The Community Bank Email Marketing Playbook Nobody Has Written Yet

Community banks blast rate sheets to everyone or send nothing at all. Segmented, lifecycle email is the highest-ROI channel most banks ignore. Here's how to fix it.

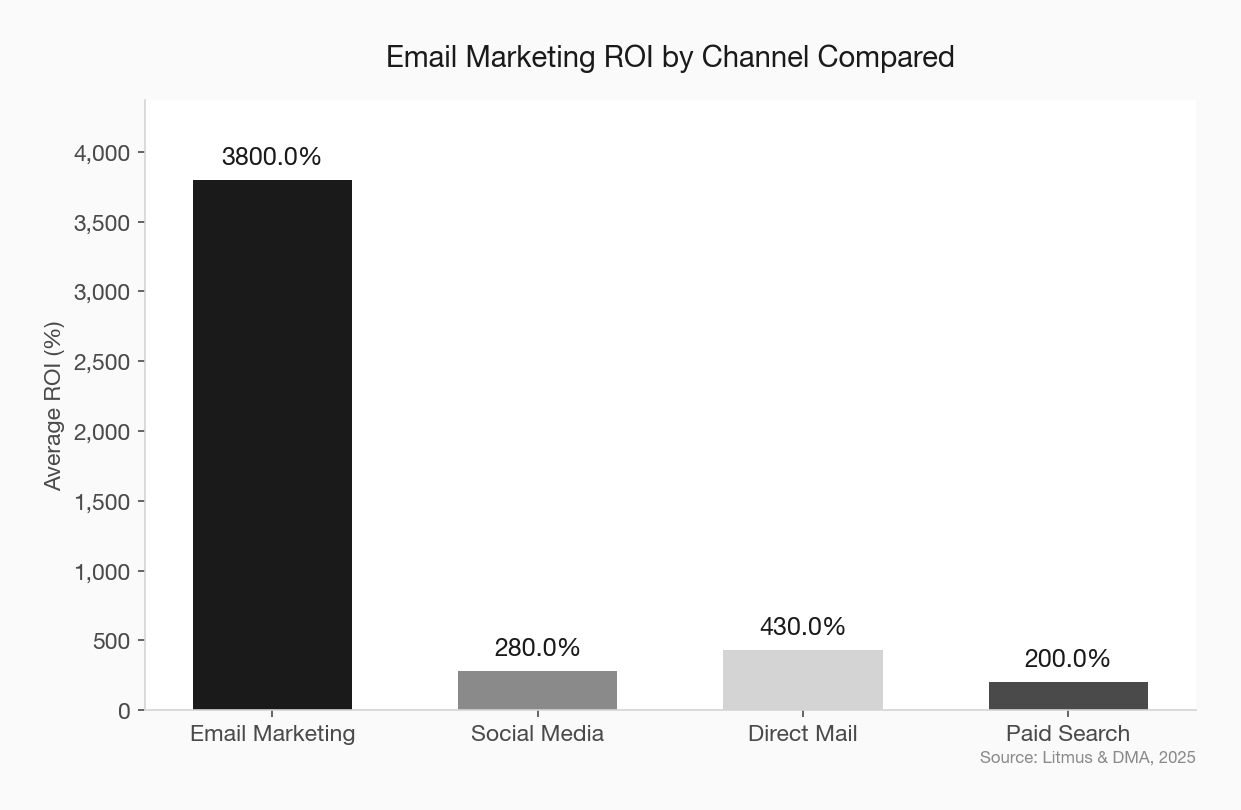

Email marketing returns an average of $36 to $42 for every dollar spent, depending on whose data you trust. That makes it the single highest-ROI marketing channel available to any business, in any industry, full stop. And community banks are barely using it.

Most community bank email programs fall into one of two categories: nonexistent, or a monthly blast of the same rate sheet to every address in the database. Neither qualifies as a strategy. Meanwhile, fintechs are running segmented lifecycle campaigns that nudge customers from onboarding to cross-sell to referral with surgical precision. The gap is not technology. It is effort and intent.

This is the playbook for closing that gap.

The State of Email at Most Community Banks

Let’s be direct about where things stand. The average financial services email sees a 27% open rate, which is actually decent compared to most industries. Banking customers overwhelmingly prefer email for non-urgent communication – 89% of them, according to industry surveys. The channel works. The audience wants it.

The problem is what banks are sending.

A typical community bank email program looks like this: a quarterly newsletter with a message from the president, a rate update, and maybe a community event photo. Every customer gets the same thing. There is no segmentation by product, behavior, or lifecycle stage. There is no automation. There is no measurement beyond “we sent it.”

This is not email marketing. This is digital junk mail.

The numbers are not subtle. Email outperforms every other marketing channel available to a community bank by a wide margin. The question is not whether to invest in email. The question is why you haven’t already.

Why Segmentation Is the Whole Game

Here is the single most important thing to understand about email marketing: segmented campaigns generate up to 760% more revenue than non-segmented blasts.

Read that again. Seven hundred and sixty percent.

The reason is straightforward. A 35-year-old first-time homebuyer and a 62-year-old business owner with $2M in deposits do not need the same message. Sending them the same email is not just ineffective – it actively trains both of them to ignore you.

Community banks already have the data to segment well. Your core system knows which customers have a checking account but no savings. It knows who opened a CD six months ago that is about to mature. It knows which business accounts have growing balances that might benefit from a treasury management conversation.

You are sitting on segmentation gold and using it for nothing.

The Five Segments Every Community Bank Should Start With

You do not need 50 segments. You need five.

New account holders (0-90 days). These customers are in the decision-confirmation window. They just chose your bank and they are looking for signals that they made the right call. This is your highest-leverage moment.

Single-product households. Customers with one product are the most likely to leave. Every additional product increases retention dramatically. These customers need cross-sell content, not rate sheets.

CD maturity approaching (30-60 days out). This is a defined event with a known date. If you are not emailing these customers before their CD matures, you are handing deposits to whoever has the best rate on Bankrate that week.

Dormant accounts (no activity in 90+ days). These customers have not closed their account, but they have stopped using it. A re-engagement sequence is the difference between recovering the relationship and watching the account quietly close.

Business banking customers. Their needs, language, and decision-making process are fundamentally different from retail customers. Lumping them together is a choice to be mediocre at both.

The Four Automated Sequences That Actually Move Numbers

Automation is where email marketing shifts from a task on someone’s to-do list to a system that runs while your team focuses on relationships. These four sequences cover the lifecycle moments that matter most.

1. The Welcome Sequence (Triggered: Account Opening)

This is the most important email sequence your bank will ever build. Data from credit unions running automated onboarding shows welcome email open rates above 70%. That is not a typo. People who just opened an account want to hear from you.

A strong welcome sequence runs 5-7 emails over the first 90 days:

- Email 1 (Day 0): Thank you, here’s how to set up mobile banking and direct deposit. No fluff.

- Email 2 (Day 3): Introduce your mobile app features. Link directly to the app store.

- Email 3 (Day 7): Meet your banker. Include a real name, a real photo, and a direct phone number.

- Email 4 (Day 14): Financial tip relevant to their account type. For checking customers, maybe it’s setting up automatic savings transfers.

- Email 5 (Day 30): Soft cross-sell. “Customers like you also use…” based on their account type.

- Email 6 (Day 60): Ask for a Google review. They have been with you long enough to have an opinion.

- Email 7 (Day 90): Check-in from their banker. “How’s everything going?” with a link to schedule a call.

The goal is not to sell in every email. The goal is to make the customer feel known and supported so that when you do make an ask, it lands.

2. The Cross-Sell Sequence (Triggered: Product Gap Detection)

Your core system can identify product gaps. A customer with checking but no savings. A business account with no line of credit. A mortgage customer with no home equity line.

Each gap should trigger a 3-email sequence spaced 7-10 days apart:

- Email 1: Educational content about the product category. No pitch. Just value.

- Email 2: A customer story or use case. “Here’s how a local business used our line of credit to manage seasonal cash flow.”

- Email 3: A direct offer with a clear call to action and a named contact to reach out to.

Michigan State University FCU tested needs-based segmentation against traditional demographic targeting and saw 63% more clicks and 80% more product opens. The data is clear: relevance beats reach every time.

3. The CD Maturity Sequence (Triggered: 45 Days Before Maturity)

This one is almost criminal to ignore because the timing is perfectly predictable.

- Email 1 (45 days out): “Your CD matures on [date]. Here are your current renewal options.”

- Email 2 (30 days out): “Rates have [moved/held steady]. Here’s what a renewal looks like at today’s rates.”

- Email 3 (14 days out): “Your CD matures in two weeks. Call [name] at [number] or click here to renew online.”

Without this sequence, you are letting maturing CDs turn into rate-shopping events. With it, you are framing the conversation before anyone else does.

4. The Re-Engagement Sequence (Triggered: 90 Days of Inactivity)

Dormant accounts are silent attrition. A 3-email re-engagement sequence costs almost nothing and can recover relationships worth thousands in lifetime value.

- Email 1: “We noticed it’s been a while. Is there anything we can help with?”

- Email 2 (7 days later): Highlight a feature or product they may not know about.

- Email 3 (14 days later): “We’d hate to lose you. Here’s a direct line to someone who can help.”

If they do not respond to the third email, flag the account for a personal phone call from a banker. The email sequence is triage. The human follow-up is where community banks have an advantage no fintech can replicate.

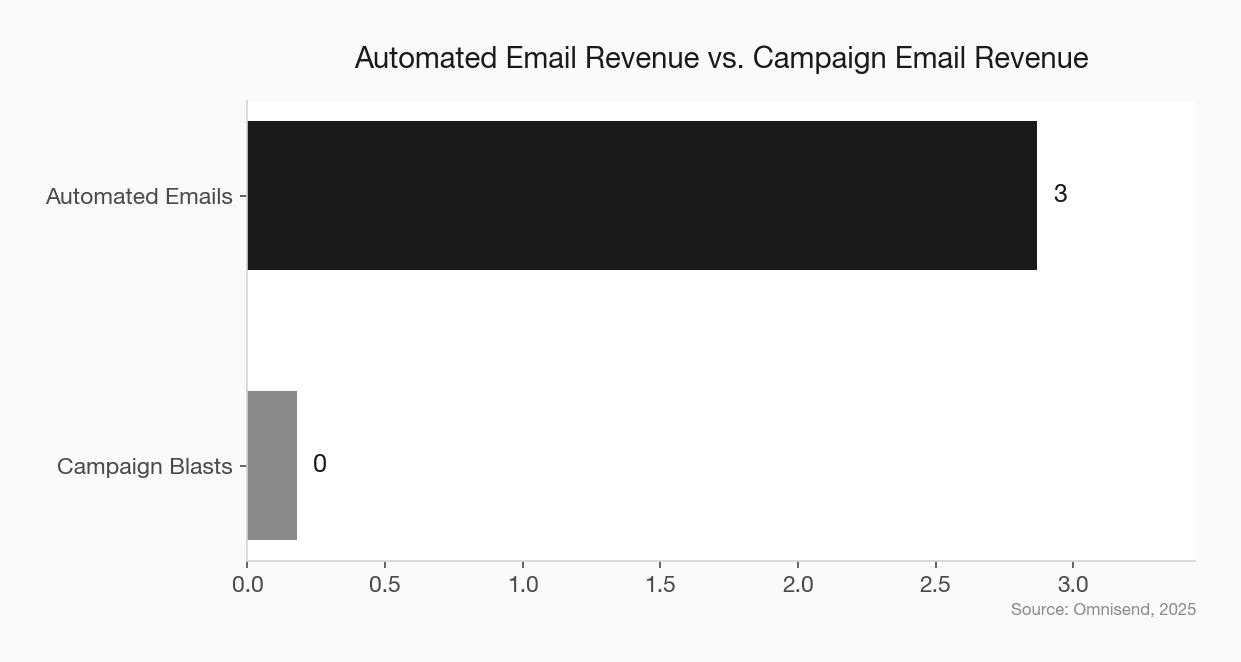

Automated emails generate $2.87 per email sent. Campaign blasts generate $0.18. That is a 15x difference. If you do nothing else from this article, build one automated sequence.

What to Measure (And What to Stop Measuring)

Open rates used to be the gold standard. They are not anymore. Apple’s Mail Privacy Protection, which covers 64% of Apple Mail users, pre-loads images and inflates open rates. If you are reporting open rates to your board as a primary metric, you are presenting unreliable data.

Here is what to track instead:

Click-through rate (CTR). This tells you whether people found your content compelling enough to act on. Financial services averages about 2-3%. If you are below 1%, your content needs work. Above 4%, you are doing something right.

Conversion rate. Did the email lead to an application, a scheduled appointment, or an account opening? This is the only metric that connects email to revenue. Banking email conversion rates average around 21%, which is remarkably high compared to other industries.

Revenue per email. Total revenue attributed to email divided by emails sent. This is the number your CEO and board actually care about.

Unsubscribe rate. If it is above 0.5% per send, you are either sending too often or sending irrelevant content. Behavior-based personalization drives unsubscribe rates down to 0.13%.

List growth rate. A healthy email list grows. If yours is shrinking, you have a collection problem at the branch and on your website.

community bank marketing metrics that matter

The Tech Stack Does Not Need to Be Complicated

Community bankers hear “marketing automation” and picture a six-figure platform that requires a dedicated team. That is not the reality anymore.

A community bank email program needs three things:

An email service provider (ESP). Mailchimp, Constant Contact, or ActiveCampaign all work fine for institutions under $1B. You are looking at $100-500 per month depending on list size. This is not a budget problem.

A data connection to your core. This is the hard part, but it is getting easier. Most modern cores can export customer data on a schedule. Some ESPs offer direct integrations with banking cores. If your core vendor tells you this is impossible, they are either wrong or you have a core problem worth addressing separately. community bank core system cost analysis

Someone who owns it. Not “the marketing team” as a collective noun. One person whose job includes email marketing as a named responsibility with time allocated to it. If email is everyone’s job, it is no one’s job.

You do not need AI-powered personalization engines or predictive analytics platforms to start. You need a list, segments, and four automated sequences. Everything else is optimization.

The Compliance Question (It Is Simpler Than You Think)

Every community banker who reads this will think: “What about compliance?”

Fair. But email marketing compliance is not the obstacle most banks make it out to be.

CAN-SPAM requires an unsubscribe link, a physical address, and no deceptive subject lines. You are already doing this if you are sending any email at all.

For financial product promotion, the same rules apply as any other advertising channel. Reg DD disclosures on deposit products. Reg Z disclosures on credit products. Your compliance team already reviews print ads and website content. Email is the same review process applied to a different channel.

The banks that are stuck are not stuck on compliance. They are stuck on comfort. There is a difference.

compliance and community bank innovation

A 30-Day Launch Plan

If you are starting from zero, here is how to get a working email program live in 30 days:

Week 1: Audit and setup. Export your customer email list from your core. Clean it. Remove duplicates, fix formatting, remove obviously invalid addresses. Set up an ESP account. Import your list.

Week 2: Segment and build. Create your five core segments. Write your welcome sequence (7 emails). You do not need to write all four sequences at once. Start with welcome.

Week 3: Compliance review and test. Run your welcome sequence through compliance review. Send test emails to internal staff. Fix subject lines, preview text, and formatting.

Week 4: Launch and measure. Turn on the welcome sequence for all new accounts. Send one segmented campaign to your single-product household segment. Measure CTR and conversions.

That is it. No six-month implementation timeline. No $200,000 consulting engagement. One month, one sequence, one segmented send.

90-day marketing plan for new community bank CMO

The Competitive Advantage Hiding in Your Inbox

Here is what fintechs understand that most community banks do not: email is not a broadcast channel. It is a relationship channel. Every email is either building trust or eroding it.

Community banks have a structural advantage in email marketing that they are completely wasting. You know your customers by name. You know their financial lives. You know when their CD matures, when their business account balance dips, when they have not visited a branch in three months. That data is a relationship engine waiting to be turned on.

The fintech sending a generic “rates are up” push notification cannot compete with a community bank sending a personalized email from a named banker who says, “Sarah, your CD matures in 30 days. Based on your goals, here are two options I’d recommend. Call me if you want to talk through it.”

That email takes 90 seconds to template and zero seconds to send once it is automated. And it is worth more than every billboard, radio spot, and rate sheet your bank has produced in the last year combined.

The playbook is not complicated. It is just unwritten at most community banks. Now it is written. The only question is whether you will run it.

community bank deposit competition strategy