The Neobank Shakeout: What Community Banks Should Do While Fintechs Are Hurting

76% of neobanks are unprofitable and VC funding has cratered. Community banks have a narrow window to recapture customers who tried fintechs and were disappointed.

Three years ago, community bankers watched neobanks raise billions, steal headlines, and vacuum up younger customers with slick apps and zero fees. The story felt inevitable: digital wins, incumbents lose.

That story is falling apart.

Chime went public in June 2025 at an $11.6 billion valuation — a 54% haircut from its $25 billion peak in 2021. Despite $2.19 billion in revenue, it posted a GAAP net loss of $1.01 billion. At least 16 neobanks have shut down globally in the past two years. Consulting firm Simon-Kucher estimates that only 5% of the world’s roughly 400 digital banks are actually reaching breakeven. And the Synapse bankruptcy froze $265 million in customer deposits, exposing a gap between fintech marketing promises and banking reality.

This is not the time to gloat. This is the time to move.

The Numbers Tell a Clear Story

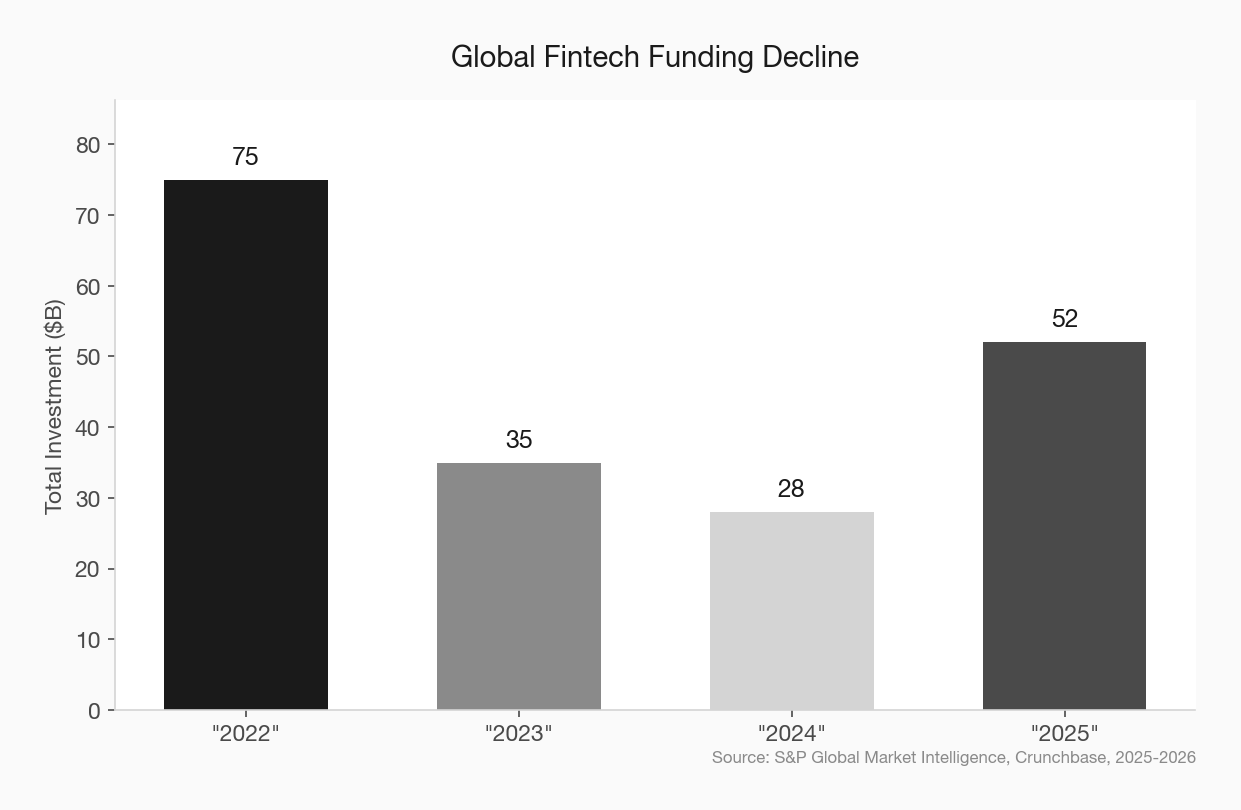

The neobank funding environment has fundamentally shifted. Global fintech investment dropped 20% in 2024 to roughly $28 billion, with North America experiencing a steep 39% decline. The “growth at any cost” era that funded free checking accounts, cashback rewards, and aggressive customer acquisition is over. Investors now want unit economics that make sense — and most neobanks can’t deliver them.

While 2025 showed a partial recovery — Crunchbase reported global fintech startup funding rose 27% to $51.8 billion — the money is flowing to infrastructure and AI, not consumer neobanks. The days of a digital bank raising $400 million on user growth alone are done.

The result: 76% of neobanks remain unprofitable in 2025, according to industry analysis. Most earn less than $30 in revenue per customer per year. That math doesn’t work when customer acquisition costs run $50 to $200 per account.

Why Neobank Customers Are Vulnerable

Here’s what the satisfaction surveys don’t capture: neobank customers are loosely held.

Yes, digital bank users report high satisfaction — roughly 63% say they’re “very satisfied,” compared to 55% at traditional banks. But satisfaction and loyalty are different animals. Most neobank relationships are shallow. A Chime or Cash App account is a secondary spending tool, not a primary financial relationship. When something goes wrong — and things have been going wrong — there’s no branch to walk into, no loan officer who knows your name, no human to call.

The Synapse collapse made this viscerally real. When the middleware company filed for bankruptcy in April 2024, customers at neobanks like Yotta and Copper suddenly couldn’t access their money. The bankruptcy trustee identified a shortfall between $65 million and $95 million. The CFPB eventually allocated $46.2 million to reimburse victims — but the trust damage was done.

This isn’t an isolated incident. It’s a structural vulnerability of the neobank model. When your “bank” is actually a fintech app layered on top of a partner bank through a middleware company, the chain of accountability gets murky fast. And customers are starting to notice.

The Window Is Open — But It Won’t Stay Open

Community banks have a narrow opportunity to recapture customers who tried neobanks and found them wanting. But this window has an expiration date. The strongest neobanks — Chime, Revolut, SoFi — are consolidating their positions. Chime expects to hit GAAP profitability in 2026, with projected revenue of $2.63-$2.67 billion and adjusted EBITDA margins of 14-15%. The survivors will be stronger, not weaker.

That means the next 12 to 18 months are the moment. Not to compete on features — you’ll lose that fight. But to compete on the things neobanks structurally cannot offer.

Four Moves to Make Right Now

1. Target the Synapse Generation

There is a cohort of consumers — particularly millennials and younger Gen X — who put real money into fintech apps and got burned. They learned that FDIC insurance doesn’t help much when a middleware company goes bankrupt and nobody can figure out which bank actually holds your deposits.

These people are not anti-technology. They’re anti-risk. They want the convenience of digital banking with the stability of a real bank. Community banks should be marketing directly to this fear — not with scare tactics, but with clarity.

The message: “Your money is here. In this building. Insured, accounted for, and accessible. No middleware. No layers. Just a bank.”

How community banks can compete on trust in a post-Synapse world

2. Fix Your Digital Front Door

The irony of the neobank shakeout is that it doesn’t lower the bar for digital experience — it raises it. Customers who tried Chime and are now open to a community bank still expect a clean mobile app, instant notifications, and online account opening that doesn’t require a fax machine.

You don’t need to match Chime’s interface pixel for pixel. But you do need to clear a minimum threshold. If your online account opening process still takes more than five minutes or requires an in-branch visit, you will lose these customers before they ever walk through your door.

The fix isn’t a full digital transformation. It’s three things: a modern mobile app (most core providers offer one now), online account opening with instant ID verification, and Zelle or a comparable peer-to-peer payment option. That’s the table stakes.

Online account opening conversion rates at community banks

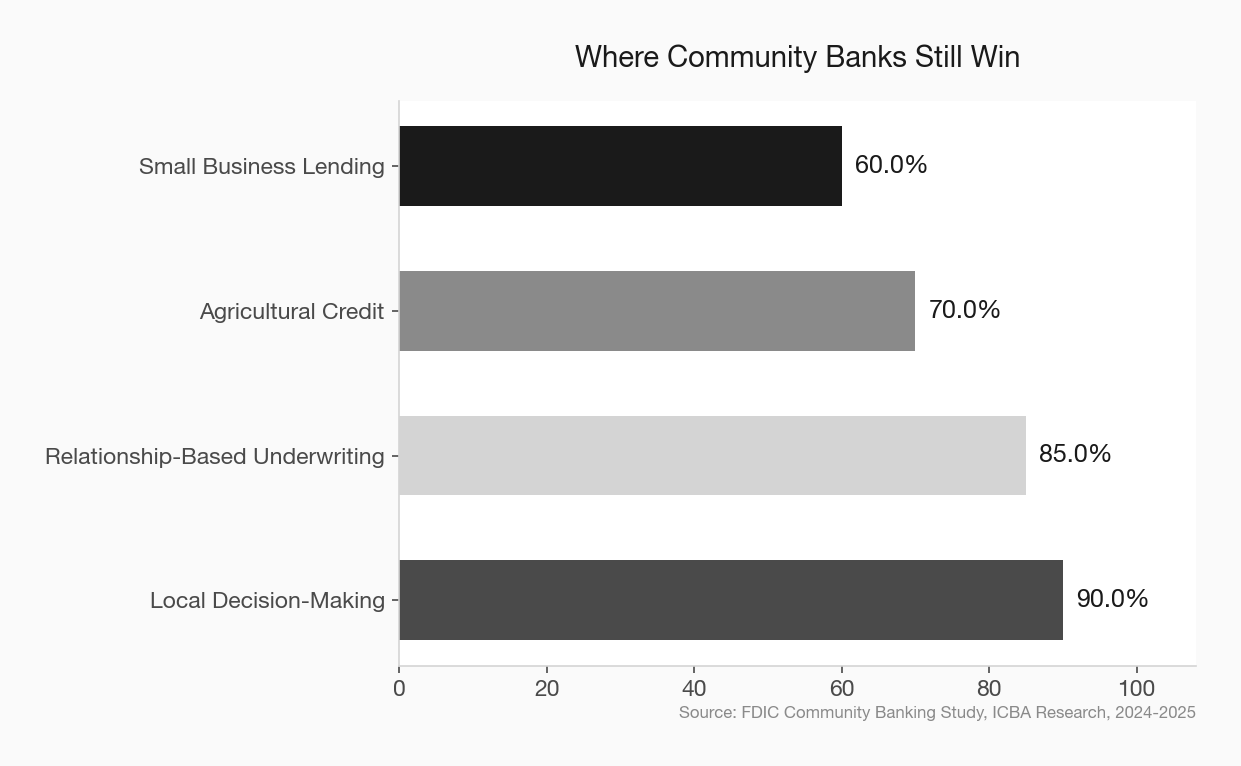

3. Lead With Your Lending Advantage

Here’s Chime’s fundamental weakness, straight from its own S-1 filing: it doesn’t do meaningful lending. Chime’s revenue is almost entirely interchange and fees. It offers a small-dollar “SpotMe” overdraft product, but it’s not making mortgage loans, SBA loans, or commercial credit decisions.

This matters because lending is where banking relationships deepen. A checking account is a utility. A business loan is a partnership. Community banks that emphasize their lending capability — particularly small business and agricultural credit — are playing a game neobanks literally cannot play.

The neobank shakeout hasn’t changed this dynamic — it’s amplified it. As fintech lending platforms face their own funding pressures, community banks with strong credit cultures and local expertise are more valuable, not less.

The small business lending story no fintech can tell

4. Tell the Stability Story — With Data

Community banks have a trust problem they don’t deserve. Younger consumers assume that a 120-year-old bank with a marble lobby is somehow less safe than an app that launched in 2018. That’s a marketing failure, not a product failure.

Fix it with specifics. Put your capital ratios on your website. Show your FDIC certificate. Publish how many years you’ve been in continuous operation. Create content that explains — in plain language — why depositing money at your bank is fundamentally different from depositing it at a fintech app that partners with a bank you’ve never heard of through a middleware company you didn’t know existed.

The Synapse story is your best proof point. Not as a weapon against fintechs, but as a clear illustration of why banking structure matters.

Why your bank’s stability is a brand asset you’re underusing

What Not to Do

A few temptations to resist:

Don’t compete on rate. Some neobanks still offer high-yield savings accounts as loss leaders. Matching those rates will destroy your margins and attract rate-chasers who will leave the moment someone offers 10 more basis points. Compete on relationship, not rate.

Don’t celebrate neobank failures publicly. It looks petty and it alienates the exact customers you’re trying to attract — people who used those products and may feel defensive about their choices. Take the high road. Offer solutions, not commentary.

Don’t assume this fixes itself. The neobank shakeout is culling the weak players, but the strong ones are getting stronger. Chime’s path to profitability is real. SoFi is building a full banking platform. Revolut just crossed 50 million global users. The competitive pressure isn’t going away — it’s concentrating.

The Real Opportunity

The neobank shakeout isn’t about fintechs failing. It’s about the market finally demanding that digital banking businesses operate like actual banks — with real revenue models, real risk management, and real accountability for customer deposits.

Community banks have been doing that for decades. The difference is that now, for the first time in years, a meaningful number of consumers are ready to hear that message.

The banks that move quickly — upgrading their digital minimum, sharpening their marketing, and telling a clear story about stability and lending — will capture customers they couldn’t have reached two years ago. The banks that wait for this moment to pass will watch those same customers settle into the surviving neobanks, this time for good.

How to build a community bank marketing strategy that actually works

The window is open. Walk through it.