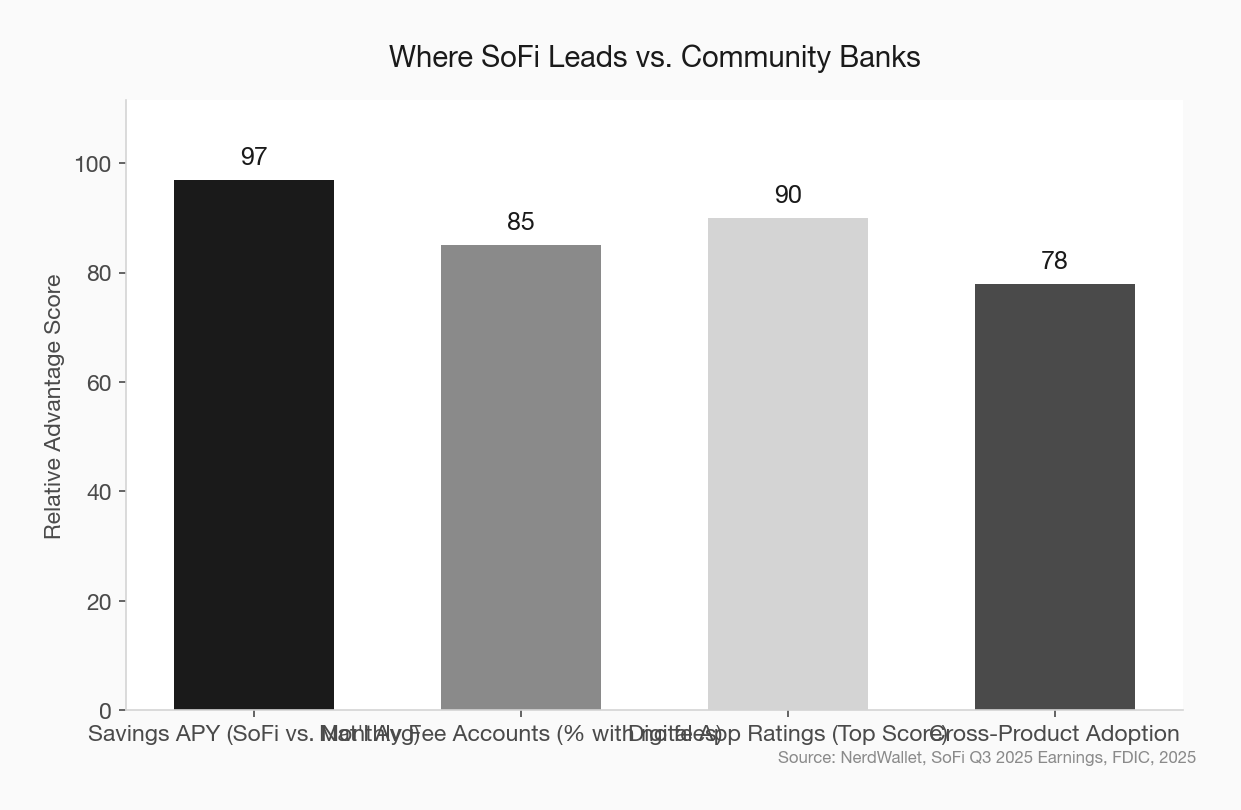

SoFi’s savings account currently earns 3.30% APY with direct deposit, with a promotional rate up to 4.00% APY for new SoFi Plus members. The national average savings rate sits at around 0.07%.

Most community banks don’t come close. If a depositor is rate-shopping and their only benchmark is APY, SoFi wins.

The honest response for community bankers isn’t to rate-match — it’s to compete on the total relationship value. A higher yield on savings at SoFi doesn’t offset the cost of driving to a branch that doesn’t exist, or calling a 1-800 number when your business account has a problem at 4:45 on a Friday.

No Fees

SoFi charges no monthly fees, no overdraft fees, no minimum balance requirements. It’s a zero-friction product for checking and savings.

Many community banks still charge monthly maintenance fees or require minimum balances to waive them. If you’re one of them, that’s a competitive liability that’s easy to fix — and worth fixing now.

Product Breadth and Integration

SoFi bundles checking, savings, investing, personal loans, student loan refinancing, mortgages, and credit cards under one roof — and cross-sells aggressively. In Q1 2025, 32% of new products were opened by existing members.

That’s not just a technology advantage. It’s a relationship deepening strategy. Community banks talk about relationship banking as a competitive edge, but SoFi is executing on cross-product stickiness at scale.

Digital Experience

SoFi offers early paycheck access (up to two days), 55,000+ ATM locations, automatic savings roundups, goal-based Vaults, and a mobile app that consistently earns top ratings.

The average community bank mobile app in 2026 is functional. Some are genuinely good. But if a prospect opens both apps side by side, SoFi’s UX will look more polished in most cases.

Where Community Banks Have the Advantage

Here is where community bankers need to sharpen their talking points — because the advantages are real, they’re material, and most banks aren’t communicating them well.

Small Business Lending

Community banks are responsible for nearly 60% of all small business loans under $1 million and 80% of all agricultural loans. SoFi does not offer traditional business banking. It has no SBA loan program, no relationship-based commercial underwriting, and no ability to sit across the table from a business owner and structure a deal around the complexity of their situation.

This is not a small gap. For any business owner who needs financing — and most do — SoFi is not a real option. Community banks need to say this plainly.

community bank small business lending advantage

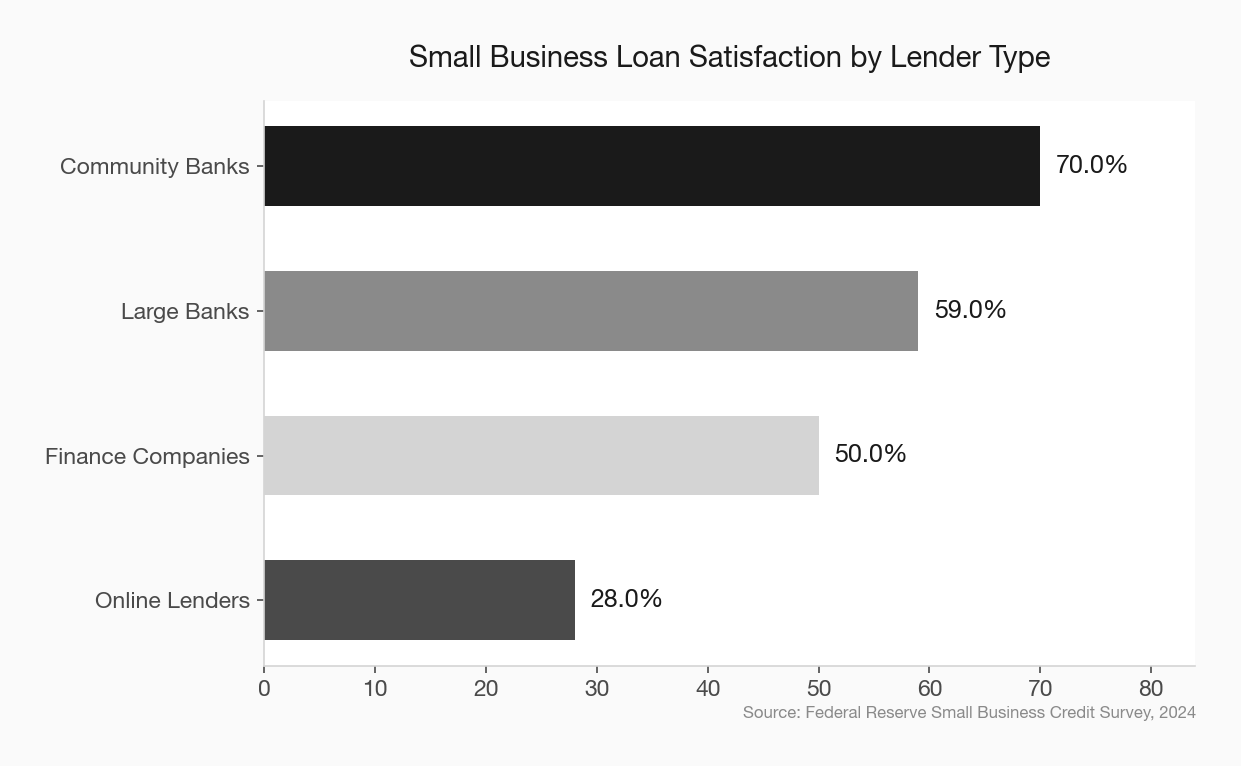

Loan Approval Rates and Satisfaction

According to Fed Small Business surveys, 70% of community bank loan applicants reported being satisfied with their experience, compared to just 28% for online lenders. Community banks approved 75% of small business loan applications compared to 66% at large banks.

The approval rate gap reflects something structural: community bank loan officers know the borrower, the business, and the market. They can weigh factors that don’t show up in a credit algorithm — the owner’s history, the local economy, the viability of the plan.

SoFi’s lending is consumer-focused and algorithm-driven. That’s fine for a personal loan. It is insufficient for a $400,000 equipment loan to a manufacturer in a small town.

Physical Presence and Cash Handling

SoFi has no branches. For many consumers this is irrelevant. For others — small business owners who handle cash, older depositors, customers who value face-to-face problem resolution — it is a dealbreaker.

SoFi also makes it difficult and sometimes costly to deposit cash. That’s a real operational friction for a significant slice of the population.

Trust, Longevity, and Community Roots

A community bank that has operated in the same market for 50 or 100 years carries a form of credibility that cannot be manufactured. SoFi was founded in 2011. It has been profitable for eight quarters. That is a real achievement. It is also not the same as being the bank that financed the first building downtown.

Local trust is not nostalgia — it’s a business asset. community bank brand trust local market

Where the Gap Is Smaller Than You Think

This is the section most fintech boosters skip, and most community bankers miss too.

Mobile Banking Is No Longer a Differentiator

In 2018, having a good mobile app was a competitive edge for digital banks. In 2026, it is table stakes. The majority of community banks now offer mobile check deposit, Zelle, account alerts, and card controls. The quality varies, but the baseline functionality is there.

If your mobile app works, you’re not losing deals because you’re a community bank. You might be losing deals because of your rates, your fees, or how you’re telling your story.

SoFi Doesn’t Do CDs or Money Market Accounts

This surprises a lot of people: SoFi offers no certificates of deposit and no money market accounts. For depositors seeking guaranteed yields over a fixed term — a significant and growing segment of the wealth market — SoFi has a product gap.

Community banks that offer competitive CD rates have a real argument with this customer type. Use it. community bank CD rates competitive advantage

SoFi Still Can’t Replace the Relationship

SoFi’s cross-sell rate is impressive. But the relationship it creates is a product relationship, not a human one. When a business owner calls their community bank, they often talk to the same person who approved their first loan. When a SoFi member has a complex problem, they call a contact center.

That distinction matters to a specific customer — and it’s the customer most likely to be profitable over a 10- to 20-year horizon.

The Honest Takeaway for Community Bankers

SoFi is a real bank now. It will keep growing. It will get better.

But SoFi is built for a specific customer: digitally native, consumer-focused, interested in managing everything from one app, and not particularly tied to a local market. That customer exists, and community banks should stop fighting for them.

The community bank customer is a small business owner who needs a line of credit and wants to call someone when there’s a problem. It’s a family that has banked locally for two generations. It’s a farmer who needs an agricultural loan that no algorithm will touch.

Win the fights you can win. Fix your fees. Get your mobile app to functional. Stop rate-matching on savings when you can’t sustain it. And then compete hard on lending, service, and community.

SoFi can’t lend to your butcher. You can.

community bank competitive strategy against fintech deposit competition community banks