Super Apps Are Coming to the US. Here's the Community Bank Response Playbook.

WeChat's financial dominance is the blueprint every US tech giant is studying. Community banks have a narrow window to build a counter-offer. Here's what that looks like.

In March 2026, Elon Musk’s X launched a public beta of X Money — a 6% APY deposit account, a metal Visa debit card, and peer-to-peer payments, all embedded inside a social platform used by hundreds of millions of people. He built it by studying WeChat. Apple already has $16.5 billion in deposits and the payment rails loaded into your customers’ pockets. Amazon is making lending decisions in your market using transaction data no community bank has access to.

This is not a future threat. It’s a present one. And the community banks that treat it as a future problem will wake up in three years and find they’ve ceded ground they can’t get back.

The WeChat Playbook, Translated

WeChat started as a messaging app in China in 2011. Today, 1.3 billion people use it monthly — not just to message, but to pay for groceries, hail rides, apply for loans, transfer money, and invest in wealth products. Financial services aren’t an add-on. They’re infrastructure. The reason people can’t leave WeChat is the same reason they can’t leave a bank: too much of their financial life runs through it.

That’s the model every major US tech platform is studying. Build a daily-use app. Establish the habit. Then layer financial services on top until you become the user’s primary financial relationship — without ever applying for a banking charter.

American tech companies have been chasing this for years. Now they’re executing.

What’s Already in Market

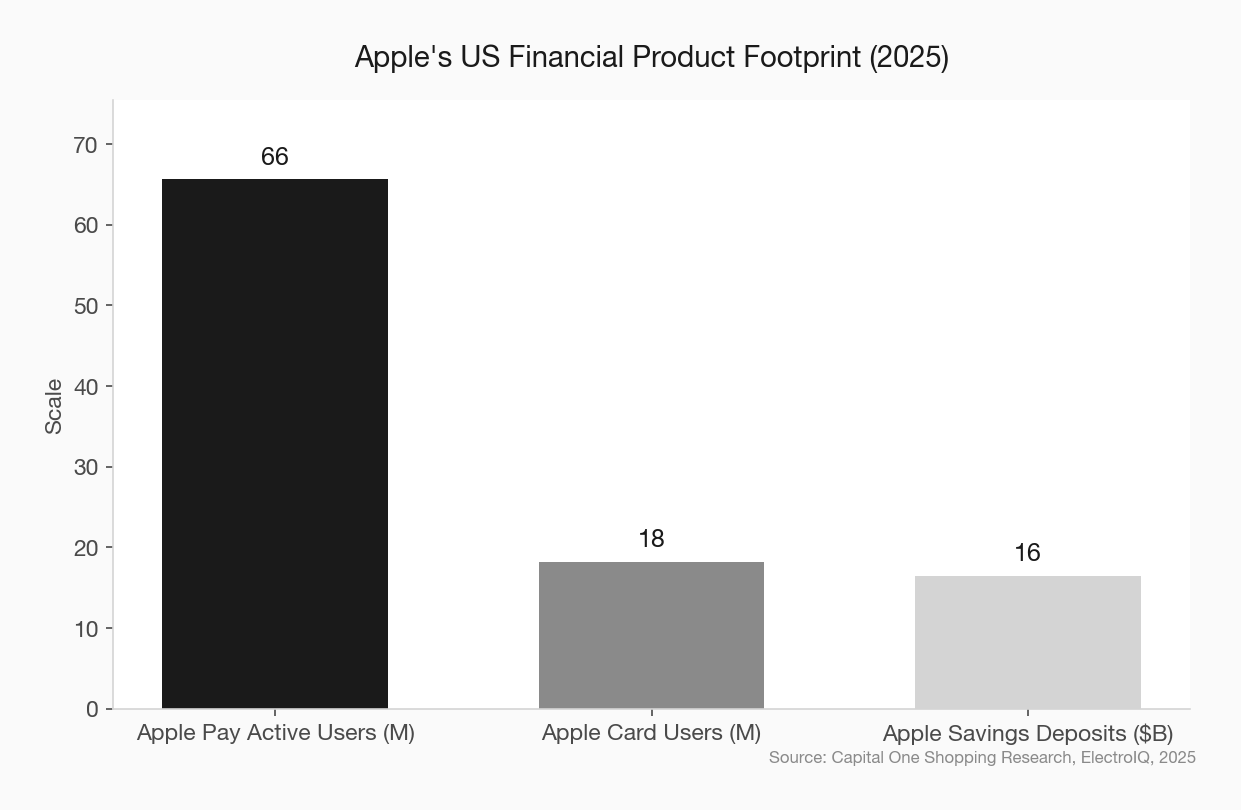

Apple has built a financial ecosystem quietly and methodically. Apple Savings surpassed $16.5 billion in deposits in 2025, offering a 4.15% APY through Goldman Sachs — competitive with any high-yield savings product available anywhere. Apple Pay commands 65.6 million active US users and a 54% share of in-store mobile wallet transactions. Apple Card reached 18.2 million users by end of 2025, up 21% year over year.

Apple doesn’t need a banking license to capture your depositors. It already is.

X Money launched its public beta in March 2026 with 6% APY FDIC-insured deposits (through Cross River Bank), a metal Visa debit card, zero foreign transaction fees, 3% cashback, and P2P payments powered by Visa Direct. By early 2026, X had secured money transmitter licenses in 40 states and DC. Elon Musk has explicitly cited WeChat as his model and described his ambition to make X a $250 billion payments company.

Amazon, through Amazon Capital Services, already disburses loans to marketplace sellers based on their transaction performance data — no application, no branch, no relationship banker required. The data advantage Amazon has over community banks in small business lending is structural and growing.

Google is embedding itself in banking infrastructure through Google Cloud. Major institutions — KeyBank, Wells Fargo — are migrating core systems to Google’s environment. That’s a strategic foothold that has nothing to do with a consumer savings account and everything to do with who controls the architecture of banking.

Why the US Version Will Be Different — and Still Dangerous

The true WeChat super app probably won’t replicate itself in the US. The regulatory environment is more fragmented. Data privacy expectations are higher. American consumers are accustomed to using separate apps for separate purposes, and antitrust scrutiny adds friction to the “everything app” model.

Community bankers sometimes hear this and exhale.

They shouldn’t. What’s emerging in the US isn’t a single everything-app — it’s category-dominant super apps. One for finance, one for social, one for commerce. Apple doesn’t need to offer ride-hailing to become the default financial layer in your customers’ lives. It just needs to be where they save, spend, and borrow.

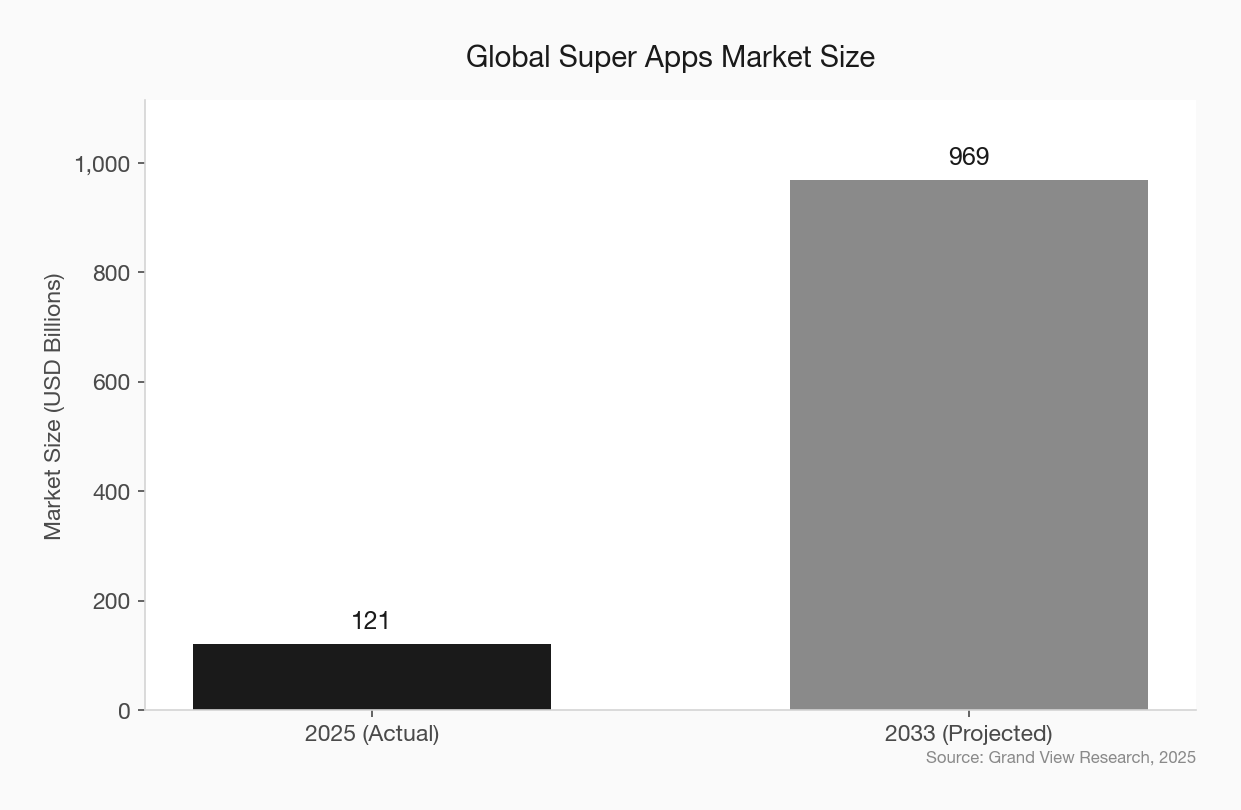

The global super apps market was valued at $121 billion in 2025 and is projected to reach $968 billion by 2033 — a 30% compound annual growth rate. That trajectory includes the US market. The question isn’t whether a super app captures meaningful share of your customer relationships. It’s when, and which platform gets there first.

In a survey of more than 500 community bank executives, roughly one in four named big tech companies as the number-one threat to their business models. More than twice as many as those who named the largest banks as their primary competitor. Community bankers already know what’s coming. The question is whether they’re building a response.

The Core Strategic Problem: The Habit Loop

WeChat didn’t win China by having better features than banks. It won because it became a daily habit. People opened WeChat dozens of times a day — to message, to pay, to order food. Financial services were a natural extension of behavior that was already automatic.

Most community bank customers open their bank’s mobile app once or twice a month. That’s not a relationship. That’s a utility bill.

Tech companies have the habit loop. Community banks have the relationship. The strategic task is to convert the relationship into a habit before tech companies convert their habit into a financial relationship. That window is open now. It won’t stay open indefinitely.

The Community Bank Response Playbook

1. Become the Primary Payment Rail in Your Market

Payments are the highest-frequency banking touchpoint. If your customers pay rent, split dinner, and pay local businesses through a tech platform’s wallet, that platform becomes their de facto primary bank — regardless of where the deposit account sits.

Community banks that want to stay relevant in the super app era need a payments strategy. That means full support for real-time payments via RTP and FedNow. It means making sure your debit card is the default loaded in Apple Pay and Google Pay. It means evaluating white-label P2P tools that carry your brand, not a fintech’s.

The goal isn’t to build your own Venmo. It’s to make sure your card is the one your customers reach for when they pay — and that every payment reinforces your brand, not someone else’s.

FedNow adoption community banks real-time payments strategy

2. Use Relationship Data to Build Financial Routines

Super apps win through habit engineering. Community banks have the data to do the same — they just rarely use it.

A customer with direct deposit, a checking account, and an auto loan at your institution is not going to disappear overnight. But if you never surface their financial picture back to them in a useful way, a competing app will. Proactive balance alerts, spending summaries, loan payoff projections, savings rate comparisons — these are all within reach for community banks with modern digital banking platforms. More importantly, they’re the kind of personalized guidance that Apple Savings can’t offer, because Apple doesn’t know what your customer told your loan officer three years ago.

That context is your advantage. Build features around it.

community bank data analytics personalization mobile banking

3. Go Vertical Before Big Tech Gets There First

The US super app landscape is evolving toward vertical dominance rather than horizontal everything-apps. The community bank equivalent is vertical banking: owning a specific customer segment so completely that a super app has no economic incentive to compete for it.

What does this look like in practice? A community bank in an agricultural market that builds a lending program, equipment financing, a grain storage payment tool, and a crop insurance resource into a single experience has built something no tech giant will replicate for a $500 million bank in a rural county. The market isn’t big enough for Apple to bother. But it’s exactly big enough for your bank.

The same logic applies to small business banking. Mercury and Relay have clean interfaces and fast onboarding. They cannot, however, look a business owner in the eye and make a judgment call on a character loan. Community banks that build their business banking program around that irreplaceable advantage — fast local decisions, one banker who answers the phone, deep knowledge of the local economy — have a position that survives the super app era.

vertical banking strategy community bank small business niche

4. Embed Yourself in Local Workflows

Here’s the counterintuitive play: get inside the ecosystems that are threatening you.

Several community banks are already partnering with local software platforms — property management tools, point-of-sale systems, contractor billing apps, payroll providers — to surface banking services inside the workflow. A restaurant owner who gets a small business line of credit through their POS system without visiting a branch is still banking with you. They just found you in a different place.

This is how community banks compete with embedded finance: by becoming an embedded option themselves. A 2025 survey by Treasury Prime found that 99% of community bank decision-makers said embedded finance is important to their institution’s long-term survival. The question isn’t whether to embed — it’s which workflow to embed into first.

Start with your existing relationships. If you serve local contractors, explore construction payment integrations. If you have strong healthcare practice relationships, look at patient financing. The super app wins by being where customers already are. Your version of that is being inside the software your local business customers already run every day.

embedded finance community bank partnership local business workflow

The Window Is Real — and Narrowing

Apple has $16.5 billion in deposits and the payment rails already sitting in your customers’ phones. X Money launched a 6% APY account this month. Amazon is making lending decisions in your market using data you’ll never have.

Community banks still have the relationship. The trust. The local knowledge. The context that no algorithm has replicated and no tech giant has bothered to acquire — because for now, it’s cheaper to take the transaction business and leave the complex stuff to you.

That calculus is changing. As super apps deepen their financial services layer, the complex stuff becomes less complex, and the relationship advantage narrows.

Community banks that act now — building a payments strategy, activating their relationship data, going vertical in their markets, and embedding in local workflows — will find the super app era opens more doors than it closes. The ones waiting for the threat to become undeniable will find that by then, the counter-offer is much harder to make.