The Real Cost of Your Core Banking System (And Whether It's Worth It)

Most community banks underestimate their core system's true cost by 70–80%. Here's the framework for calculating what you're actually paying — and when to consider switching.

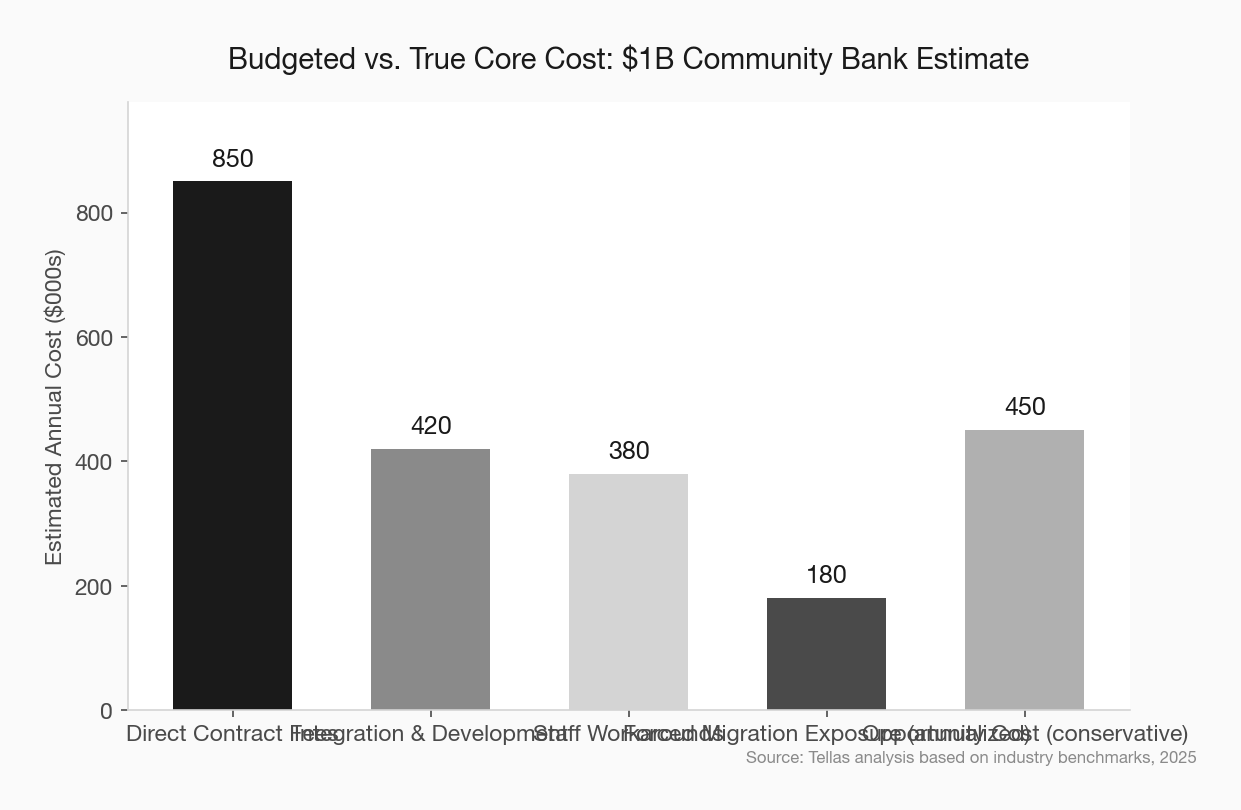

Your core contract says $700,000 a year. Your actual cost is closer to $2.4 million.

That gap — between what banks budget for their core and what it actually costs when you account for integration fees, workarounds, compliance overhead, and lost opportunity — is one of the most consequential blind spots in community banking. Most executives never run the full calculation. Most boards never see it.

The number matters because it changes the decision. Switching cores is expensive and disruptive — but so is staying. You can’t make a rational call about your technology roadmap if you’re only looking at half the ledger.

Here’s the framework for calculating your true core cost, and the signs that the math is finally turning against staying.

The Sticker Price Is a Fiction

A $1 billion community bank typically pays $500,000 to $1.2 million annually in direct core system fees. That’s the number in your budget. That’s the number your CFO sees.

But according to Deloitte’s 2024 banking technology survey, financial institutions underestimate the true total cost of ownership of their core systems by 70–80%, with the average bank discovering real costs are 3.4 times higher than initially budgeted once every factor is counted.

Three-point-four times.

The sticker price covers the license. The true cost covers everything else — and everything else adds up fast.

The Five Cost Categories Nobody Budgets For

1. Integration Fees

The Big Three core providers — FIS, Fiserv, and Jack Henry — control roughly 90% of the community bank market. Their legacy architectures were not designed for the API-connected ecosystem that banking runs on today. Every new fintech partnership, every new digital tool, every third-party integration has to fight through a system built before smartphones existed.

The result: custom coding, middleware, and professional services charges for things that should be table stakes. Bankers describe multi-year delays and inflated costs just to connect fraud detection tools or digital account opening platforms to their core. Those fees don’t appear on the core contract. They show up in IT project budgets, vendor invoices, and professional services line items — scattered across the P&L in ways that make the core look cheaper than it is.

2. Staff Time and Workarounds

Legacy cores generate manual work. When systems can’t talk to each other, people fill the gap. Loan officers reconcile spreadsheets. Operations staff re-enter data between systems. Compliance teams build manual reporting workarounds because the core can’t generate the output the examiners want.

That time has a cost. The OCC’s November 2025 Request for Information on core providers noted specific concerns about “overly-complicated and lengthy billing statements that require considerable bank resources to understand and review.” That’s one example. Multiply it across every department that interfaces with the core, and you’re looking at tens of thousands of staff hours per year — hours that could be going toward customer relationships, loan production, and the work that actually builds the bank.

3. Forced Upgrades and Sunsetting Products

This one is coming for a lot of banks right now. Fiserv has notified clients to migrate away from its Retail Online Banking (ROB) and Business Online Banking (BOB) platforms by December 2026. The products are being discontinued. The bank has to move — and in many cases, the bank is bearing the conversion cost for the vendor’s decision.

This is not a Fiserv-specific dynamic. Core vendors regularly sunset applications, forcing clients into migrations they didn’t plan or budget. When you’re evaluating the cost of your core, you need to ask: what products are being sunset in the next five years, and who pays when they do?

4. Deconversion Fees and Contract Terms

Buried in most core contracts are deconversion fees that make switching prohibitively expensive regardless of performance. The industry consultants who specialize in negotiating these contracts are direct about it: community banks that negotiate without expert help “have little chance of getting a fair deal” against the Big Three.

The OCC’s 2025 RFI flagged exactly this dynamic — describing “reduced competitive pressure,” “reduced negotiating power,” and “potentially anti-competitive forces” in the core provider market. The American Bankers Association called it “an important area of focus.” That’s regulatory language for: the vendors have the leverage and they know it.

If you’re within three years of renewal and you haven’t hired someone to help you negotiate, you’re going to get the terms your vendor wants, not the terms your bank needs.

5. Opportunity Cost

This is the hardest category to quantify and the one that matters most.

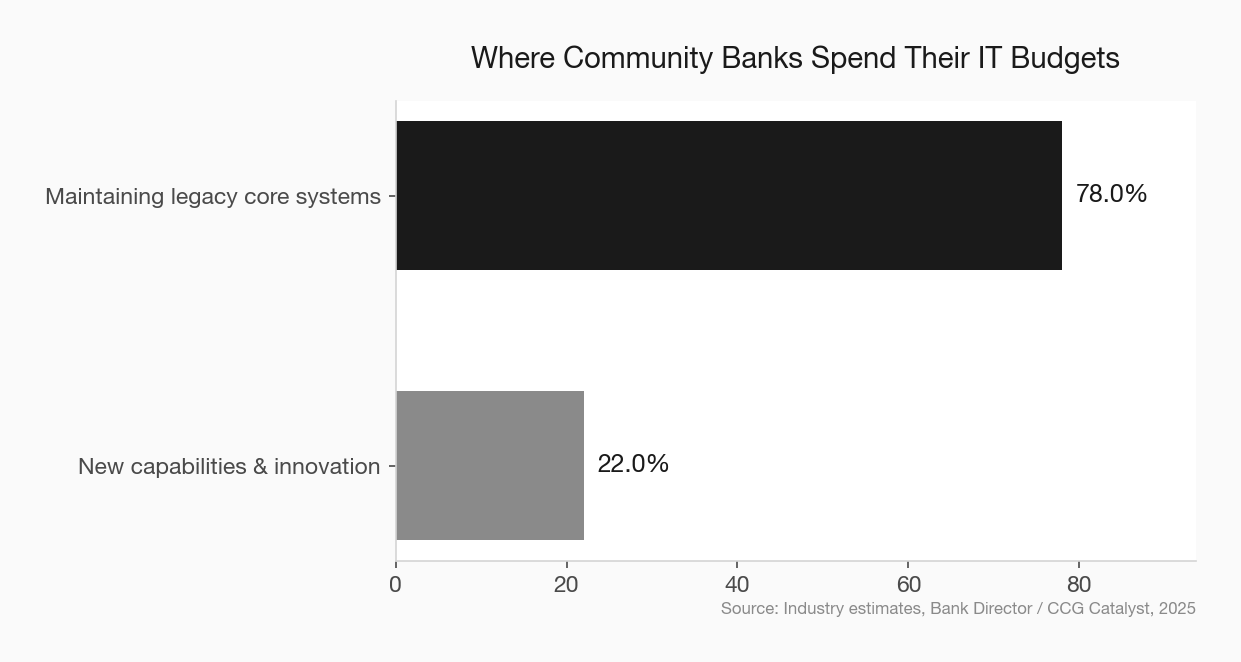

The ABA’s most recent core survey found that 35% of community banks are dissatisfied with their core processor and less than half would recommend their current provider to a peer. Banks spend up to 78% of their IT budgets maintaining legacy cores — not building new capabilities, not improving the customer experience, not competing. Maintaining.

Every month your team is managing a legacy core is a month they’re not building the digital account opening flow that converts. Every integration delay is a product launch that doesn’t happen. Every manual workaround is a loan officer spending time on data entry instead of a relationship.

McKinsey estimates that institutions who successfully modernize achieve 25% operational savings and a 65% reduction in time-to-market for new products. That’s not a technology outcome — that’s a revenue outcome.

The Framework: Calculating Your True Core Cost

Run this exercise before your next board technology discussion. It takes an afternoon with your CFO and your IT lead.

Direct costs (what you know): Annual core license fee, per-module and per-user charges, data processing fees, annual maintenance charges.

Integration costs (dig into IT project budgets): API connection fees, middleware costs, custom development for third-party tools, vendor professional services on core-related projects over the last three years.

Staff time (harder but doable): Estimate hours per week spent on manual workarounds, data re-entry, reconciliation, and core-related compliance reporting. Multiply by loaded labor cost. Annualize.

Forced migration exposure: Identify any products your core vendor has announced as end-of-life. Get a quote for the migration. That’s a liability on your technology balance sheet.

Opportunity cost (directional, not precise): What products have you delayed or declined to launch because of core limitations? What fintech partnerships have you passed on? Assign a conservative revenue estimate to one or two.

Most banks that run this exercise land at a true annual cost that’s two to three times their budgeted core spend. That number changes the math on switching.

So When Does Switching Make Sense?

Switching cores is genuinely hard. PeoplesBank, a $4.4 billion Massachusetts community bank, completed a migration to Nymbus in June 2025 — finishing 24 hours ahead of schedule. It was remarkable enough to make industry news precisely because most migrations don’t go that well.

The PeoplesBank model is instructive. They didn’t attempt a big-bang cutover. Starting in 2020, they launched a digital-only brand (ZYNLO Bank) on Nymbus as a sidecar core, validating the platform with real customers and real deposits before committing the whole institution. By the time the full migration happened, the technology was proven and the team had four years of experience with the platform. ZYNLO grew to $150 million in deposits before the main bank moved.

That’s a viable path for banks with the strategic patience to execute it. Not every bank has that — but the lesson holds: the sidecar strategy de-risks migration while your team builds the capability to do it right.

The case for switching gets stronger when:

- Your true core cost calculation exceeds what a modern replacement would cost on a five-year NPV basis, including conversion costs

- Your vendor has announced sunset products that force a migration anyway — at that point you’re already paying switch costs, you might as well control where you’re going

- Your core limitations are blocking specific revenue opportunities you’ve identified and quantified

- You have more than three years remaining on your contract (enough runway to negotiate and plan)

The case for staying — and optimizing — gets stronger when:

- You’re within 18 months of renewal (not enough time to manage a conversion responsibly)

- Your true cost calculation, while higher than budgeted, doesn’t materially change the NPV calculation against conversion

- You have specific negotiating leverage (the OCC’s current attention to anticompetitive core practices gives every community bank something to point to at the table)

community bank technology strategy and digital transformation

What to Do Before Your Next Renewal

Whether you’re switching or staying, three things should happen before you sign anything:

Run the true cost calculation. Do it this quarter, before you’re in renewal mode and time pressure is working against you.

Hire someone to help you negotiate. The consultants who specialize in core contract negotiation earn their fees many times over. This is not the place to go it alone against vendors who negotiate these contracts every day.

Use the OCC’s attention. The OCC issued a formal Request for Information in November 2025 specifically about anticompetitive practices in the core market. The ABA has a Core Platforms Committee and resources specifically for this. The regulatory environment has never been more favorable for community banks who want to push back.

fintech partnership evaluation framework for community banks community bank AI tools and digital strategy

The core system decision isn’t just a technology decision. It’s a profitability decision, a talent decision, and a competitive positioning decision. Treat it like one.