The Board Problem: Why Community Bank Boards Are the Biggest Barrier to Growth

Most community bank boards lack the technology and marketing expertise needed to compete today. Here's why board composition is the real growth barrier — and what to do about it.

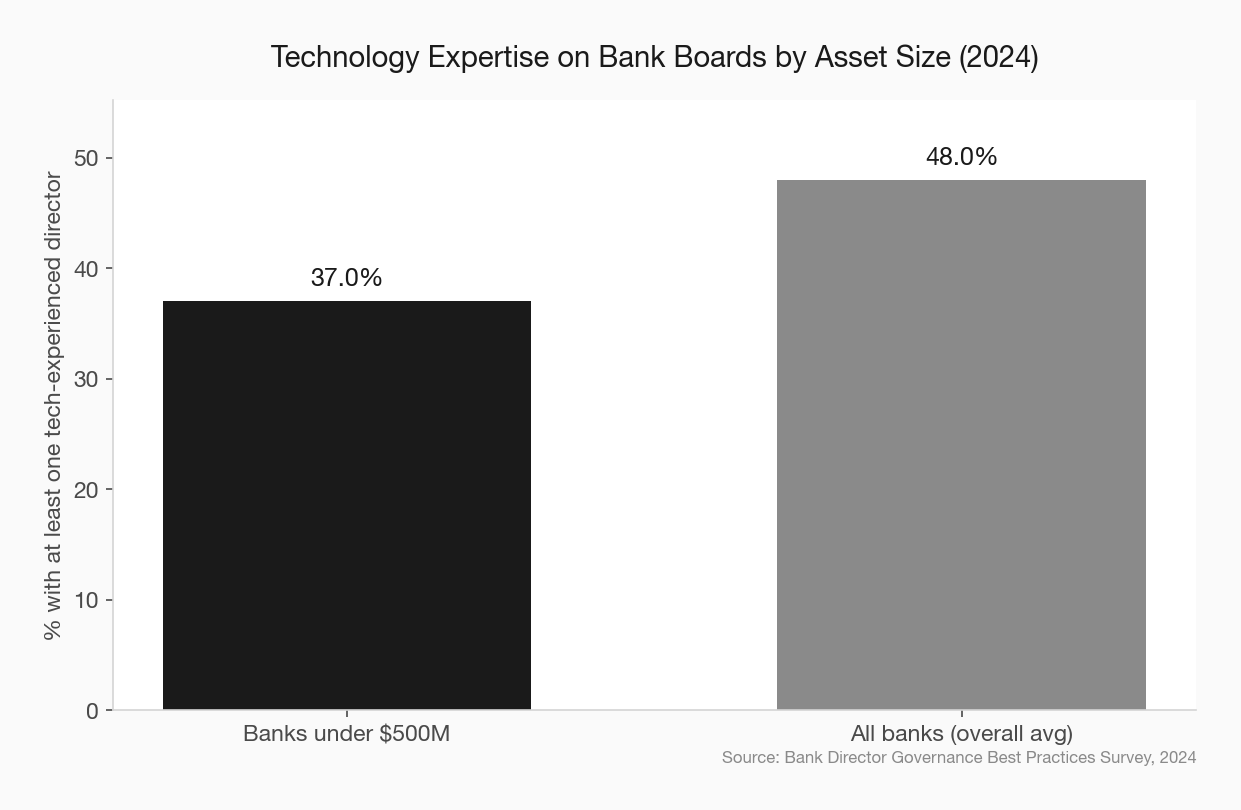

In 2024, only 37% of community banks with under $500 million in assets had a single person with technology experience on their board. Not a technology committee. Not a digital advisory panel. One person.

That number comes from Bank Director’s 2024 Governance Best Practices Survey. Sit with it for a moment. Community banks are losing ground to fintechs, neobanks, and megabanks on technology, digital experience, and brand — and the people responsible for strategic direction are overwhelmingly making decisions without anyone in the room who has ever shipped a product, run a digital campaign, or built a tech stack.

This is not a management problem. It’s a governance problem. And it starts at the top.

The Structural Bias Nobody Talks About

Community bank boards are built for stability. That was the right design for decades. A board full of long-tenured local business owners, attorneys, and accountants made sense when the competitive environment was stable and the primary risks were credit and interest rate risk.

That environment no longer exists.

The average board tenure at community banks runs 7 to 10 years. Some individual directors have served 15 to 20. These are not bad people — many of them are deeply committed to their communities. But long tenure creates a structural bias: toward the familiar, the incremental, and the safe. When someone has spent a decade on a board that never moved fast, velocity looks reckless.

The result is that community banks default to the status quo at exactly the moment the industry requires urgency.

why community banks are losing ground to fintechs

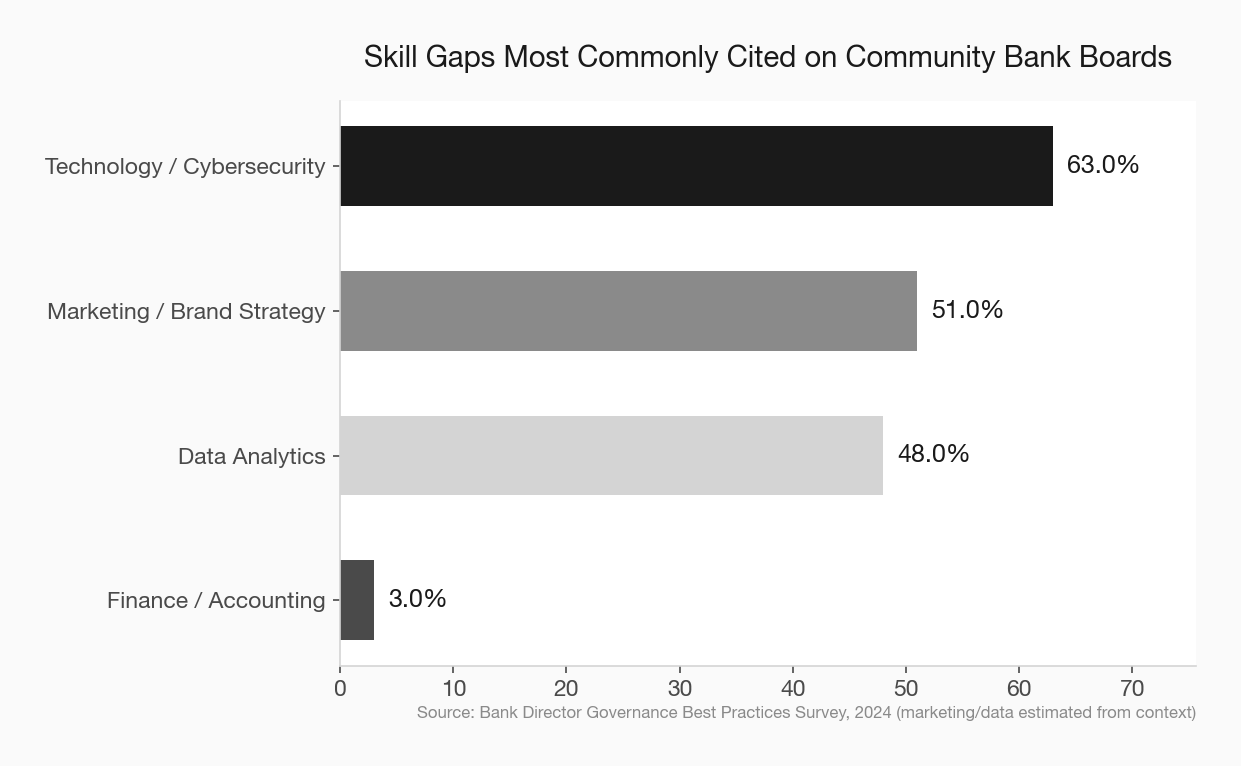

What’s Missing Isn’t Just Tech

The technology expertise gap is the most obvious symptom, but it’s not the only one. Marketing is just as underrepresented.

Most community bank boards have zero members with professional marketing or brand-building experience. Some have a business owner who does their own marketing. That’s not the same thing. When the marketing budget comes up for review, the people around the table don’t have the vocabulary to evaluate whether a website redesign is worth $200,000 or whether the bank’s social strategy is a liability.

So they cut. Or they approve the same plan they approved last year. Or they defer to whatever the local marketing firm pitched.

why your bank’s website is costing you deposits

Compare that to fintech boards. Chime, SoFi, and other consumer fintechs have boards stacked with former consumer product executives, marketers, and technologists. They didn’t get their brand right by accident. They got it right because the people setting strategy understood branding as a competitive weapon, not a line item.

The Compliance Comfort Zone

Here’s how the conversation typically goes when a community bank board encounters a new initiative: someone raises a compliance concern. The initiative slows down for review. The review takes months. By the time it clears, the window has passed or the team has moved on.

how regulatory fear kills community bank innovation

Compliance caution is not wrong. What’s wrong is using compliance as a ceiling rather than a framework.

Banks that are growing — and there are community banks that are genuinely growing — have boards that ask a different question. Not “could this create a compliance issue?” but “what would we need to do to manage this compliantly?” The first question is a veto. The second is a path forward.

Board composition drives this. Directors who have navigated regulatory environments in other industries — healthcare, financial services, technology — understand compliance as a design constraint, not a stop sign. Directors who have only ever seen compliance from inside a conservative banking culture tend to treat any gray area as a red light.

The Consolidation Tax

The community banking sector has lost more than 2,000 institutions since 2014. There were over 6,100 community banks a decade ago; fewer than 4,100 remain today, according to ICBA data. Some of that consolidation is inevitable. Much of it is not.

Banks that get acquired or merged out of existence often share a pattern: years of flat growth, underinvestment in technology and marketing, and an inability to attract the next generation of customers. These are strategy failures. And strategy is set by the board.

When a bank runs the same undifferentiated playbook for five years — same products, same channels, same messaging, same website from 2017 — it’s not bad luck. It’s governance. Someone at the top was comfortable enough with “fine” to never push for “better.”

the deposit wars and how to compete without destroying margins

A board that asks hard questions about growth — what is our share of new accounts opened in this market? What percentage of our loan applications start online? What does our brand mean to a 35-year-old in this town? — forces management to find answers. Most community bank boards aren’t asking these questions because they don’t know they’re the right questions to ask.

What Good Board Composition Looks Like

This is not an argument for replacing every long-tenured director with a Silicon Valley transplant. It’s an argument for intentional recruitment.

A community bank board of eight to twelve people can carry significant expertise in finance, law, credit, and community relationships — and still make room for one or two directors with technology, marketing, or consumer-experience backgrounds. The research supports this: MIT found that companies with three or more digitally savvy directors showed statistically better performance in revenue growth and return on assets. You don’t need a majority. You need critical mass.

Concrete steps worth taking:

- Audit your board’s expertise map. List every current director’s professional background and identify where the gaps are. Most boards have never done this formally.

- Set term limits. This is the single most effective structural change a board can make. Not to force out good directors, but to create natural renewal cycles that allow new expertise to enter.

- Recruit differently. Stop looking only at the bank’s existing customer and business network. A fintech founder, a regional CMO, a health system CIO — these people exist in most markets and bring exactly the outside perspective that governance needs.

- Create advisory roles if full board seats aren’t available. Some banks have launched technology advisory committees or marketing advisory boards that feed into board-level strategy discussions. This is a reasonable interim step, though it shouldn’t be a substitute for real board composition change.

The ICBA launched an AI Readiness Survey for community bank boards in 2025 specifically because this gap has become impossible to ignore. If the industry association is telling you to assess your board’s AI readiness, the question is not whether this matters. It’s how long you can afford to wait.

The Real Risk

Community bank boards talk about risk constantly. Credit risk. Interest rate risk. Liquidity risk. Regulatory risk. These conversations are necessary.

But there is a category of risk that most community bank boards underweight: the risk of irrelevance. The risk that five years from now, the next generation of customers, employees, and business owners in your community doesn’t think of your institution as the obvious choice — or doesn’t think of it at all.

That risk is not managed by the credit committee or the ALM model. It is managed by leadership with the courage to ask uncomfortable questions about where the bank is headed and the expertise to understand what the answers mean.

A board built for 2005 cannot manage that risk. It doesn’t have the tools.

The good news is that this is fixable. Board composition is a choice. The banks that make the right choice now will have a meaningful structural advantage in five years over the ones that kept renominating the same twelve people.