The Stablecoin Moment: What Community Banks Should Know Now That the Law Has Landed

The GENIUS Act passed in July 2025. Here's what community banks need to know about deposit risk, the yield loophole, and what to do before January 2027.

$33 trillion.

That’s how much moved through stablecoin networks in 2025, according to Bloomberg — a 72% increase over the prior year. Not held. Moved. That number approached the annual GDP of the United States, transacted through digital dollars that bypass traditional banking rails entirely.

The GENIUS Act — the Guiding and Establishing National Innovation for U.S. Stablecoins Act — was signed into law on July 18, 2025. Full implementation is set for January 18, 2027. That gives community banks roughly 18 months to build a strategy, brief their boards, file with regulators, or at minimum decide where they stand.

Most community banks have used close to none of those months productively.

This isn’t a trend to monitor. The law is on the books. The FDIC is writing implementation rules. The clock is running. The question is what community banks will do with the time they have left.

What the GENIUS Act Actually Does

The GENIUS Act creates the first federal regulatory framework for “payment stablecoins” — digital assets redeemable at a fixed value, typically 1:1 with the US dollar. It designates three types of permitted issuers:

- Subsidiaries of insured depository institutions

- Federal-qualified nonbank payment stablecoin issuers

- State-qualified payment stablecoin issuers

The first category is the opening that matters for community banks. A bank subsidiary can be approved as a licensed stablecoin issuer. Under FDIC proposed application rules published in December 2025, state nonmember banks apply through the FDIC for subsidiary approval. The evaluation criteria include reserve backing on a 1:1 basis, management quality, redemption framework clarity, and monthly reserve disclosures.

The law also prohibits issuers from paying interest or yield to stablecoin holders. The banking industry fought for that provision. It was supposed to prevent stablecoin accounts from functioning like uninsured, unregulated deposit substitutes.

The problem is it doesn’t fully work. Not yet.

The Loophole Nobody Closed

Here’s the structural flaw: the GENIUS Act bars issuers from paying yield. It says nothing about custodians, wallets, or exchanges.

That means Coinbase, Kraken, or any crypto exchange can hold stablecoins on behalf of customers and offer yield on those balances — even when the issuer itself is prohibited from doing so. The no-yield rule has a front door and an open back window.

The American Bankers Association’s Community Bankers Council raised this directly with the Senate in early 2026, with nearly 100 community bank leaders warning that some crypto intermediaries were exploiting this gap, undermining the act’s intent. The argument from the other side is straightforward: custodians and exchanges are just like brokerage accounts, and they’ve always been allowed to pay interest on swept cash.

That argument has merit as a legal matter. As a competitive matter, it’s a problem for community banks.

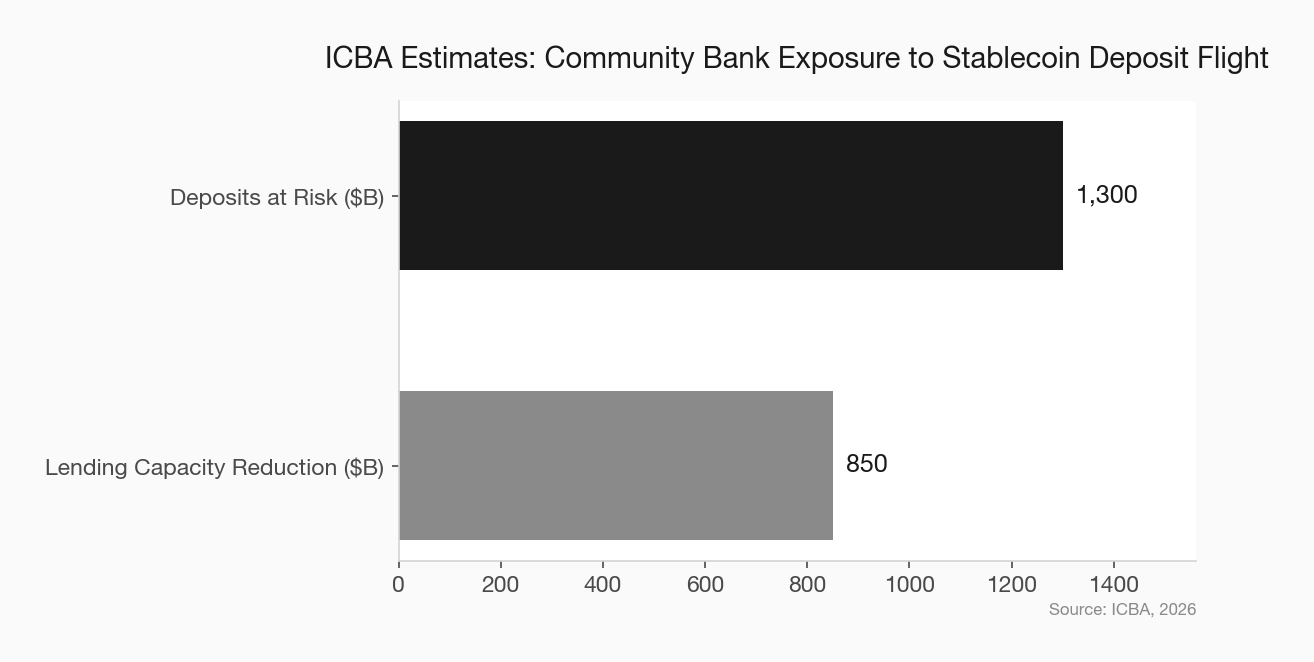

The ICBA ran the numbers. If yield-bearing stablecoin products proliferate through exchanges, the estimated impact is $1.3 trillion in reduced bank deposits — and $850 billion in reduced community bank lending capacity. JPMorgan’s broader projection put total bank deposit exposure at $6.6 trillion system-wide if stablecoin ecosystems aren’t adequately regulated.

These are projections, not certainties. But the mechanism is real. When yield migrates from bank deposits to exchange-held stablecoins, community banks lose the funding they need to make loans — and the communities that depend on those loans feel the impact first.

Why the Deposit Threat Is Structural, Not Hypothetical

Community banks don’t compete with Coinbase today. But their customers are already using stablecoins more than most executives realize.

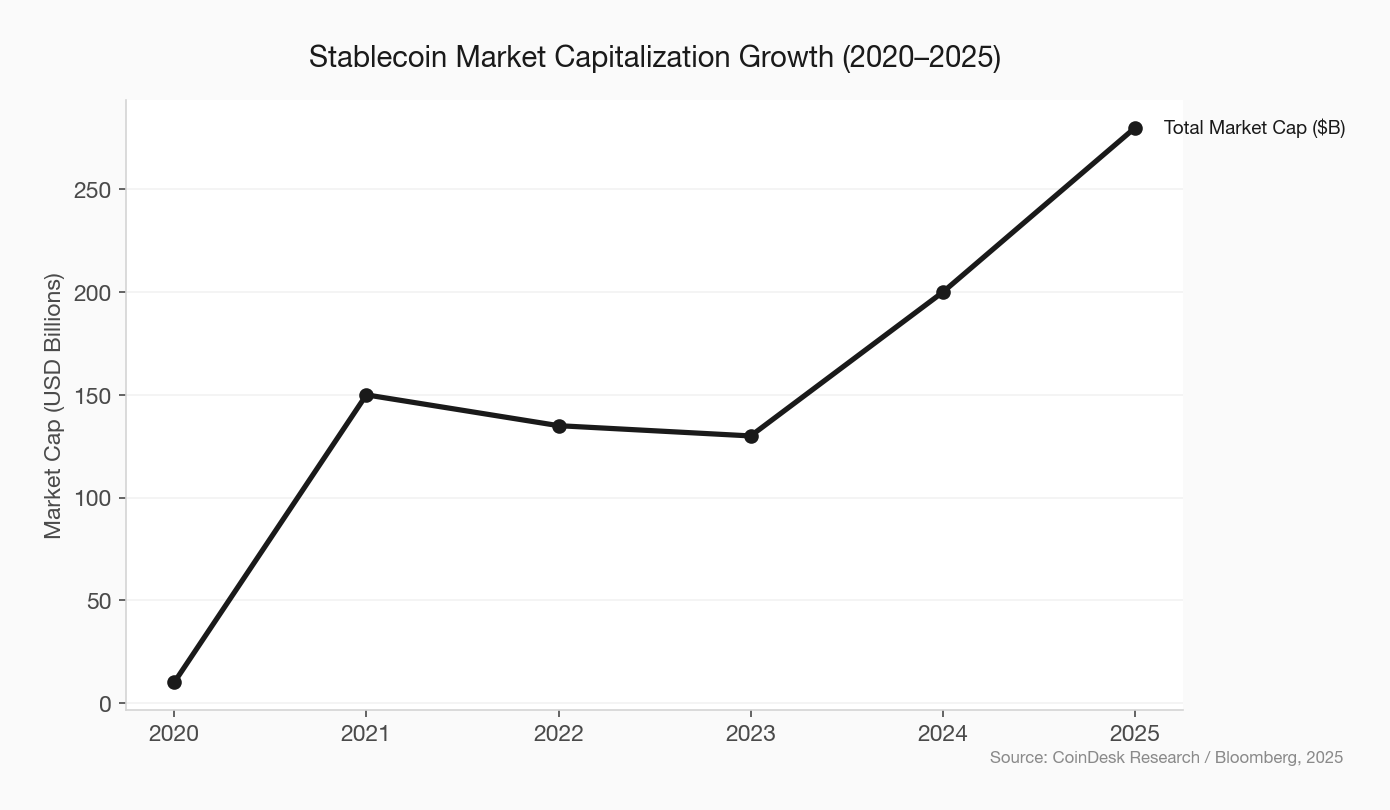

The stablecoin market crossed $280 billion in market capitalization by end of 2025, up from roughly $200 billion at the year’s start. Citi projects a base case of $1.9 trillion by 2030 — a bull case of $4 trillion. The two dominant coins, Tether’s USDT and Circle’s USDC, account for 93% of total market cap. Transaction volume hit $33 trillion last year, according to Bloomberg.

The driver isn’t speculation anymore. It’s utility. Businesses use USDC to pay international contractors in minutes, avoiding wire fees and two-day settlement windows. Freelancers hold USDT between client payments. Consumers on exchanges are earning 4-6% APY on dollar-denominated assets while their community bank savings account pays a fraction of that.

When that yield flows through a wallet holding a GENIUS Act-compliant stablecoin, it starts to look like a high-yield savings account — minus the bank relationship, minus the branch, minus the conversation with a loan officer.

The threat isn’t that customers will close their accounts tomorrow. It’s that idle cash accumulates in stablecoin ecosystems instead of sweeping back into checking or savings accounts. The deposit base erodes incrementally. Funding costs rise. Lending capacity compresses. This is the embedded finance threat applied directly to the deposit side of the balance sheet — and it moves quietly.

embedded finance threat community bank deposits

What the Implementation Clock Means for You

January 2027 is not an abstract regulatory date. For community banks considering any path involving stablecoin issuance through a subsidiary, the clock is already tight:

Establishing a subsidiary takes time. The FDIC review process runs 120 days after an application is deemed complete — and getting to “complete” requires developing the reserve infrastructure, management structure, and redemption framework the FDIC will evaluate. Add legal review, board approval, and operational buildout, and a bank starting today would be moving fast to be operational before the implementation deadline.

Banks that want to offer stablecoin-adjacent products through a fintech or correspondent partner have more time, but need to start vendor evaluation now. The market is developing rapidly and the best partnerships won’t wait until 2027.

Three Positions. Pick One.

Not every community bank needs a stablecoin product. But every community bank needs a position. There are three viable ones.

Issue

Establish a bank subsidiary, apply through the FDIC, and become a licensed stablecoin issuer. This makes sense for institutions with commercial payment customers, cross-border client relationships, or treasury operations where real-time settlement creates clear value. It’s resource-intensive and primarily appropriate for community banks above $1 billion in assets with the compliance infrastructure to support it.

Partner

Work with a fintech or correspondent bank building stablecoin infrastructure and offer access to compliant products through your existing relationship channels. You carry less regulatory burden; you maintain the customer relationship. This is the most likely near-term fit for institutions in the $250 million to $1 billion range that want a stake in the ecosystem without building the infrastructure from scratch.

Compete on relationship

Acknowledge that some idle deposits will migrate to stablecoin ecosystems and lean harder into what stablecoins fundamentally cannot provide: credit judgment, local knowledge, FDIC insurance, and the relationship that a digital wallet never replicates. Strengthen your business banking program, deepen primary banking relationships, and make sure your customers understand what distinguishes a community bank account from a Coinbase wallet.

community bank small business banking strategy community bank deposit retention relationship banking

All three are defensible strategies. Defaulting to none of them — which describes most community banks today — is not a strategy. It’s avoidance, and avoidance has a cost.

Four Things to Do Before Year-End

Conduct a deposit concentration analysis. Where is your idle float? Which business customers are moving cash off-balance-sheet into payment apps or investment accounts? Stablecoin migration will follow the same pattern. If you don’t know where your at-risk deposits sit today, you can’t defend them.

Brief your board. Most community bank boards have not had a serious conversation about the GENIUS Act, stablecoin deposit risk, or the strategic options available to the institution. That conversation needs to happen in 2026, not 2027. A 30-minute briefing — structured around the three positions above — is a reasonable starting point.

Call your core vendor. Ask directly: what stablecoin or digital asset integration is on your roadmap, and when? Core systems that don’t support real-time payment sweeps, API connectivity, or tokenized deposit infrastructure will be a barrier regardless of which path you choose. community bank core banking system API strategy This is also a useful test of whether your core vendor is thinking ahead — or just maintaining the status quo.

Get legal and compliance in the room. The FDIC comment period on proposed application rules closed in February 2026. Final rules are being finalized by regulators. Your legal team should be reading them now and providing an opinion on what the issuer subsidiary pathway would require at your institution — even if you decide not to pursue it. Knowing the cost of a door is different from opening it.

The Opportunity Inside the Threat

JPMorgan’s JPM Coin already moves billions between institutional clients on blockchain rails. Citi Token Services offers similar functionality for treasury and trade finance clients. The large banks have made their bet and are building stablecoin infrastructure into their core operations.

Community banks have a different competitive position. Their SMB customers trust them. Their local business clients need credit decisions made by someone who understands the industry, the community, and the character of the borrower — things no stablecoin wallet will ever assess. The depositor relationship that a community bank holds is not easily replicated by a digital account.

But that edge only holds if it’s actively maintained. Passive banking is how you lose deposits incrementally to every new financial product that offers marginally better yield, marginally faster payments, or marginally less friction. Stablecoins are the next version of that story.

The law is written. The rules are being finalized. The banks treating January 2027 as a starting line are going to spend years catching up to institutions that treated 2026 as a strategy year.