The API Economy and What It Means for Your Core System Strategy

Community banks spend 40% of their core budget on integrations. The API economy is reshaping what to demand from your core vendor.

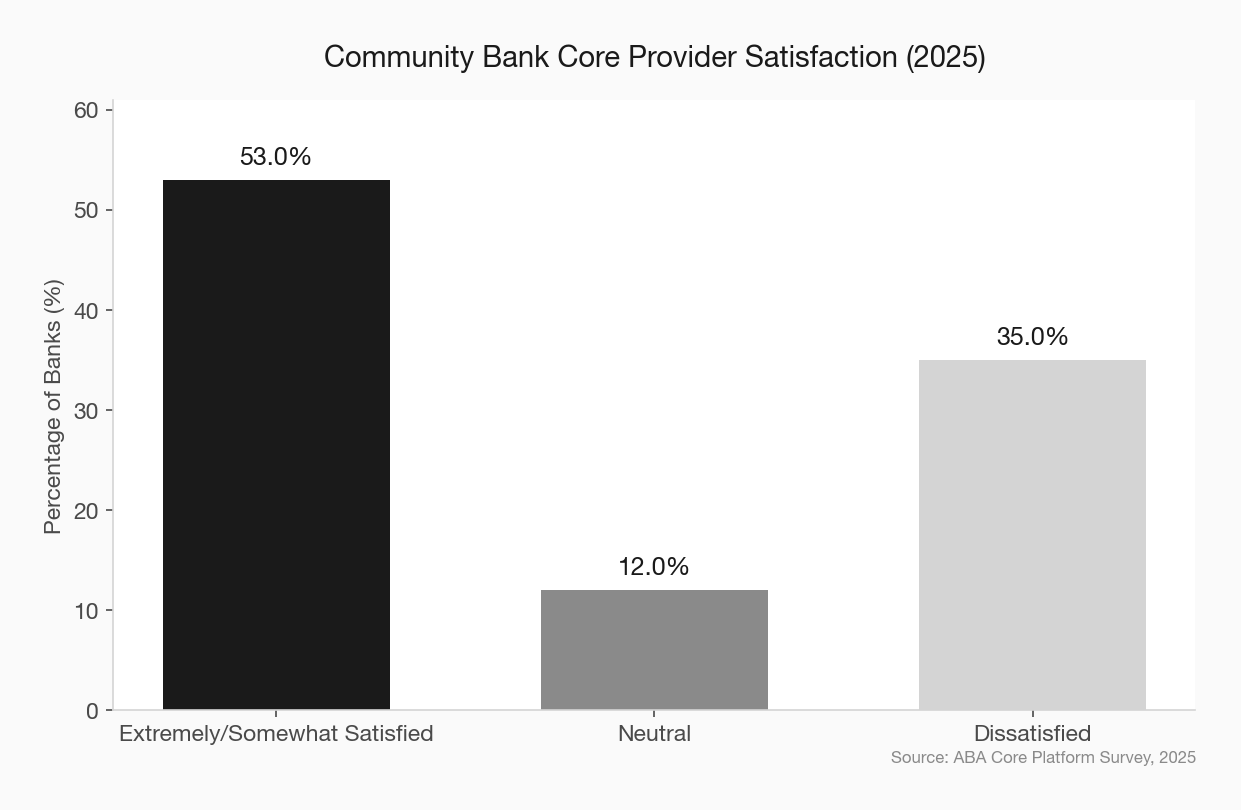

Thirty-five percent of community banks are dissatisfied with their core provider. That’s not a Glassdoor review — it’s the ABA’s 2025 Core Platform Survey. And when you dig into why, the same word keeps surfacing: integration.

The core banking system used to be the center of gravity for everything a community bank did. It handled deposits, loans, reporting, and compliance in a single monolithic package. That model worked when the core was the only software a bank needed. It does not work in 2026, when the average community bank relies on dozens of third-party tools for everything from digital account opening to fraud detection to CRM.

The connective tissue between those tools and your core is APIs. And if your core vendor treats API access as a premium add-on rather than a baseline feature, you’re paying a tax on every piece of innovation you try to adopt.

What the API Economy Actually Means for Banks

An API — application programming interface — is how two pieces of software talk to each other. When your digital banking platform pulls a customer’s balance from the core, that’s an API call. When your lending platform pushes a loan decision back to the core, same thing.

The “API economy” is what happens when those connections stop being one-off custom builds and start being standardized, published, and available to any authorized partner. It’s the difference between calling your core vendor every time you want to connect a new tool and plugging that tool in yourself through a documented interface.

For community banks, this matters for three reasons.

First, it determines how fast you can adopt new technology. A bank with open API access can integrate a new fintech partner in weeks. A bank waiting on its core vendor’s professional services team is looking at months — and a five-figure invoice.

Second, it determines how much you pay. Core providers have historically charged “click fees” for API usage, per-transaction costs for integrations, and premium pricing for access to more capable API tiers. A 2023 Forrester study found that financial institutions spend an average of 40% of their total core banking budget on customizations and integrations over a five-year period. That’s not product cost. That’s the cost of making the product work with everything else.

Third, it determines who controls your technology roadmap. If every new integration requires your core vendor’s involvement and approval, they have veto power over your innovation strategy. That’s not a partnership. That’s a dependency.

The Big Three Problem

The community banking core market is dominated by Fiserv, FIS, and Jack Henry. The Kansas City Fed has documented this concentration, and the OCC has taken notice. In May 2025, the OCC issued a Request for Information specifically about community bank digitalization — asking how banks manage connectivity using APIs, and whether there are limitations in their core providers’ API offerings around functionality, data accessibility, scalability, or third-party compatibility.

The response was loud enough that the OCC issued a second RFI in November 2025, this one focused exclusively on community banks’ engagement with core service providers. Among the 22 comments received on the first RFI, a recurring theme was “predominant market reliance on the largest core service providers, resulting in reduced bargaining power and difficulty integrating new technology with legacy platforms.”

Translation: community banks feel locked in, and the lock is getting tighter as the ecosystem of tools they need keeps growing.

To be fair, the Big Three are responding — slowly. Jack Henry is on track for an H1 2026 launch of its public cloud-native core, with 15 core components already live. FIS rolled out its Modern Banking Platform with an API-first architecture. Fiserv announced Core Advance as its next-generation platform. But cloud-native doesn’t automatically mean open, and “API-first” in a press release doesn’t always translate to “API-accessible” in a contract.

What “Good” Looks Like: The Questions to Ask Your Core Vendor

Not all API strategies are created equal. Here’s what separates a core with genuine API connectivity from one that just checks the box.

Is the API catalog published and documented?

A real API-first core publishes its full API catalog — every endpoint, every data object, every authentication method — in documentation that any developer can read. If you have to call your account rep to find out what’s available, that’s not open. That’s gated.

What does API access cost?

Ask for the full picture: per-call fees, monthly access fees, tiered pricing structures, and whether API access is bundled with your core contract or sold separately. Some vendors embed “click charges” that mean you’re paying both the fintech partner and the core provider every time data moves between them. Get this in writing before you sign.

Can third parties integrate directly, or do they have to go through the core vendor?

This is the critical question. Some cores require every integration to be built and certified through the vendor’s own professional services team. Others publish open APIs that allow any authorized fintech to connect directly. The difference is months of timeline and tens of thousands of dollars per integration.

What’s the data portability story?

APIs aren’t just about connecting tools. They’re about accessing your own data. Can you pull customer data, transaction history, and account information through APIs for your own analytics and reporting? Or is your data effectively held hostage inside the core?

The Real Cost of Your Core Banking System

The Middleware Option

If your current core isn’t API-friendly — and many legacy systems aren’t — middleware platforms offer a bridge. Kinective, which serves nearly 2,500 banks and credit unions, provides pre-built connectors between major cores and fintech applications. Portx focuses specifically on community banks and credit unions with a cloud-native integration layer.

Apiture’s digital banking platform now integrates with over 200 fintech partners across 40-plus cores, and in 2025 launched its Fintech Connector program to let new partners integrate without custom development work.

These middleware solutions aren’t free, and they add another vendor to manage. But for banks stuck on a legacy core with limited API access, middleware can unlock fintech partnerships that would otherwise be impossible — without the risk and cost of a full core conversion.

The strategic question is whether middleware is a long-term solution or a bridge to a more open core. For most community banks, I’d argue it’s a bridge. Middleware solves the integration problem today, but it doesn’t solve the underlying issue of being on a platform that treats connectivity as an afterthought.

How to Evaluate a Fintech Partnership Without Getting Burned

The Sidecar Core Strategy

IDC projects that 40% of global banks will be pursuing sidecar core strategies by 2026, rising to 70-80% by 2028. A sidecar core runs alongside your existing system, handling specific functions — often digital account opening, real-time payments, or a new product line — through modern, API-native architecture while the legacy core continues to run the bulk of operations.

This is the pragmatist’s approach to core modernization. You don’t rip and replace. You build new capabilities on a modern platform and connect them to the legacy system through APIs. Over time, you migrate more functions to the sidecar until the legacy core is handling less and less.

For community banks, the sidecar approach has real appeal. It limits risk, spreads cost over time, and lets you prove value before committing to a full migration. The catch is that it requires your legacy core to have at least basic API connectivity — which brings us back to the fundamental question of what your current vendor is willing to provide.

Stop Calling It Digital Transformation

What the Regulators Are Signaling

The OCC’s two RFIs in 2025 — one on community bank digitalization, one specifically on core service providers — are not casual inquiries. The agency is building a record. The questions in the November RFI are pointed: they ask about innovation barriers, due diligence transparency, costs, billing errors, and whether current regulatory frameworks adequately address the power imbalance between community banks and their core vendors.

In October 2025, the OCC also issued several bulletins designed to reduce regulatory burden on community banks with assets up to $30 billion. The direction is clear: regulators want community banks to be able to compete digitally, and they’re starting to recognize that core vendor dynamics are a structural barrier.

This doesn’t mean regulation is imminent. But it does mean that community banks have political tailwind if they push their core vendors harder on API access, pricing transparency, and data portability. The “we’ve always done it this way” defense is losing ground with both the market and the regulators.

The Compliance Trap: How Regulatory Fear Kills Innovation

A Practical Framework for Your API Strategy

Here’s what I’d actually do if I were a community bank CEO looking at this landscape today.

Audit your current state. How many third-party tools does your bank use? How are they connected to the core? What are you paying in integration fees, click charges, and professional services? Most banks don’t have a clear picture of this, and you can’t negotiate what you can’t quantify.

Read your contract. Specifically, the API access provisions, data portability clauses, and termination terms. The ABA’s 2020 survey found that more than half of banks cited fees for third-party implementation and upgrade fees as their most problematic contract provisions. Know what you signed.

Demand a published API catalog. When your contract comes up for renewal, make API documentation and access a non-negotiable term. If your vendor can’t or won’t provide a published catalog of available APIs, pricing, and access terms, that tells you everything about their strategic direction.

Evaluate middleware as a bridge. If you’re mid-contract with a legacy core, a middleware platform can give you API connectivity now while you plan your longer-term strategy.

Put a sidecar strategy on the roadmap. Even if a full core switch isn’t realistic in the next two years, identify one or two functions — digital account opening is the most common starting point — where a modern, API-native sidecar could deliver immediate value.

Watch what the OCC does next. The regulatory record being built in 2025 could lead to concrete guidance or rulemaking in 2026-2027. Community banks that have already audited their vendor relationships and documented their constraints will be best positioned to benefit.

The Real Cost of Your Core Banking System

The Bottom Line

Your core system’s API strategy is not a technology decision. It’s a business strategy decision. It determines how fast you can move, what it costs you to innovate, and whether you control your own roadmap or rent it from a vendor.

The API economy rewards openness. Community banks that demand open, documented, fairly priced API access from their core providers — or find workarounds through middleware and sidecar strategies — will be the ones that can actually adopt the fintech tools, AI capabilities, and digital experiences their customers expect.

The ones that accept whatever their core vendor offers by default will keep spending 40 cents of every core dollar on the privilege of connecting their own systems together. That’s not a technology problem. That’s a negotiation problem. And it’s one community banks can solve — if they decide to.